ASC 842 Leases — A Concise Guide to Lessee Accounting

ASC 842 governs accounting for leases. For lessees, the core idea is simple: when a company obtains the right to use identified property, plant, or equipment for a period of time in exchange for consideration, it generally recognizes a lease liability and a right-of-use asset.

That balance sheet recognition is the biggest change from legacy lease accounting. Under ASC 842, many leases that historically stayed off the balance sheet are now recognized as assets and liabilities. However, the income statement pattern still depends on whether the lease is classified as a finance lease or an operating lease.

This guide focuses only on lessee accounting. It does not cover lessor accounting.

What this guide covers — and what it does not cover

This guide covers the core ASC 842 model for lessees, including:

- identifying whether a contract contains a lease;

- separating lease and nonlease components;

- determining the lease term;

- determining lease payments;

- selecting the discount rate;

- classifying leases as finance or operating leases;

- initially measuring the lease liability and right-of-use asset;

- subsequently accounting for finance and operating leases;

- short-term lease elections;

- variable lease payments;

- lease modifications and remeasurements;

- impairment and leasehold improvements;

- presentation; and

- disclosure.

This guide focuses primarily on:

- ASC 842-10, Overall

- ASC 842-20, Lessee

ASC 842 also includes guidance for lessors, sale and leaseback transactions, and leveraged lease arrangements. Those topics are not covered in this guide. Lessor accounting is addressed separately in ASC 842-30. Sale and leaseback transactions are addressed in ASC 842-40. Leveraged lease arrangements are addressed in ASC 842-50.

Subleases and related-party or common-control leases are mentioned only at a high level. Those topics can involve additional rules and are better addressed in separate guides.

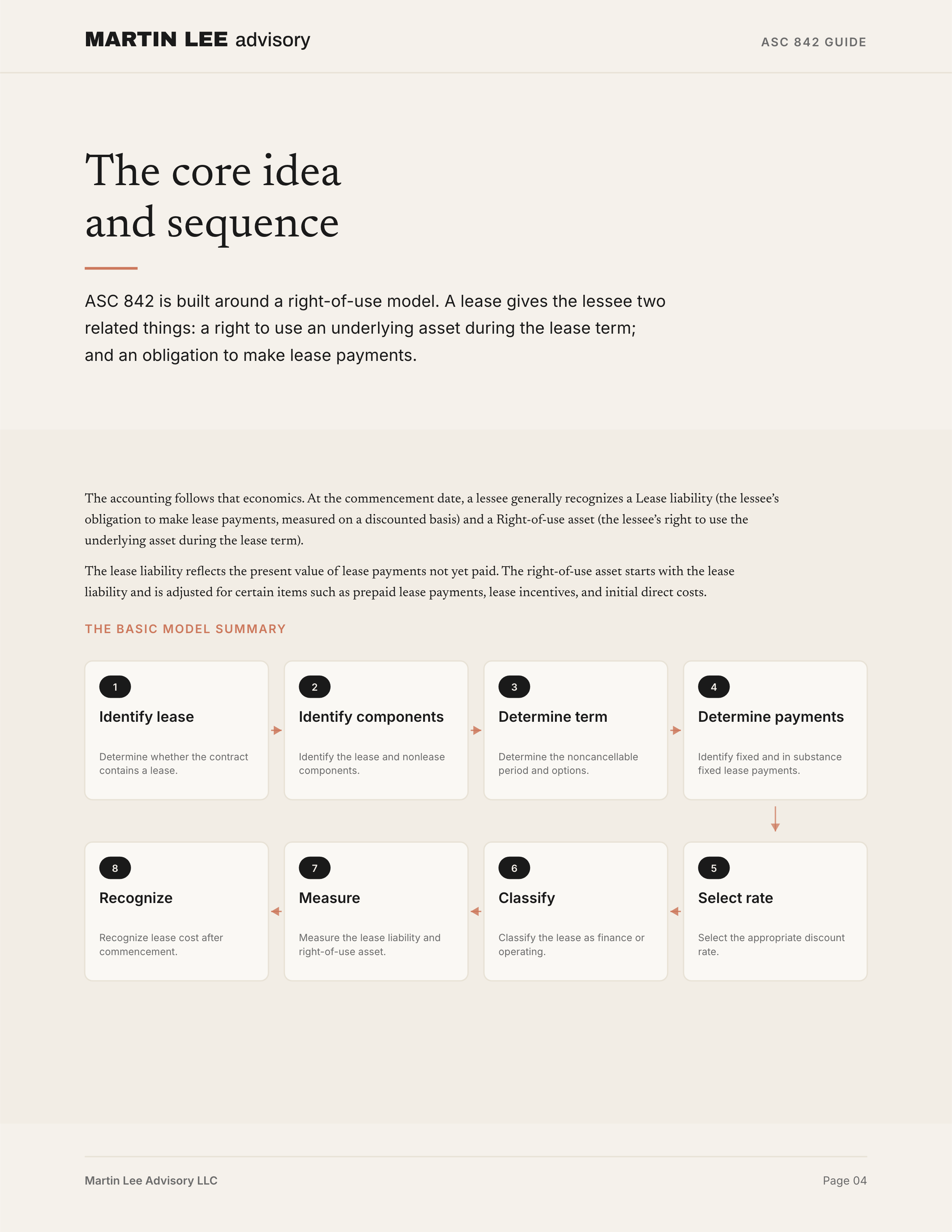

The core idea

ASC 842 is built around a right-of-use model.

A lease gives the lessee two related things:

- a right to use an underlying asset during the lease term; and

- an obligation to make lease payments.

The accounting follows that economics.

At the commencement date, a lessee generally recognizes:

| Item | What it represents |

|---|---|

| Lease liability | The lessee’s obligation to make lease payments, measured on a discounted basis. |

| Right-of-use asset | The lessee’s right to use the underlying asset during the lease term. |

The lease liability reflects the present value of lease payments not yet paid. The right-of-use asset starts with the lease liability and is adjusted for certain items such as prepaid lease payments, lease incentives, and initial direct costs.

The basic model can be summarized as follows:

Determine whether the contract contains a lease

↓

Identify the lease components

↓

Determine the lease term

↓

Determine the lease payments

↓

Select the discount rate

↓

Classify the lease

↓

Measure the lease liability and right-of-use asset

↓

Recognize lease cost after commencementStep 1: Determine whether the contract contains a lease

The first question is whether the contract is, or contains, a lease.

A contract contains a lease if it conveys the right to control the use of identified property, plant, or equipment for a period of time in exchange for consideration.

This definition has three key parts:

- there must be an identified asset;

- the customer must have the right to obtain substantially all of the economic benefits from use of that asset; and

- the customer must have the right to direct the use of that asset.

If those conditions are met, the contract contains a lease. If they are not met, the arrangement may be a service contract instead.

Identified asset

A lease requires an identified asset. The asset may be explicitly specified in the contract, such as a particular building, vehicle, floor, server, or piece of equipment. It may also be implicitly specified if the supplier can fulfill the contract only by using a particular asset.

An asset is not identified if the supplier has a substantive substitution right throughout the period of use. A substitution right is substantive only if both of the following are true:

- the supplier has the practical ability to substitute alternative assets throughout the period of use; and

- the supplier would benefit economically from substituting the asset.

A supplier’s right to substitute an asset only for repairs, maintenance, malfunction, or technical upgrades generally does not prevent the asset from being identified.

If the customer cannot readily determine whether the supplier’s substitution right is substantive, the customer presumes that the substitution right is not substantive.

Portions of assets

A physically distinct portion of an asset can be an identified asset. Examples include a floor of a building or a segment of a pipeline that connects a customer to a larger pipeline.

A capacity portion of a larger asset is not an identified asset unless it represents substantially all of the capacity of that asset. For example, a specified number of physically distinct dark fibers in a fiber-optic cable may be identified assets, while a capacity portion of a larger cable generally is not unless it represents substantially all of the cable’s capacity.

Right to obtain economic benefits

The lessee must have the right to obtain substantially all of the economic benefits from use of the identified asset during the period of use.

Economic benefits can come from using, holding, or subleasing the asset. They include primary outputs, by-products, and other benefits that can be realized from use of the asset.

The analysis is performed within the scope of the customer’s right to use the asset. For example, if a vehicle can be used only within a specified territory or up to a specified mileage limit, the analysis considers the economic benefits within those contractual limits.

A requirement to pay the supplier a portion of the cash flows generated from use of the asset does not, by itself, prevent the customer from obtaining substantially all of the economic benefits. For example, percentage rent based on sales from leased retail space does not prevent the lessee from controlling the use of the retail space.

Right to direct the use

The lessee must also have the right to direct the use of the identified asset during the period of use.

A customer has the right to direct the use of an identified asset if either:

- the customer has the right to direct how and for what purpose the asset is used; or

- the relevant decisions about how and for what purpose the asset is used are predetermined, and the customer either has the right to operate the asset or designed the asset in a way that predetermines its use.

