ASC 718 Stock Compensation — A Concise Guide to the Core Model

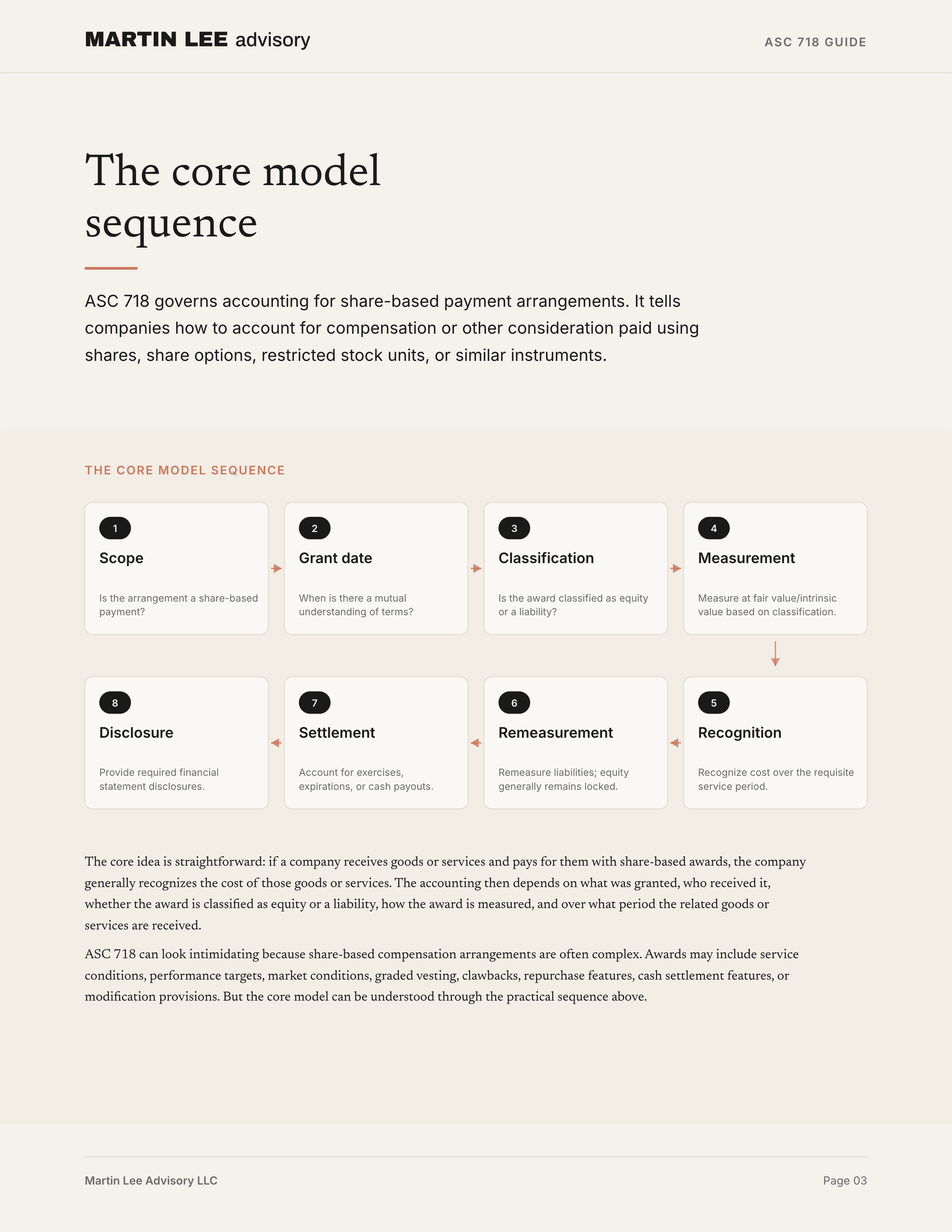

ASC 718 governs accounting for share-based payment arrangements. It tells companies how to account for compensation or other consideration paid using shares, share options, restricted stock units, stock appreciation rights, or similar instruments.

The core idea is straightforward: if a company receives goods or services and pays for them with share-based awards, the company generally recognizes the cost of those goods or services. The accounting then depends on what was granted, who received it, whether the award is classified as equity or a liability, how the award is measured, and over what period the related goods or services are received.

ASC 718 can look intimidating because share-based compensation arrangements are often complex. Awards may include service conditions, performance targets, market conditions, graded vesting, clawbacks, repurchase features, cash settlement features, or modification provisions. But the core model can be understood through a practical sequence:

Scope

↓

Grant date

↓

Classification

↓

Measurement

↓

Recognition period

↓

Subsequent accounting

↓

DisclosureThis guide focuses on that core model.