The key question is who controls the relevant decisions that most affect the economic benefits from using the asset.

Examples of decision-making rights that may indicate control include the right to decide:

- what type of output the asset produces;

- when output is produced;

- where output is produced;

- whether output is produced; and

- how much output is produced.

Rights limited to operating or maintaining an asset do not usually give the customer the right to direct use, unless the relevant decisions about how and for what purpose the asset is used are predetermined and the customer controls operation.

Protective rights

A contract may include restrictions designed to protect the supplier’s asset, personnel, or compliance with laws and regulations. These are protective rights.

Protective rights may limit how the lessee uses the asset, but they do not necessarily prevent the lessee from controlling the asset. For example, a lease may limit where an aircraft can fly, what cargo a ship can carry, or what type of business can operate in leased retail space. Those restrictions often define the scope of the lessee’s right of use rather than giving control back to the supplier.

Embedded leases

A contract does not need to be labeled a lease to contain a lease.

Service, outsourcing, logistics, data center, transportation, supply, and power arrangements may contain embedded leases if the customer controls the use of identified property, plant, or equipment.

The embedded lease analysis is often one of the most important parts of ASC 842. A contract that looks like a service contract may contain a lease if the customer controls an identified asset. Conversely, a contract that depends on a supplier’s equipment may not contain a lease if the supplier controls how and for what purpose the equipment is used.

A practical screen is:

Is there an identified asset?

↓

No → no lease

↓

Yes

↓

Does the customer obtain substantially all economic benefits from use?

↓

No → no lease

↓

Yes

↓

Does the customer direct how and for what purpose the asset is used?

↓

No → no lease

↓

Yes → contract contains a leaseStep 2: Identify lease and nonlease components

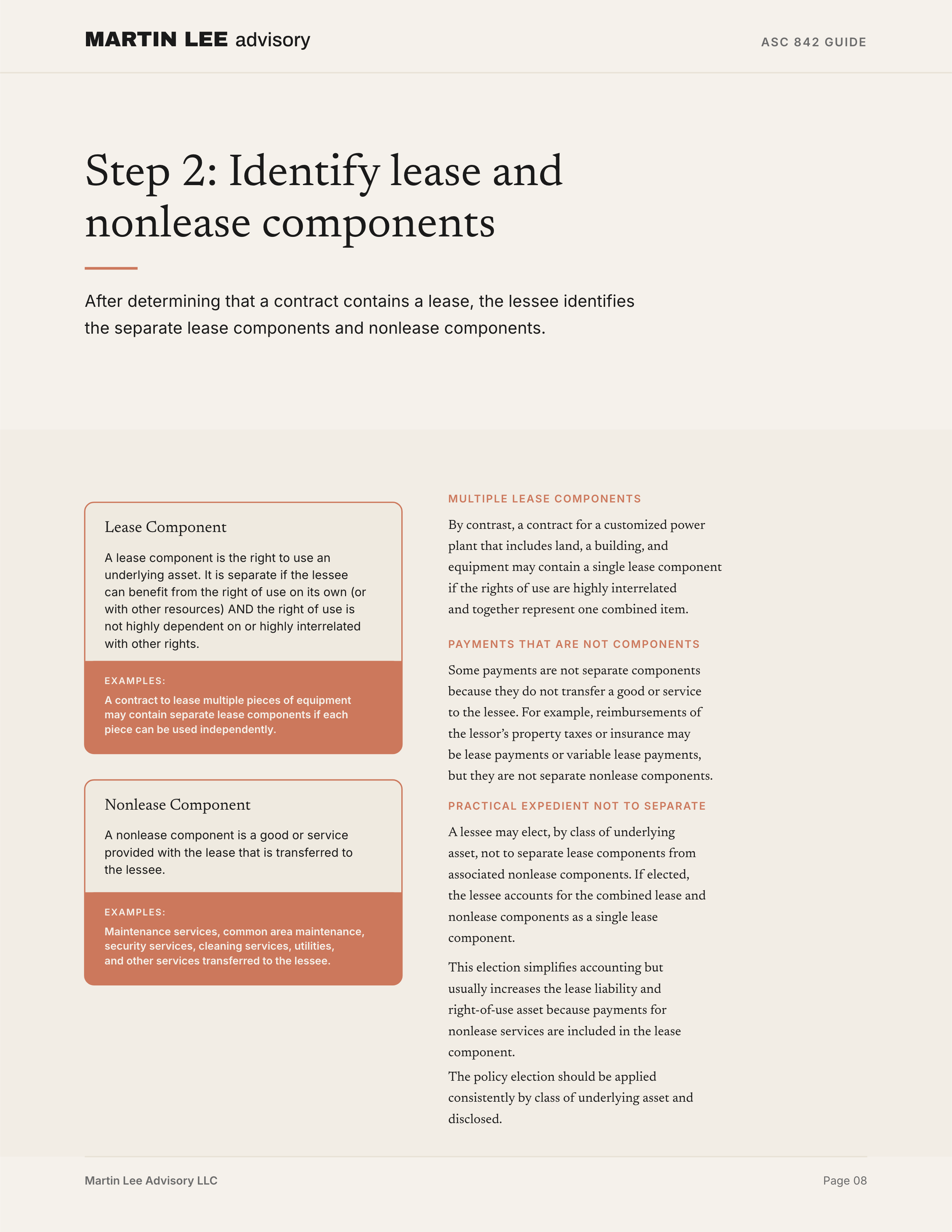

After determining that a contract contains a lease, the lessee identifies the separate lease components and nonlease components.

A lease component is the right to use an underlying asset. A nonlease component is a good or service provided with the lease, such as maintenance, common area maintenance, utilities, cleaning, security, or other services.

A right to use an underlying asset is a separate lease component if both of the following are true:

- the lessee can benefit from the right of use on its own or together with other readily available resources; and

- the right of use is not highly dependent on or highly interrelated with other rights of use in the contract.

For example, a contract to lease multiple pieces of equipment may contain separate lease components if each piece of equipment can be used independently and is not highly dependent on the others.

By contrast, a contract for a customized power plant that includes land, a building, and equipment may contain a single lease component if the rights of use are highly interrelated and together represent one combined item.

Nonlease components

Nonlease components are accounted for separately from lease components unless the lessee elects a practical expedient.

Common nonlease components include:

- maintenance services;

- common area maintenance;

- security services;

- cleaning services;

- utilities; and

- other services transferred to the lessee.

Some payments are not separate components because they do not transfer a good or service to the lessee. For example, reimbursements of the lessor’s property taxes or insurance may be lease payments or variable lease payments, but they are not separate nonlease components.

Practical expedient not to separate lease and nonlease components

A lessee may elect, by class of underlying asset, not to separate lease components from associated nonlease components. If elected, the lessee accounts for the combined lease and nonlease components as a single lease component.

This election simplifies accounting but usually increases the lease liability and right-of-use asset because payments for nonlease services are included in the lease component.

The policy election should be applied consistently by class of underlying asset and disclosed.

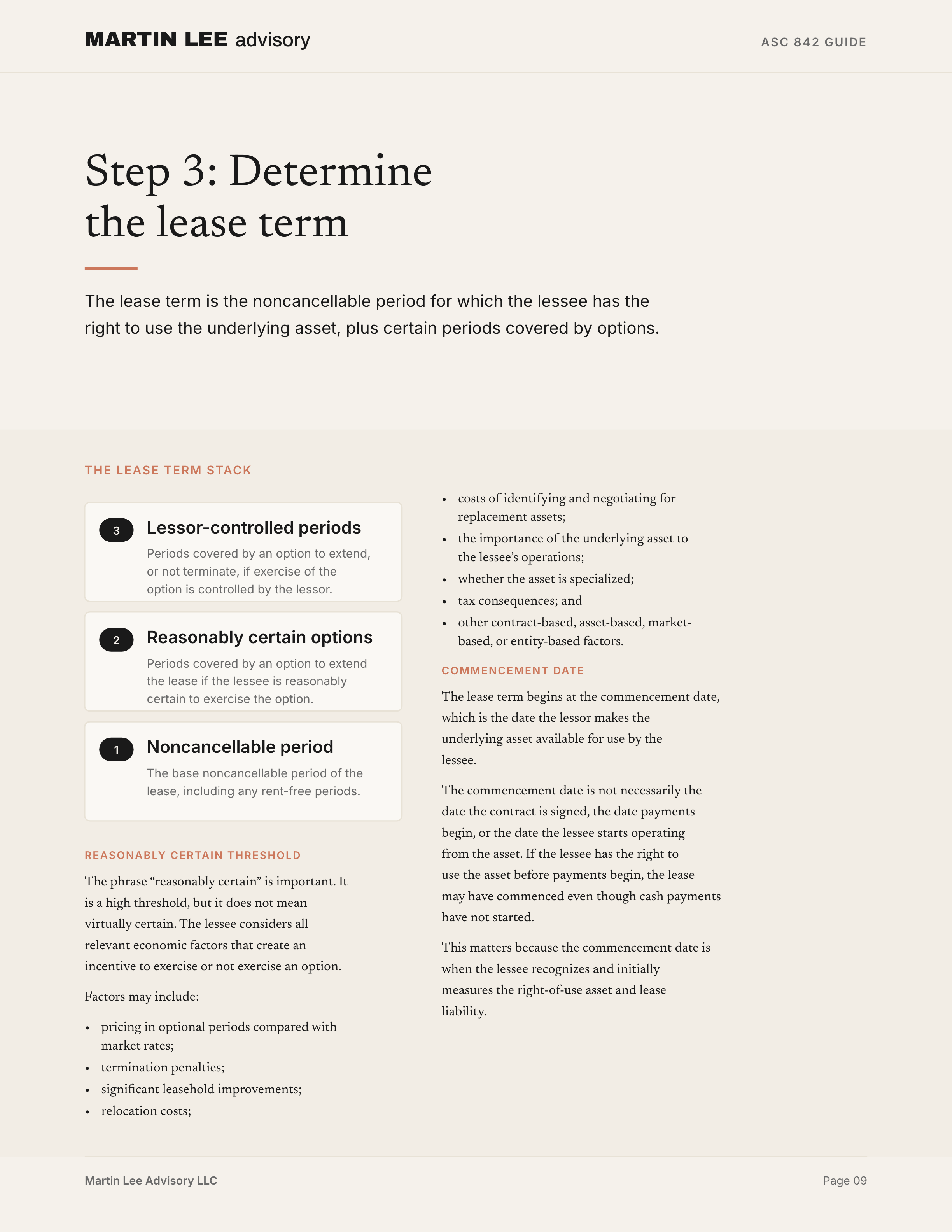

Step 3: Determine the lease term

The lease term is the noncancellable period for which the lessee has the right to use the underlying asset, plus certain periods covered by options.

The lease term includes:

- the noncancellable period of the lease;

- periods covered by an option to extend the lease if the lessee is reasonably certain to exercise the option;

- periods covered by an option to terminate the lease if the lessee is reasonably certain not to exercise the option; and

- periods covered by an option to extend, or not terminate, the lease if exercise of the option is controlled by the lessor.

The phrase “reasonably certain” is important. It is a high threshold, but it does not mean virtually certain. The lessee considers all relevant economic factors that create an incentive to exercise or not exercise an option.

Factors may include:

- pricing in optional periods compared with market rates;

- termination penalties;

- significant leasehold improvements;

- relocation costs;

- costs of identifying and negotiating for replacement assets;

- the importance of the underlying asset to the lessee’s operations;

- whether the asset is specialized;

- tax consequences; and

- other contract-based, asset-based, market-based, or entity-based factors.

The lease term begins at the commencement date and includes any rent-free periods.

Commencement date

The commencement date is the date the lessor makes the underlying asset available for use by the lessee.

The commencement date is not necessarily the date the contract is signed, the date payments begin, or the date the lessee starts operating from the asset. If the lessee has the right to use the asset before payments begin, the lease may have commenced even though cash payments have not started.

This matters because the commencement date is when the lessee recognizes and initially measures the right-of-use asset and lease liability.

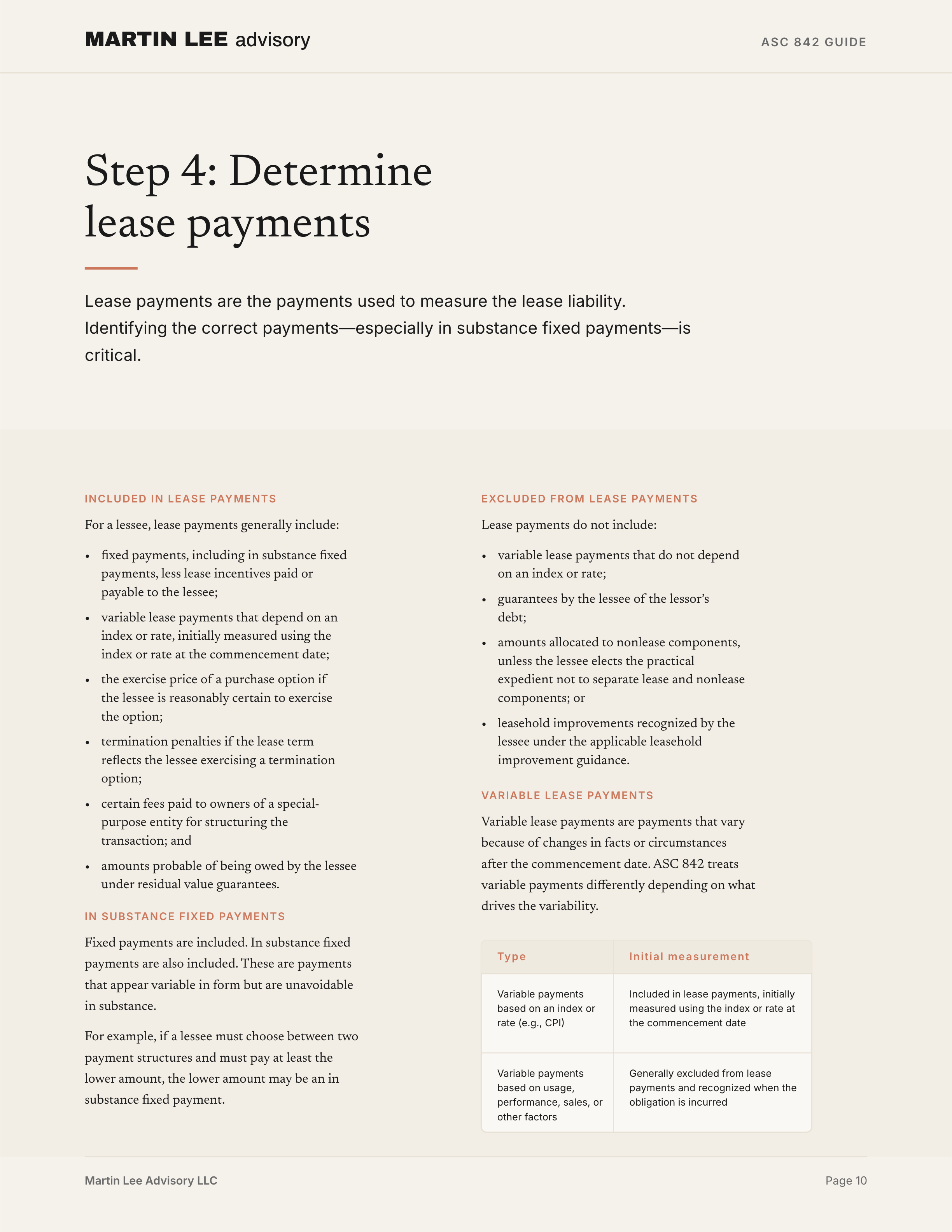

Step 4: Determine lease payments

Lease payments are the payments used to measure the lease liability.

For a lessee, lease payments generally include:

- fixed payments, including in substance fixed payments, less lease incentives paid or payable to the lessee;

- variable lease payments that depend on an index or rate, initially measured using the index or rate at the commencement date;

- the exercise price of a purchase option if the lessee is reasonably certain to exercise the option;

- termination penalties if the lease term reflects the lessee exercising a termination option;

- certain fees paid to owners of a special-purpose entity for structuring the transaction; and

- amounts probable of being owed by the lessee under residual value guarantees.

Lease payments do not include:

- variable lease payments that do not depend on an index or rate;

- guarantees by the lessee of the lessor’s debt;

- amounts allocated to nonlease components, unless the lessee elects the practical expedient not to separate lease and nonlease components; or

- leasehold improvements recognized by the lessee under the applicable leasehold improvement guidance.

Fixed and in substance fixed payments

Fixed payments are included in lease payments.

In substance fixed payments are also included. These are payments that appear variable in form but are unavoidable in substance.

For example, if a lessee must choose between two payment structures and must pay at least the lower amount, the lower amount may be an in substance fixed payment.

Variable lease payments

Variable lease payments are payments that vary because of changes in facts or circumstances after the commencement date.

ASC 842 treats variable payments differently depending on what drives the variability.

| Type of variable payment | Initial measurement treatment |

|---|---|

| Variable payments based on an index or rate | Included in lease payments, initially measured using the index or rate at the commencement date. |

| Variable payments based on usage, performance, sales, or other factors | Generally excluded from lease payments and recognized when the obligation is incurred. |

For example, lease payments that increase based on CPI are included in the initial lease liability using the CPI at commencement. Later changes in CPI generally do not update the lease liability unless the liability is remeasured for another reason.