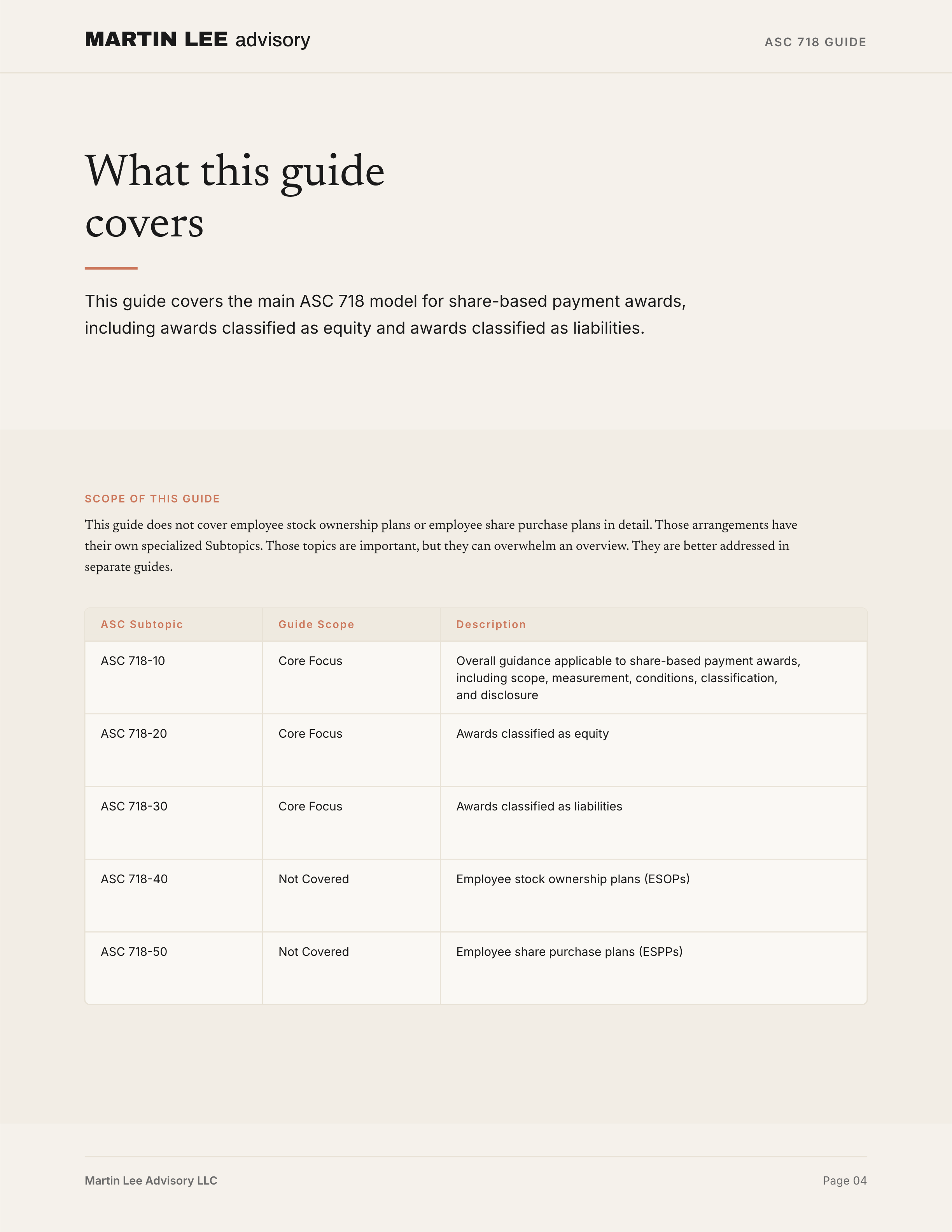

What this guide covers — and what it does not cover

This guide covers the main ASC 718 model for share-based payment awards, including awards classified as equity and awards classified as liabilities.

It focuses primarily on:

- ASC 718-10, Overall

- ASC 718-20, Awards Classified as Equity

- ASC 718-30, Awards Classified as Liabilities

This guide does not cover employee stock ownership plans or employee share purchase plans in detail. Those arrangements have their own specialized Subtopics:

- ASC 718-40, Employee Stock Ownership Plans

- ASC 718-50, Employee Share Purchase Plans

ASC 718-40 covers employer accounting for leveraged and nonleveraged ESOPs, including ESOP debt, suspense shares, committed-to-be-released shares, dividends, EPS, and ESOP-specific disclosures.

ASC 718-50 covers employee share purchase plans, including whether a plan is compensatory or noncompensatory, the 5% discount concept, look-back features, and purchase-period mechanics.

Those topics are important, but they can overwhelm an overview. They are better addressed in separate guides.

The core idea

ASC 718 is not just a valuation standard. It is an accounting model for recognizing the cost of goods or services received in share-based payment arrangements.

The key question is:

What did the company receive, and what share-based award did it provide in exchange?

For employee awards, the company usually receives employee service. For nonemployee awards, the company may receive goods, services, or other consideration. In some cases, share-based awards may also be issued to a customer and evaluated as consideration payable to a customer under ASC 606.

Most ASC 718 accounting starts with a fair-value-based measurement objective. The company measures the award and recognizes compensation cost, or another appropriate asset or expense, as the related goods or services are received.

How ASC 718 is organized

ASC 718 is organized into several Subtopics. The core overview works best if the Subtopics are understood by role:

| Subtopic | What it covers |

|---|---|

| ASC 718-10 | Overall guidance applicable to share-based payment awards, including scope, recognition, measurement, conditions, classification concepts, and disclosure. |

| ASC 718-20 | Awards classified as equity. |

| ASC 718-30 | Awards classified as liabilities. |

| ASC 718-40 | Employee stock ownership plans. |

| ASC 718-50 | Employee share purchase plans. |

For a general overview, the most important split is between equity-classified awards and liability-classified awards.

Equity-classified awards are generally measured at grant-date fair value and are not remeasured after grant date. Liability-classified awards are remeasured at each reporting date through settlement, with changes recognized through compensation cost. ASC 718-20 addresses equity-classified awards, while ASC 718-30 addresses liability-classified awards.

Step 1: Determine whether the arrangement is in scope

The first question is whether the arrangement is a share-based payment arrangement within ASC 718.

ASC 718 generally applies when a company acquires goods or services by issuing share-based awards or by incurring liabilities that are based, at least in part, on the price of the company’s shares or other equity instruments.

Common awards include:

- stock options;

- restricted stock;

- restricted stock units;

- performance shares or performance units;

- stock appreciation rights;

- phantom stock or similar cash-settled awards;

- awards with market or performance conditions; and

- awards issued to nonemployees in exchange for goods or services.

ASC 718 applies to both employee and nonemployee awards, although the attribution of cost for nonemployee awards may differ because the entity recognizes the cost in the same manner as if it had paid cash for the goods or services.

The scope analysis matters because not every equity-related transaction is compensation. Some equity instruments are issued in financing transactions, business combinations, revenue arrangements, or other transactions covered by other GAAP. The company first needs to understand why the award was issued and what the company received in exchange.

Step 2: Identify what the entity is receiving

ASC 718 accounting follows the economics of the exchange. The company identifies what it receives in return for the award.