By contrast, rent based on a percentage of sales is generally excluded from the lease liability and recognized as variable lease cost when the sales occur.

Lease incentives

Lease incentives reduce the measurement of the right-of-use asset and may reduce lease payments depending on how they are structured.

Lease incentives include payments made to or on behalf of the lessee. They also may include certain losses incurred by the lessor from assuming a lessee’s preexisting lease with a third party.

Common examples include:

- cash payments from the lessor to the lessee;

- tenant improvement allowances;

- reimbursement of moving costs; and

- assumption of a preexisting lease obligation.

The accounting depends on the substance of the arrangement and whether the payment is a lease incentive, a reimbursement for lessee-owned improvements, or something else.

Initial direct costs

Initial direct costs are incremental costs of a lease that would not have been incurred if the lease had not been obtained.

For a lessee, initial direct costs are included in the right-of-use asset. They are not included in the lease liability.

Costs that would have been incurred regardless of whether the lease was obtained are not initial direct costs. For example, internal salaries, legal costs to negotiate lease terms, and general overhead generally do not qualify merely because they relate to lease activity.

Step 5: Determine the discount rate

The lessee uses a discount rate to measure the lease liability.

The discount rate is selected at the commencement date using information available at that date.

A lessee uses the rate implicit in the lease if that rate is readily determinable. If the rate implicit in the lease is not readily determinable, the lessee uses its incremental borrowing rate.

The incremental borrowing rate is the rate the lessee would pay to borrow, on a collateralized basis, an amount equal to the lease payments over a similar term in a similar economic environment.

Nonpublic entity risk-free rate election

A lessee that is not a public business entity may elect to use a risk-free discount rate instead of its incremental borrowing rate. The election is made by class of underlying asset.

This election can reduce complexity, especially for private companies that do not have readily available borrowing rates. However, using a risk-free rate often results in a larger lease liability and right-of-use asset because risk-free rates are usually lower than incremental borrowing rates.

A lessee that makes this election must disclose the election and the class or classes of underlying assets to which it applies.

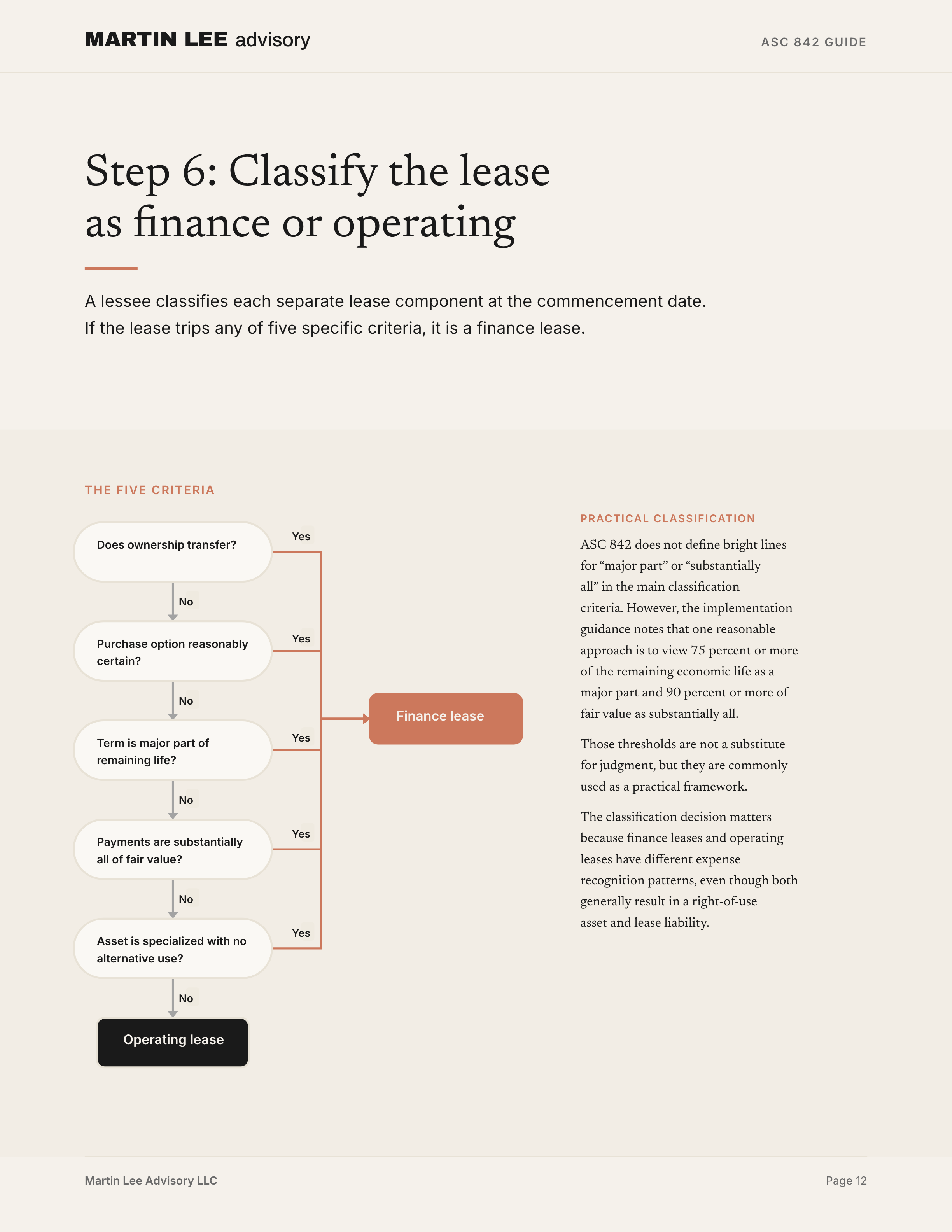

Step 6: Classify the lease as finance or operating

A lessee classifies each separate lease component at the commencement date as either a finance lease or an operating lease.

A lease is classified as a finance lease if any of the following criteria are met:

- the lease transfers ownership of the underlying asset to the lessee by the end of the lease term;

- the lease grants the lessee an option to purchase the underlying asset that the lessee is reasonably certain to exercise;

- the lease term is for the major part of the remaining economic life of the underlying asset;

- the present value of the lease payments and certain residual value guarantees equals or exceeds substantially all of the fair value of the underlying asset; or

- the underlying asset is of such a specialized nature that it is expected to have no alternative use to the lessor at the end of the lease term.

If none of those criteria are met, the lessee classifies the lease as an operating lease.

Practical classification considerations

ASC 842 does not define bright lines for “major part” or “substantially all” in the main classification criteria. However, the implementation guidance notes that one reasonable approach is to view 75 percent or more of the remaining economic life as a major part and 90 percent or more of fair value as substantially all.

Those thresholds are not a substitute for judgment, but they are commonly used as a practical framework.

The classification decision matters because finance leases and operating leases have different expense recognition patterns, even though both generally result in a right-of-use asset and lease liability.

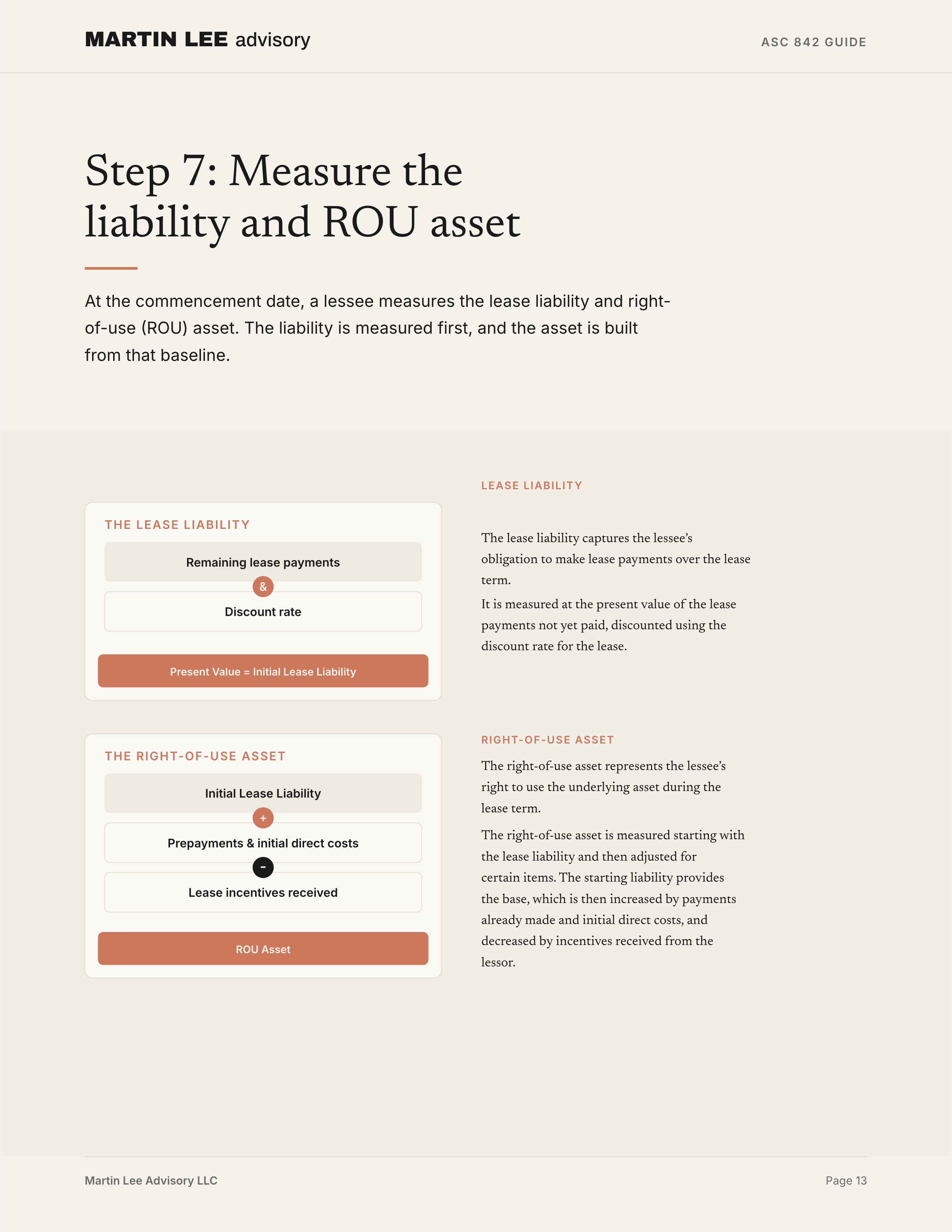

Step 7: Measure the lease liability and right-of-use asset

At the commencement date, a lessee measures the lease liability and right-of-use asset.

Lease liability

The lease liability is measured at the present value of the lease payments not yet paid, discounted using the discount rate for the lease.

In simplified form:

Lease liability

=

Present value of lease payments not yet paidThe lease liability captures the lessee’s obligation to make lease payments over the lease term.

Right-of-use asset

The right-of-use asset is measured starting with the lease liability and then adjusted for certain items.

In simplified form:

Right-of-use asset

=

Initial lease liability

+ lease payments made at or before commencement

- lease incentives received

+ lessee initial direct costsThe right-of-use asset represents the lessee’s right to use the underlying asset during the lease term.

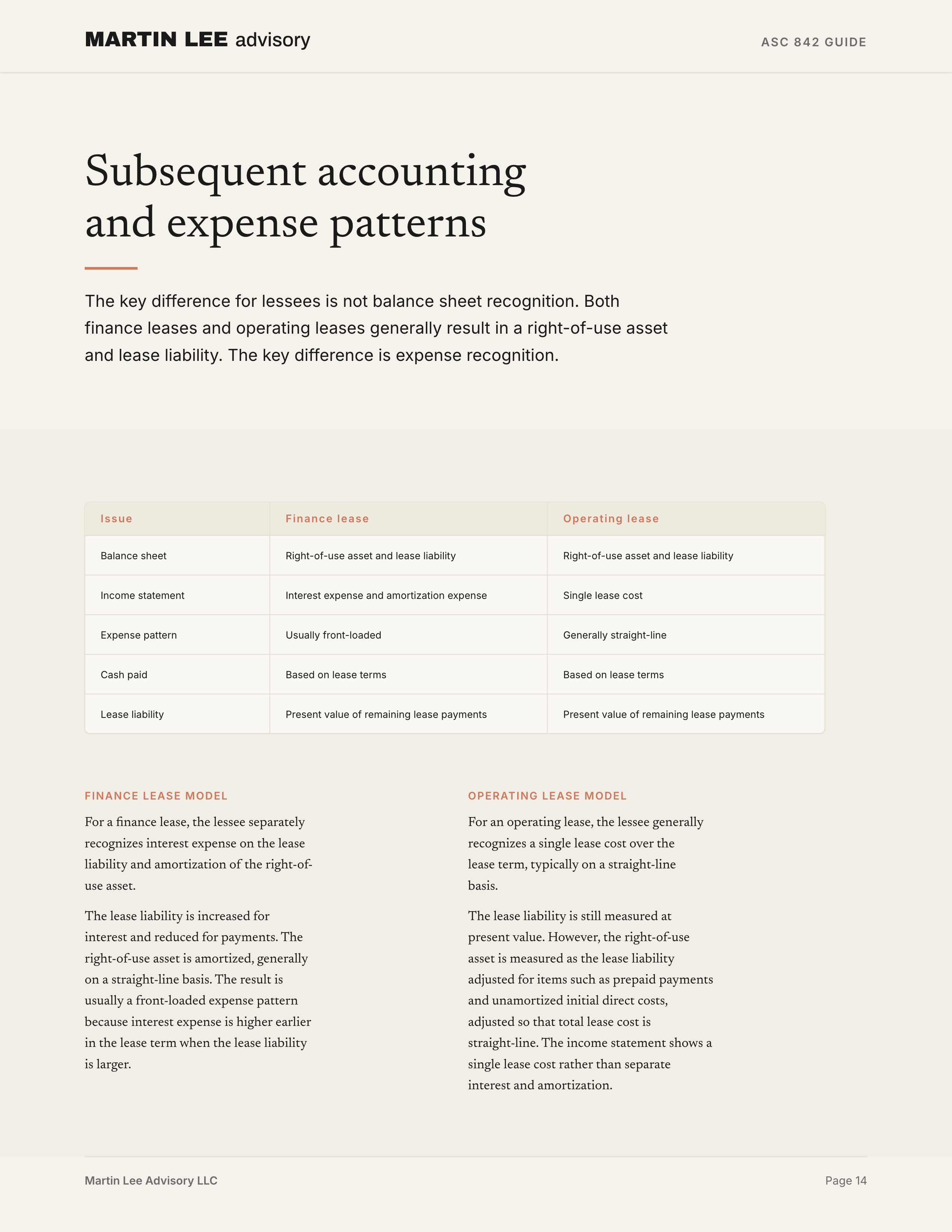

Finance lease subsequent accounting

For a finance lease, the lessee separately recognizes:

- interest expense on the lease liability; and

- amortization of the right-of-use asset.

The lease liability is increased for interest and reduced for lease payments. The right-of-use asset is amortized, generally on a straight-line basis unless another systematic basis better reflects the pattern in which the lessee consumes the asset’s benefits.

The result is usually a front-loaded expense pattern because interest expense is higher earlier in the lease term when the lease liability is larger.

The basic finance lease model is:

Lease liability

→ accrete interest using the discount rate

→ reduce for payments made

Right-of-use asset

→ amortize over the applicable period

Income statement

→ interest expense + amortization expenseThe right-of-use asset is amortized from the commencement date to the earlier of the end of the useful life of the right-of-use asset or the end of the lease term. However, if the lease transfers ownership or the lessee is reasonably certain to exercise a purchase option, the asset is amortized to the end of the useful life of the underlying asset.

Operating lease subsequent accounting

For an operating lease, the lessee generally recognizes a single lease cost over the lease term, typically on a straight-line basis.

The lease liability is still measured at the present value of remaining lease payments. However, the right-of-use asset is measured as the lease liability adjusted for items such as prepaid or accrued lease payments, remaining lease incentives, unamortized initial direct costs, and impairment.

The basic operating lease model is:

Lease liability

→ accrete interest using the discount rate

→ reduce for payments made

Right-of-use asset

→ adjusted so that total lease cost is generally straight-line

Income statement

→ single lease costThis is why operating lease accounting under ASC 842 can feel unusual. The lessee records a lease liability and right-of-use asset on the balance sheet, but the income statement generally shows a single lease cost rather than separate interest and amortization.

Finance lease vs. operating lease

The key difference for lessees is not balance sheet recognition. Both finance leases and operating leases generally result in a right-of-use asset and lease liability.