For employees, the company usually receives service over a vesting period. For nonemployees, the company may receive services, goods, or other benefits. If the award is issued to a customer, the company may need to consider ASC 606’s guidance on consideration payable to a customer.

This matters because the debit side of the entry depends on what the company receives. The award may result in:

- compensation cost;

- an asset, if the goods or services qualify for capitalization under other GAAP; or

- a reduction of revenue, if the award is consideration payable to a customer.

For a basic employee stock option or RSU, the accounting usually results in compensation cost recognized over the service period. For a nonemployee award issued for services related to constructing an asset, the cost may be capitalized if the applicable asset guidance allows capitalization.

Step 3: Determine the grant date

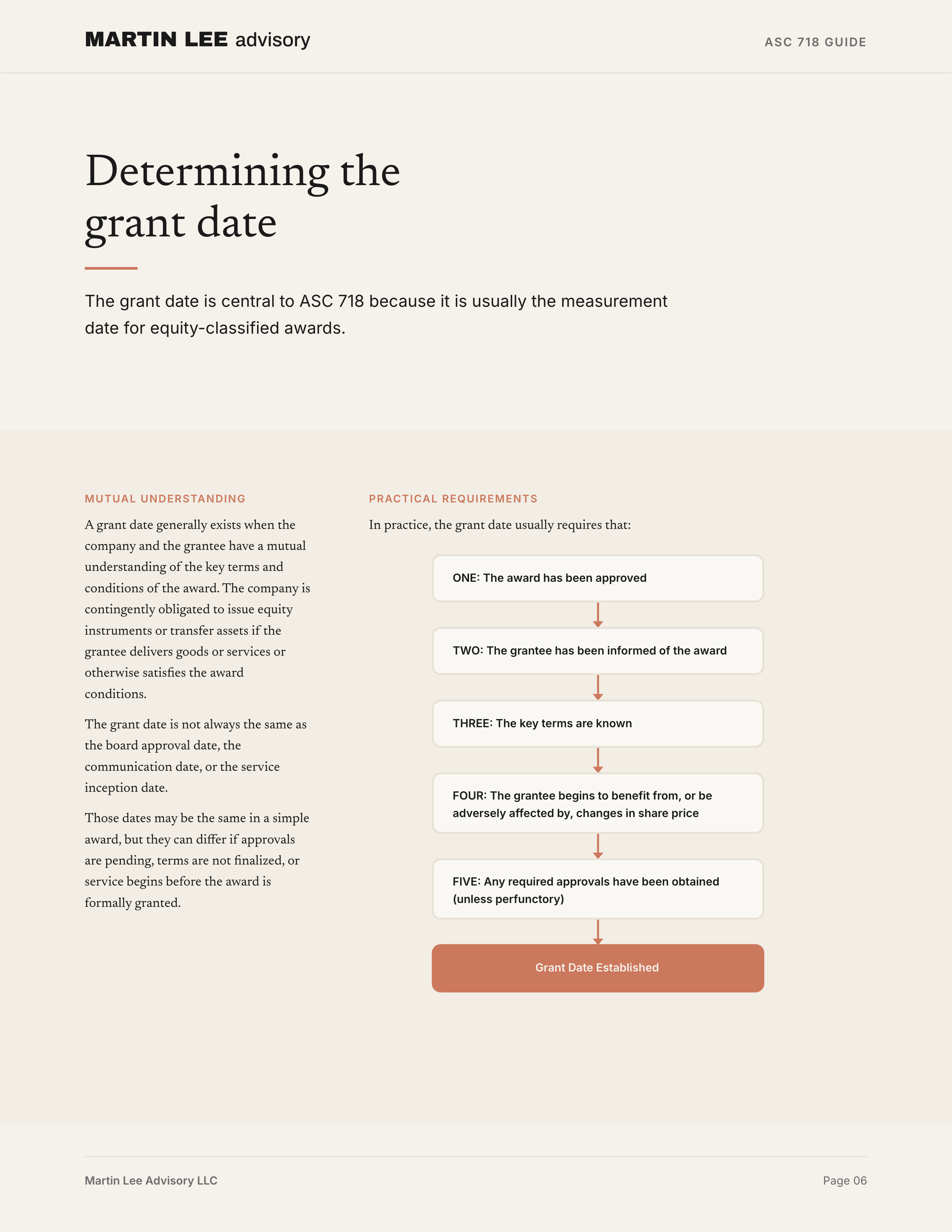

The grant date is central to ASC 718 because it is usually the measurement date for equity-classified awards.

A grant date generally exists when the company and the grantee have a mutual understanding of the key terms and conditions of the award. The company is contingently obligated to issue equity instruments or transfer assets if the grantee delivers goods or services or otherwise satisfies the award conditions.

In practice, the grant date usually requires that:

- the award has been approved;

- the grantee has been informed of the award;

- the key terms are known;

- the grantee begins to benefit from, or be adversely affected by, changes in the company’s share price; and

- any required approvals have been obtained, unless approval is essentially perfunctory.

The grant date is not always the same as the board approval date, the communication date, or the service inception date. Those dates may be the same in a simple award, but they can differ if approvals are pending, terms are not finalized, or service begins before the award is formally granted.