The key difference is expense recognition.

| Issue | Finance lease | Operating lease |

|---|---|---|

| Balance sheet | Right-of-use asset and lease liability | Right-of-use asset and lease liability |

| Income statement | Interest expense and amortization expense | Single lease cost |

| Expense pattern | Usually front-loaded | Generally straight-line |

| Cash paid | Based on lease terms | Based on lease terms |

| Lease liability measurement | Present value of remaining lease payments | Present value of remaining lease payments |

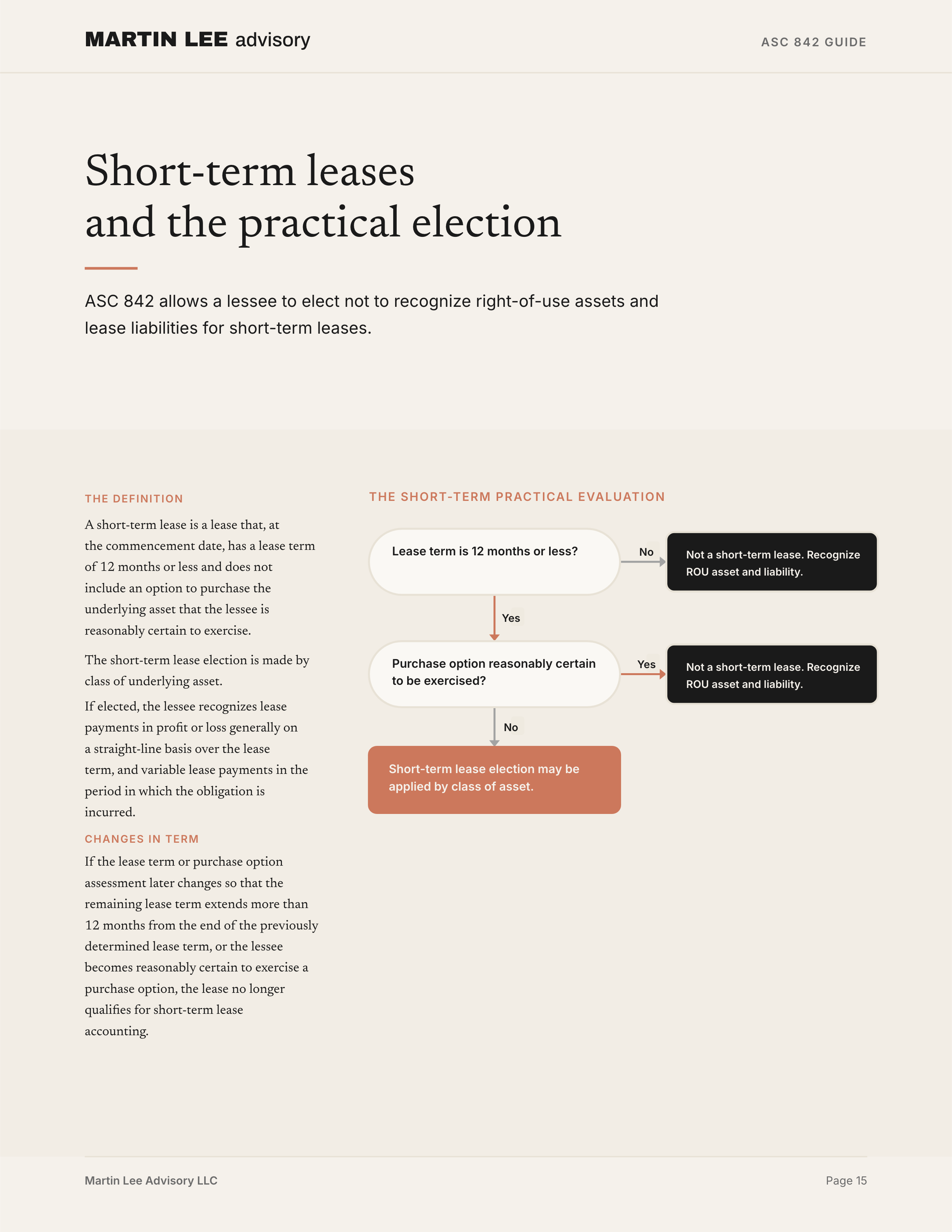

Short-term leases

ASC 842 allows a lessee to elect not to recognize right-of-use assets and lease liabilities for short-term leases.

A short-term lease is a lease that, at the commencement date, has a lease term of 12 months or less and does not include an option to purchase the underlying asset that the lessee is reasonably certain to exercise.

The short-term lease election is made by class of underlying asset.

If elected, the lessee recognizes lease payments in profit or loss generally on a straight-line basis over the lease term, and variable lease payments in the period in which the obligation is incurred.

A practical way to evaluate the election is:

Lease term is 12 months or less?

↓

No → not a short-term lease

↓

Yes

↓

Purchase option reasonably certain to be exercised?

↓

Yes → not a short-term lease

↓

No → short-term lease election may be appliedIf the lease term or purchase option assessment later changes so that the remaining lease term extends more than 12 months from the end of the previously determined lease term, or the lessee becomes reasonably certain to exercise a purchase option, the lease no longer qualifies for short-term lease accounting.

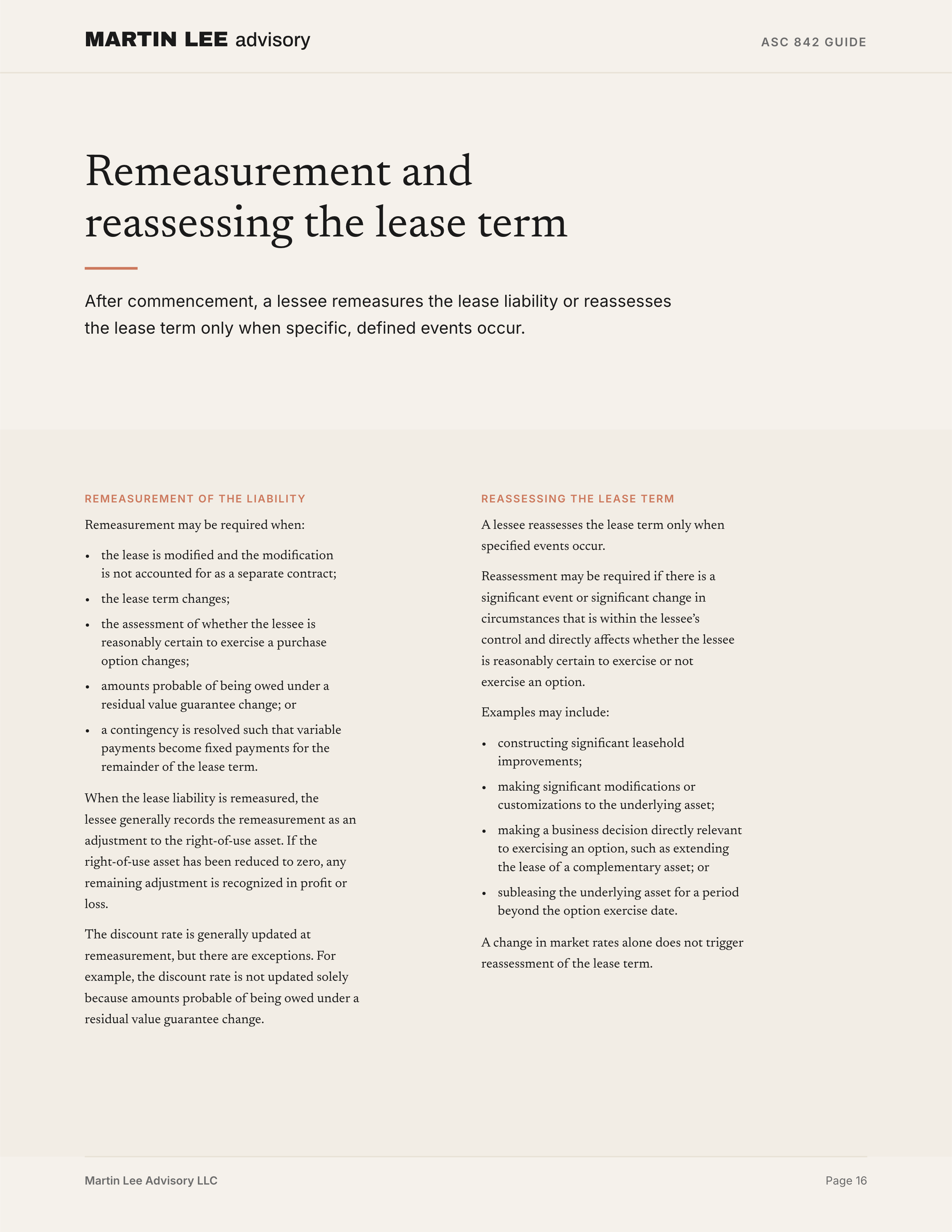

Remeasurement of the lease liability

After commencement, a lessee remeasures the lease liability when certain events occur.

Remeasurement may be required when:

- the lease is modified and the modification is not accounted for as a separate contract;

- the lease term changes;

- the assessment of whether the lessee is reasonably certain to exercise a purchase option changes;

- amounts probable of being owed under a residual value guarantee change; or

- a contingency is resolved such that variable payments become fixed payments for the remainder of the lease term.

When the lease liability is remeasured, the lessee generally records the remeasurement as an adjustment to the right-of-use asset. If the right-of-use asset has been reduced to zero, any remaining adjustment is recognized in profit or loss.

The discount rate is generally updated at remeasurement, but there are exceptions. For example, the discount rate is not updated solely because amounts probable of being owed under a residual value guarantee change.

Reassessing the lease term

A lessee reassesses the lease term only when specified events occur.

Reassessment may be required if there is a significant event or significant change in circumstances that is within the lessee’s control and directly affects whether the lessee is reasonably certain to exercise or not exercise an option.

Examples may include:

- constructing significant leasehold improvements;

- making significant modifications or customizations to the underlying asset;

- making a business decision directly relevant to exercising an option, such as extending the lease of a complementary asset; or

- subleasing the underlying asset for a period beyond the option exercise date.

A change in market rates alone does not trigger reassessment of the lease term.

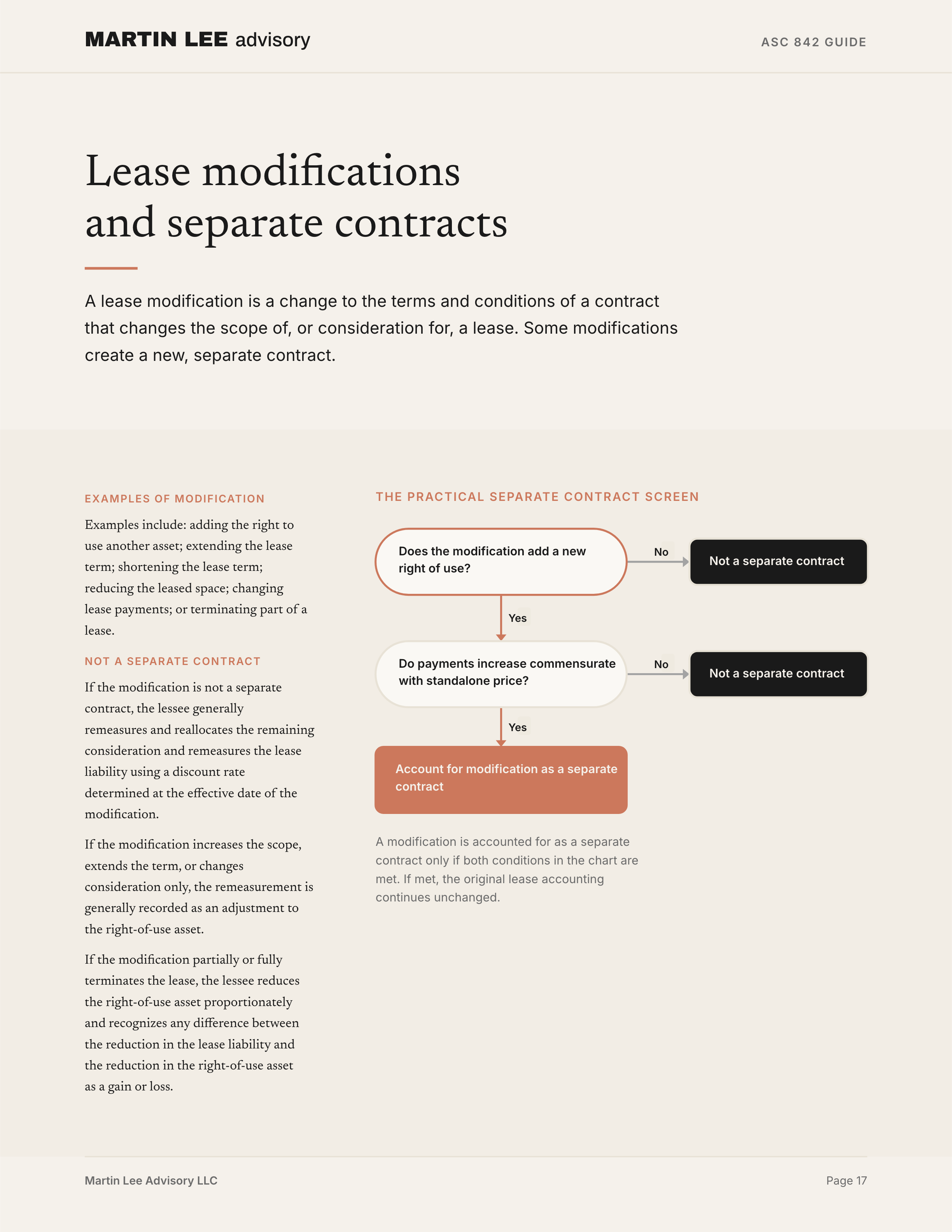

Lease modifications

A lease modification is a change to the terms and conditions of a contract that changes the scope of, or consideration for, a lease.

Examples include:

- adding the right to use another asset;

- extending the lease term;

- shortening the lease term;

- reducing the leased space;

- changing lease payments; or

- terminating part of a lease.

A modification is accounted for as a separate contract only if both of the following are true:

- the modification grants the lessee an additional right of use not included in the original lease; and

- the lease payments increase by an amount commensurate with the standalone price of the additional right of use, adjusted for the circumstances of the contract.

If those conditions are met, the lessee accounts for the modification as a separate lease. The original lease accounting continues unchanged.

If the modification is not a separate contract, the lessee generally remeasures and reallocates the remaining consideration and remeasures the lease liability using a discount rate determined at the effective date of the modification.

If the modification increases the scope, extends the term, or changes consideration only, the remeasurement is generally recorded as an adjustment to the right-of-use asset.

If the modification partially or fully terminates the lease, the lessee reduces the right-of-use asset proportionately and recognizes any difference between the reduction in the lease liability and the reduction in the right-of-use asset as a gain or loss.

A practical modification screen is:

Does the modification add a new right of use?

↓

No → not a separate contract

↓

Yes

↓

Do payments increase commensurate with standalone price?

↓

No → not a separate contract

↓

Yes → account for as a separate contractVariable lease payments after commencement

Variable lease payments that are not included in the lease liability are recognized in the period in which the obligation is incurred.

Examples include:

- payments based on sales;

- payments based on usage;

- performance-based payments; and

- variable reimbursements not based on an index or rate.

If variable lease payments depend on an index or rate, they are included in the initial lease liability using the index or rate at commencement. Later changes in the index or rate are generally recognized as variable lease cost unless the lease liability is remeasured for another reason.

Maintenance deposits

Some leases require the lessee to make maintenance deposits, sometimes called maintenance reserves or supplemental rent.

If the deposits are refundable only when the lessee performs specified maintenance, the lessee generally accounts for the payments as a deposit asset. The lessee evaluates whether it is probable that amounts on deposit will be returned to reimburse maintenance costs. Amounts less than probable of being returned are recognized in the same manner as variable lease expense.

When the maintenance is performed, the maintenance costs are expensed or capitalized under the lessee’s maintenance accounting policy.

Impairment of right-of-use assets

A lessee evaluates right-of-use assets for impairment under the long-lived asset impairment guidance in ASC 360.

If a right-of-use asset is impaired, the lessee recognizes an impairment loss. After impairment, the subsequent accounting for the right-of-use asset changes because the asset is measured at its carrying amount immediately after impairment, less subsequent amortization.

For an operating lease, impairment can change the pattern of lease cost recognition. After impairment, the single lease cost is calculated as the sum of amortization of the remaining right-of-use asset and accretion of the lease liability.

The practical point is important: operating lease cost may no longer be straight-line after the right-of-use asset is impaired.

Leasehold improvements

Leasehold improvements are accounted for separately from the right-of-use asset.

Generally, leasehold improvements are amortized over the shorter of:

- the useful life of the leasehold improvements; and

- the remaining lease term.

However, if the lease transfers ownership of the underlying asset to the lessee or the lessee is reasonably certain to exercise a purchase option, leasehold improvements are amortized over their useful life.

ASC 842 includes special guidance for leasehold improvements associated with leases between entities under common control. Because that guidance is specialized, this overview does not cover it in detail.

Subleases

A sublease occurs when the original lessee re-leases the underlying asset to a third party while the original lease remains in effect.

Subleases can create additional accounting questions because the original lessee may become an intermediate lessor. If the original lessee is not relieved of its primary obligation under the head lease, it generally continues to account for the original lease.

Sublease accounting can require consideration of both lessee and lessor guidance, as well as impairment if expected sublease income is less than the related lease cost. Because subleases can become complex quickly, this guide treats them as a separate topic.

Termination of a lease

If a lease is terminated before the end of the lease term, the lessee derecognizes the right-of-use asset and lease liability and recognizes any difference in profit or loss.

If the lessee purchases the underlying asset, the transaction is not accounted for as a lease termination in the same way. Instead, the purchase is treated as part of acquiring the underlying asset. Any difference between the purchase price and the carrying amount of the lease liability immediately before purchase is recorded as an adjustment to the carrying amount of the acquired asset.