Step 4: Classify the award as equity or liability

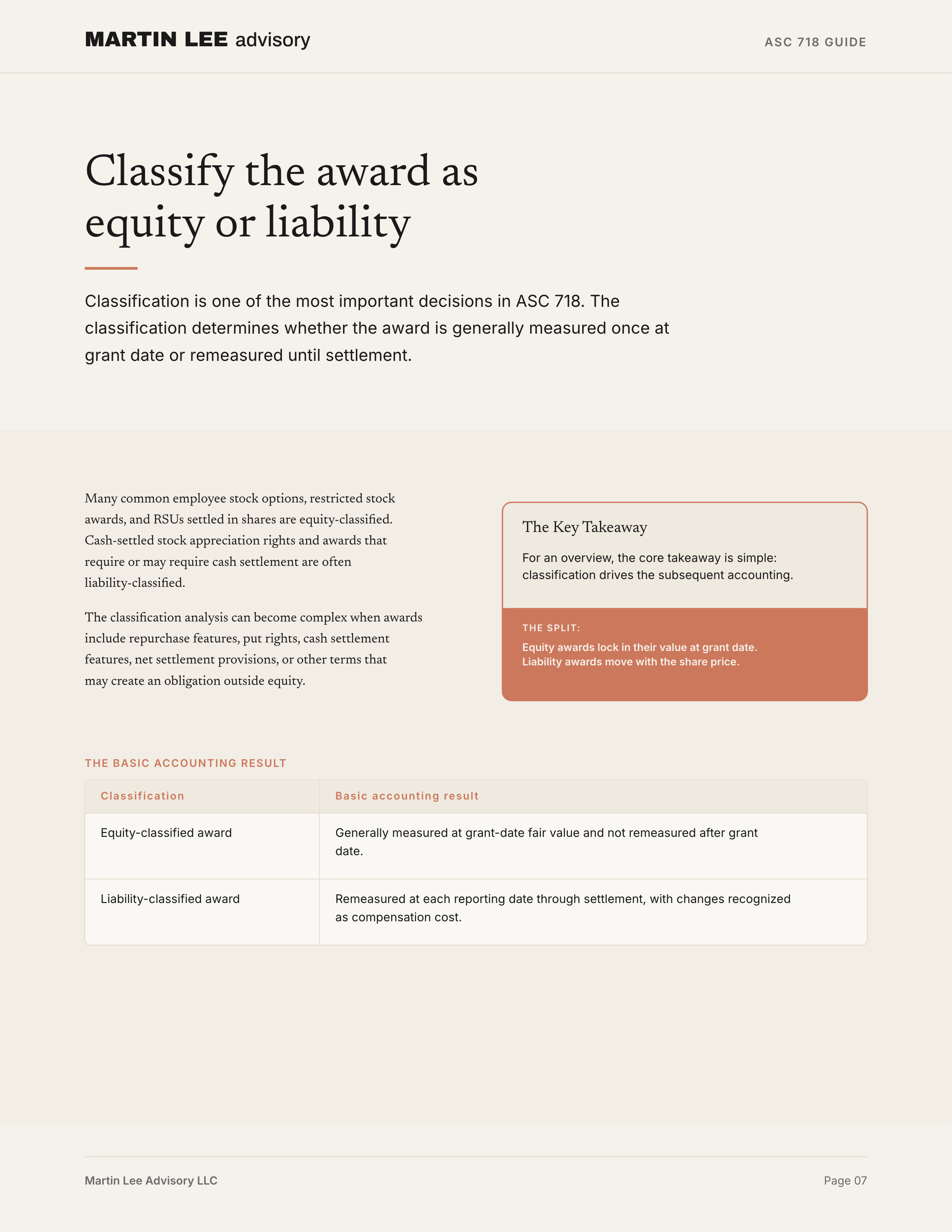

Classification is one of the most important decisions in ASC 718.

The classification determines whether the award is generally measured once at grant date or remeasured until settlement.

| Classification | Basic accounting result |

|---|---|

| Equity-classified award | Generally measured at grant-date fair value and not remeasured after grant date. |

| Liability-classified award | Remeasured at each reporting date through settlement, with changes recognized as compensation cost. |

Many common employee stock options, restricted stock awards, and RSUs settled in shares are equity-classified. Cash-settled stock appreciation rights and awards that require or may require cash settlement are often liability-classified.

The classification analysis can become complex when awards include repurchase features, put rights, cash settlement features, net settlement provisions, or other terms that may create an obligation outside equity. For an overview, the key takeaway is simple: classification drives subsequent accounting.