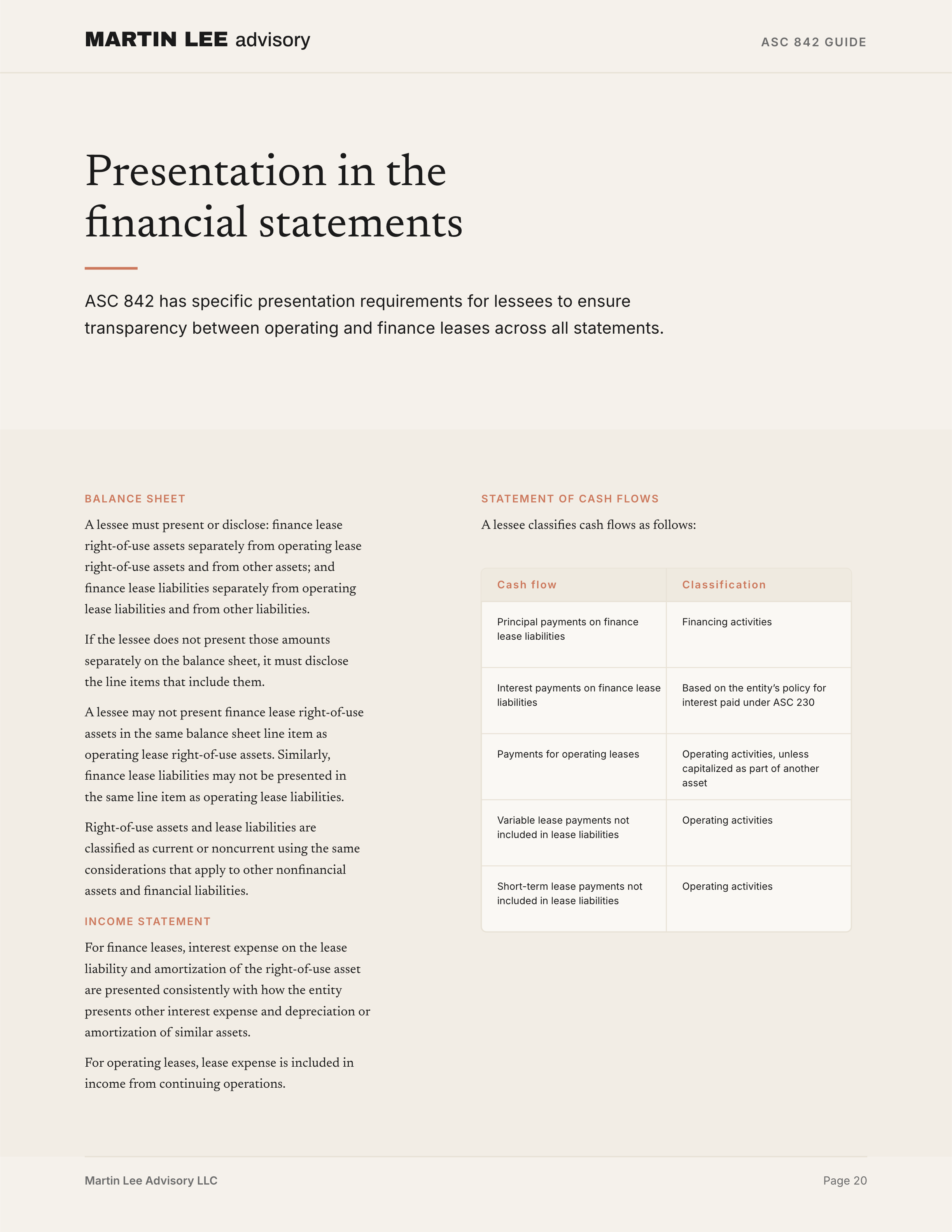

Presentation

ASC 842 has specific presentation requirements for lessees.

Balance sheet

A lessee must present or disclose:

- finance lease right-of-use assets separately from operating lease right-of-use assets and from other assets; and

- finance lease liabilities separately from operating lease liabilities and from other liabilities.

If the lessee does not present those amounts separately on the balance sheet, it must disclose the line items that include them.

A lessee may not present finance lease right-of-use assets in the same balance sheet line item as operating lease right-of-use assets. Similarly, finance lease liabilities may not be presented in the same line item as operating lease liabilities.

Right-of-use assets and lease liabilities are classified as current or noncurrent using the same considerations that apply to other nonfinancial assets and financial liabilities.

Income statement

For finance leases, interest expense on the lease liability and amortization of the right-of-use asset are presented consistently with how the entity presents other interest expense and depreciation or amortization of similar assets.

For operating leases, lease expense is included in income from continuing operations.

Statement of cash flows

A lessee classifies cash flows as follows:

| Cash flow | Classification |

|---|---|

| Principal payments on finance lease liabilities | Financing activities |

| Interest payments on finance lease liabilities | Based on the entity’s policy for interest paid under ASC 230 |

| Payments for operating leases | Operating activities, unless capitalized as part of another asset |

| Variable lease payments not included in lease liabilities | Operating activities |

| Short-term lease payments not included in lease liabilities | Operating activities |

Disclosure

The disclosure objective is to enable users of financial statements to assess the amount, timing, and uncertainty of cash flows arising from leases.

A lessee discloses qualitative and quantitative information about:

- its leases;

- significant judgments made in applying ASC 842; and

- amounts recognized in the financial statements relating to leases.

The level of detail should be useful. A lessee should avoid obscuring meaningful information with too much insignificant detail or by aggregating leases with different characteristics.

Qualitative disclosures

A lessee discloses information about the nature of its leases, including:

- a general description of leases;

- the basis and terms for variable lease payments;

- options to extend or terminate leases;

- options recognized as part of right-of-use assets and lease liabilities and those not recognized;

- residual value guarantees;

- restrictions or covenants imposed by leases;

- sublease information, if applicable; and

- leases that have not yet commenced but create significant rights and obligations.

A lessee also discloses significant assumptions and judgments, such as:

- determining whether a contract contains a lease;

- allocating consideration between lease and nonlease components; and

- determining the discount rate.

Quantitative disclosures

For each period presented, a lessee discloses lease cost and cash flow information, including:

- finance lease cost, separated between amortization of right-of-use assets and interest on lease liabilities;

- operating lease cost;

- short-term lease cost;

- variable lease cost;

- sublease income, if applicable;

- gains or losses from sale and leaseback transactions, if applicable;

- cash paid for amounts included in lease liabilities;

- noncash information about lease liabilities arising from obtaining right-of-use assets;

- weighted-average remaining lease term; and

- weighted-average discount rate.

A lessee also discloses a maturity analysis for finance lease liabilities and operating lease liabilities separately. The maturity analysis shows undiscounted cash flows for each of the first five years and a total for the remaining years, along with a reconciliation to the lease liabilities recognized on the balance sheet.

Practical summary

ASC 842 lessee accounting can be summarized through a few practical questions.

Does the contract contain a lease?

Is there identified property, plant, or equipment?

↓

No → no lease

↓

Yes

↓

Does the customer obtain substantially all economic benefits from use?

↓

No → no lease

↓

Yes

↓

Does the customer direct the use of the asset?

↓

No → no lease

↓

Yes → contract contains a leaseIs the lease short-term?

Lease term is 12 months or less?

↓

No → recognize ROU asset and lease liability

↓

Yes

↓

Purchase option reasonably certain to be exercised?

↓

Yes → recognize ROU asset and lease liability

↓

No

↓

Short-term lease election may be applied by class of underlying assetIs the lease finance or operating?

Does ownership transfer?

↓

Yes → finance lease

Is a purchase option reasonably certain to be exercised?

↓

Yes → finance lease

Is the lease term for the major part of remaining economic life?

↓

Yes → finance lease

Do lease payments equal or exceed substantially all fair value?

↓

Yes → finance lease

Is the asset specialized with no expected alternative use to the lessor?

↓

Yes → finance lease

If none apply → operating leaseHow are the lease liability and right-of-use asset measured?

Lease liability

=

Present value of lease payments not yet paid

Right-of-use asset

=

Lease liability

+ payments made at or before commencement

- lease incentives received

+ lessee initial direct costsHow is lease cost recognized?

Finance lease

→ interest on lease liability

→ amortization of right-of-use assets

→ usually front-loaded expense patterns

Operating leases

→ single lease cost

→ generally straight-line expense patternWhere this guide stops

This guide covers the core ASC 842 lessee accounting model: identifying leases, components, lease term, lease payments, discount rate, classification, initial measurement, subsequent measurement, short-term leases, variable payments, remeasurements, modifications, impairment, leasehold improvements, presentation, and disclosure.

It does not cover:

- lessor accounting under ASC 842-30;

- sale and leaseback accounting under ASC 842-40;

- leveraged lease arrangements under ASC 842-50;

- detailed transition guidance;

- detailed sublease accounting;

- detailed related-party or common-control lease accounting;

- build-to-suit arrangements;

- foreign currency lease accounting;

- maintenance deposit accounting beyond the overview level; or

- detailed numerical examples.

ASC 842’s lessee model is often summarized as “put leases on the balance sheet,” but the model is broader than that. The real work is determining whether a contract contains a lease, identifying the lease components, measuring the lease liability and right-of-use asset, and understanding how classification affects the pattern of lease cost recognition.