Step 5: Measure the award

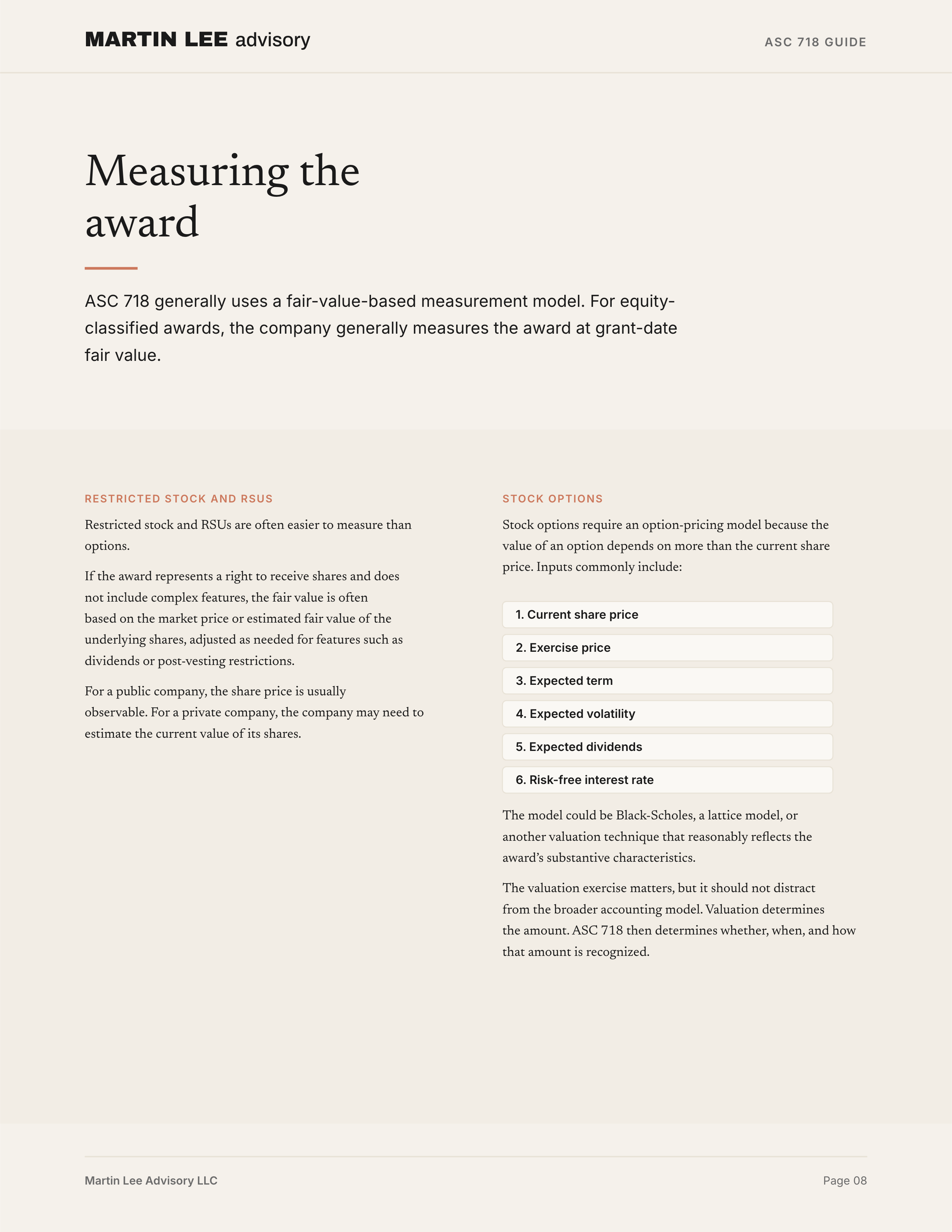

ASC 718 generally uses a fair-value-based measurement model.

For equity-classified awards, the company generally measures the award at grant-date fair value. For liability-classified awards, the award is measured and remeasured at fair value, or in some cases intrinsic value for certain nonpublic entities, through settlement.

The measurement approach depends on the award.

Restricted stock and RSUs

Restricted stock and RSUs are often easier to measure than options. If the award represents a right to receive shares and does not include complex features, the fair value is often based on the market price or estimated fair value of the underlying shares, adjusted as needed for features such as dividends or post-vesting restrictions.

For a public company, the share price is usually observable. For a private company, the company may need to estimate the current value of its shares.

Stock options

Stock options require an option-pricing model because the value of an option depends on more than the current share price. Inputs commonly include:

- current share price;

- exercise price;

- expected term;

- expected volatility;

- expected dividends; and

- risk-free interest rate.

The model could be Black-Scholes, a lattice model, or another valuation technique that reasonably reflects the award’s substantive characteristics.

The valuation exercise matters, but it should not distract from the broader accounting model. Valuation determines the amount. ASC 718 then determines whether, when, and how that amount is recognized.

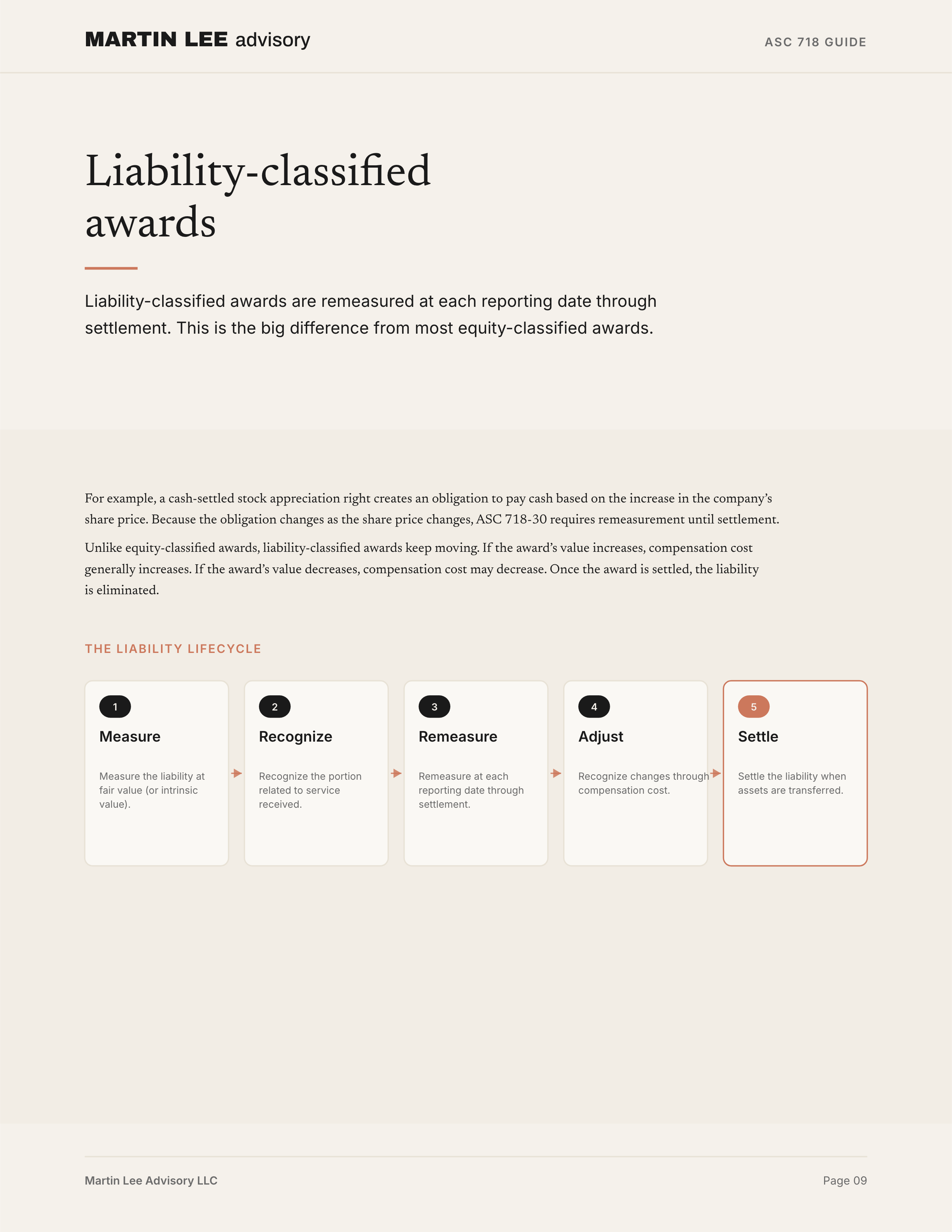

Liability awards

Liability-classified awards are remeasured at each reporting date through settlement. This is the big difference from most equity-classified awards.

For example, a cash-settled stock appreciation right creates an obligation to pay cash based on the increase in the company’s share price. Because the obligation changes as the share price changes, ASC 718-30 requires remeasurement until settlement. Changes in fair value, or intrinsic value if a qualifying nonpublic entity elects that method, are recognized as compensation cost.

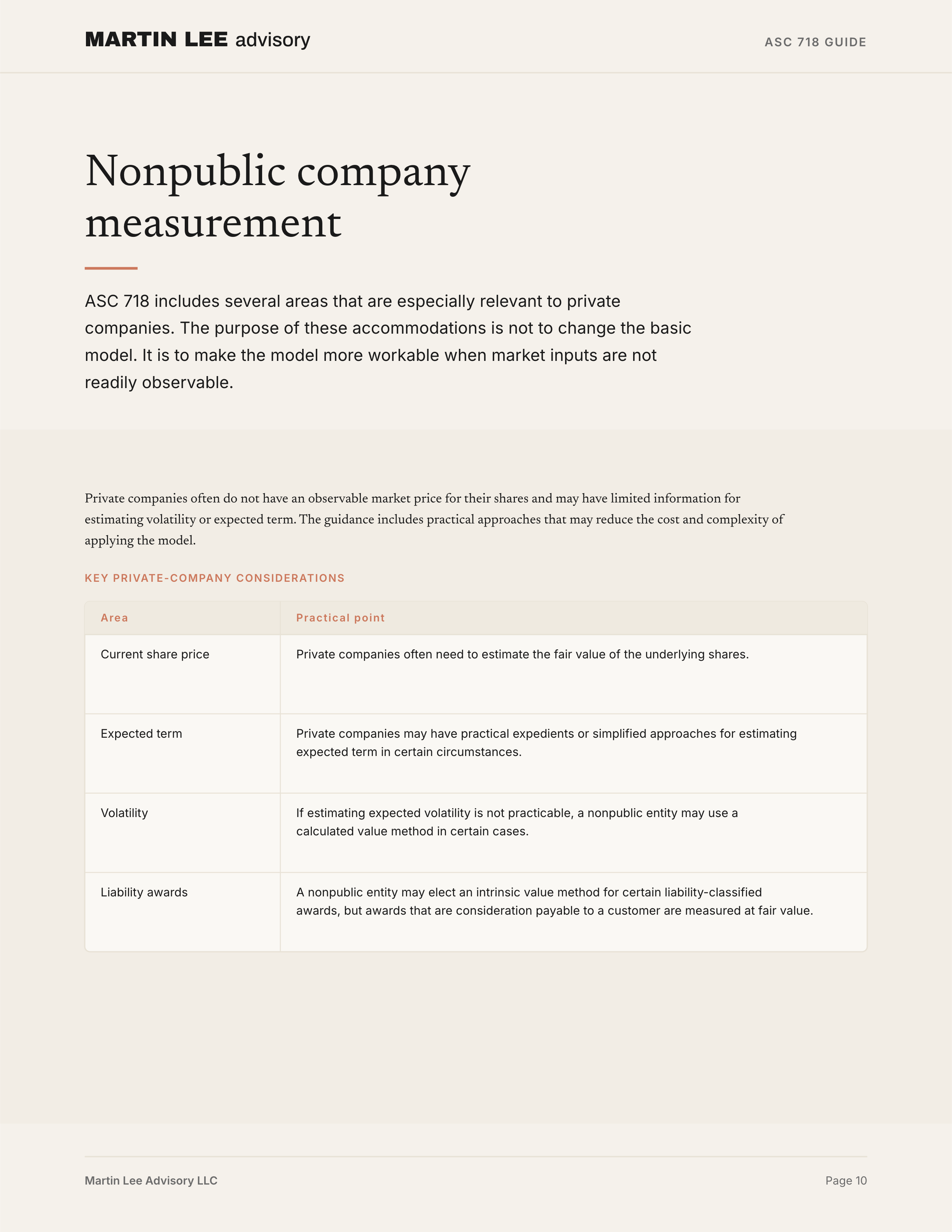

Nonpublic company measurement considerations

ASC 718 includes several areas that are especially relevant to private companies.

Private companies often do not have an observable market price for their shares and may have limited information for estimating volatility or expected term. The guidance includes practical approaches that may reduce the cost and complexity of applying the model.

Key private-company considerations include:

| Area | Practical point |

|---|---|

| Current share price | Private companies often need to estimate the fair value of the underlying shares. |

| Expected term | Private companies may have practical expedients or simplified approaches for estimating expected term in certain circumstances. |

| Volatility | If estimating expected volatility is not practicable, a nonpublic entity may use a calculated value method in certain cases. |

| Liability awards | A nonpublic entity may elect an intrinsic value method for certain liability-classified awards, but awards that are consideration payable to a customer are measured at fair value. |

The purpose of these accommodations is not to change the basic model. It is to make the model more workable when market inputs are not readily observable.

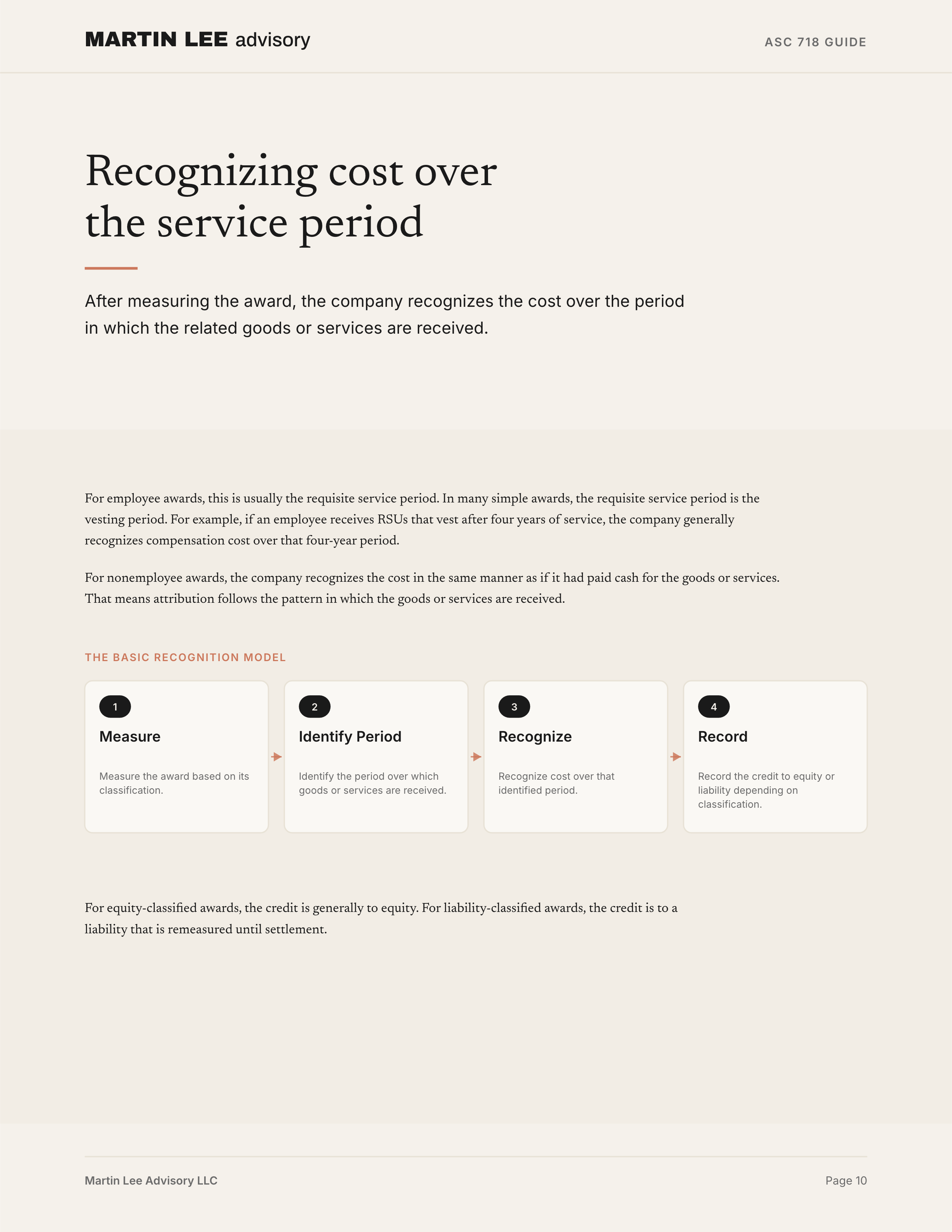

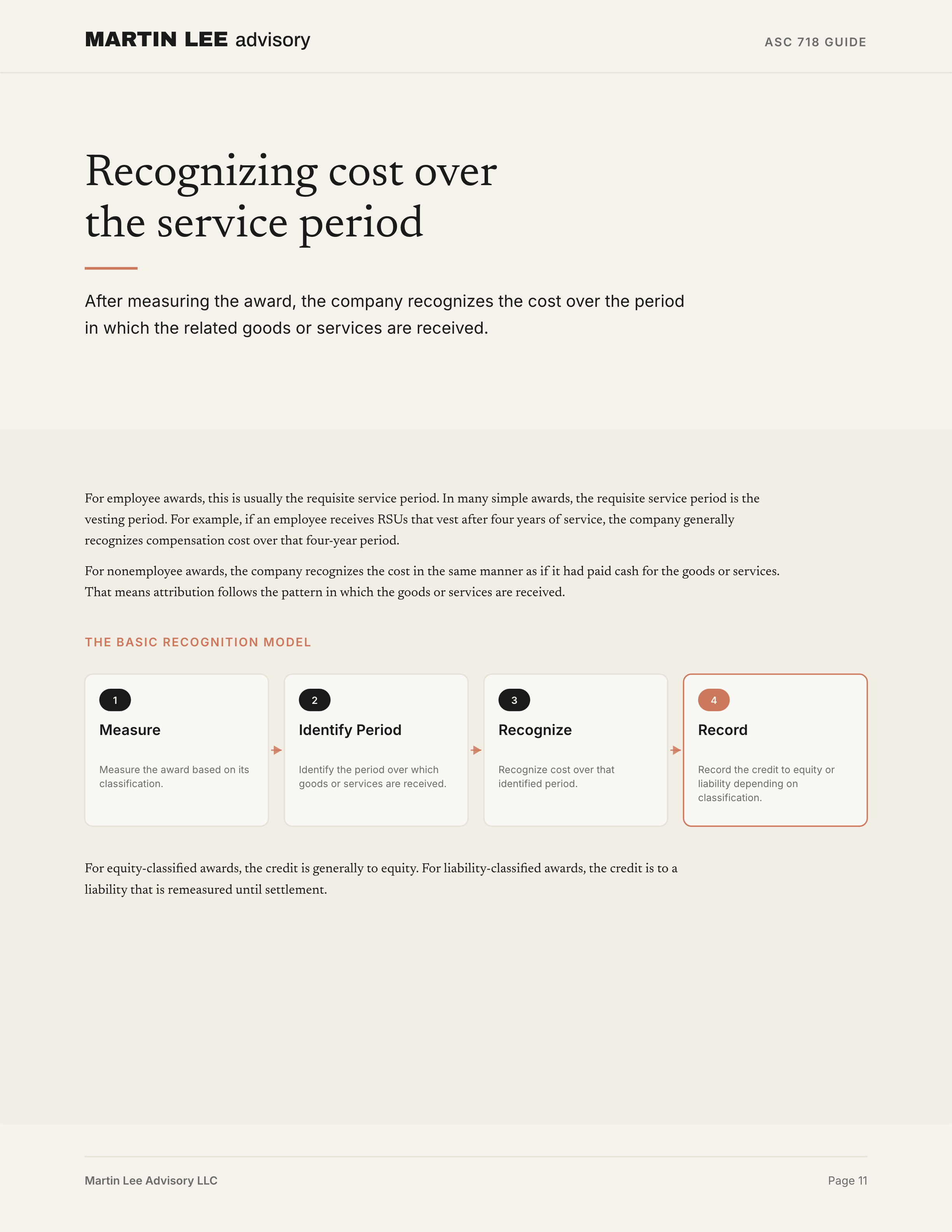

Step 6: Recognize compensation cost over the service period

After measuring the award, the company recognizes the cost over the period in which the related goods or services are received.

For employee awards, this is usually the requisite service period. In many simple awards, the requisite service period is the vesting period. For example, if an employee receives RSUs that vest after four years of service, the company generally recognizes compensation cost over that four-year period.

For nonemployee awards, the company recognizes the cost in the same manner as if it had paid cash for the goods or services. That means attribution follows the pattern in which the goods or services are received.

The basic recognition model is:

Measure the award

↓

Identify the period over which goods or services are received

↓

Recognize cost over that period

↓

Record the credit to equity or liability depending on classificationFor equity-classified awards, the credit is generally to equity. For liability-classified awards, the credit is to a liability that is remeasured until settlement.

Service, performance, and market conditions

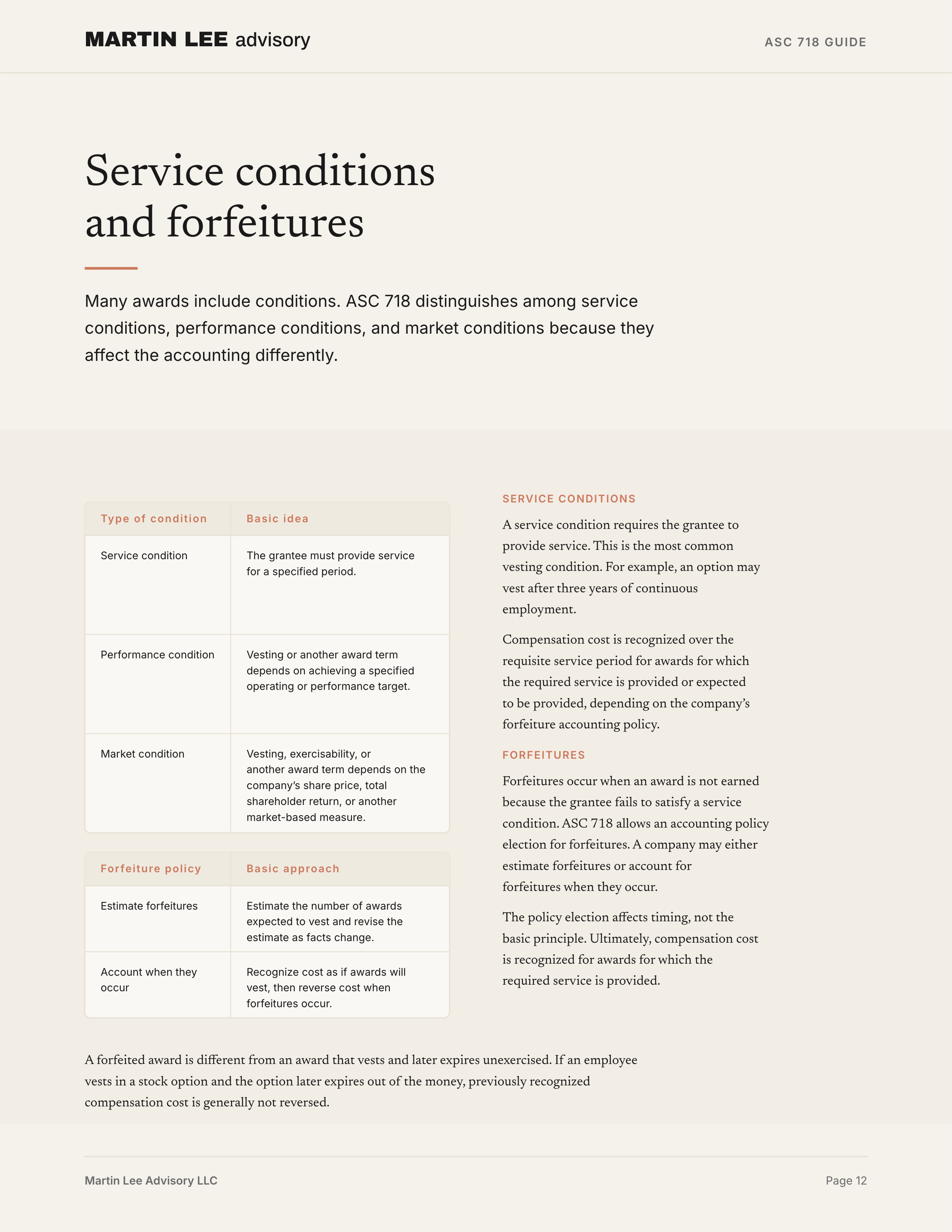

Many awards include conditions. ASC 718 distinguishes among service conditions, performance conditions, and market conditions because they affect the accounting differently.

| Type of condition | Basic idea |

|---|---|

| Service condition | The grantee must provide service for a specified period. |

| Performance condition | Vesting or another award term depends on achieving a specified operating or performance target. |

| Market condition | Vesting, exercisability, or another award term depends on the company’s share price, total shareholder return, or another market-based measure. |

Service conditions

A service condition requires the grantee to provide service. This is the most common vesting condition.

For example, an option may vest after three years of continuous employment. Compensation cost is recognized over the requisite service period for awards for which the required service is provided or expected to be provided, depending on the company’s forfeiture accounting policy.

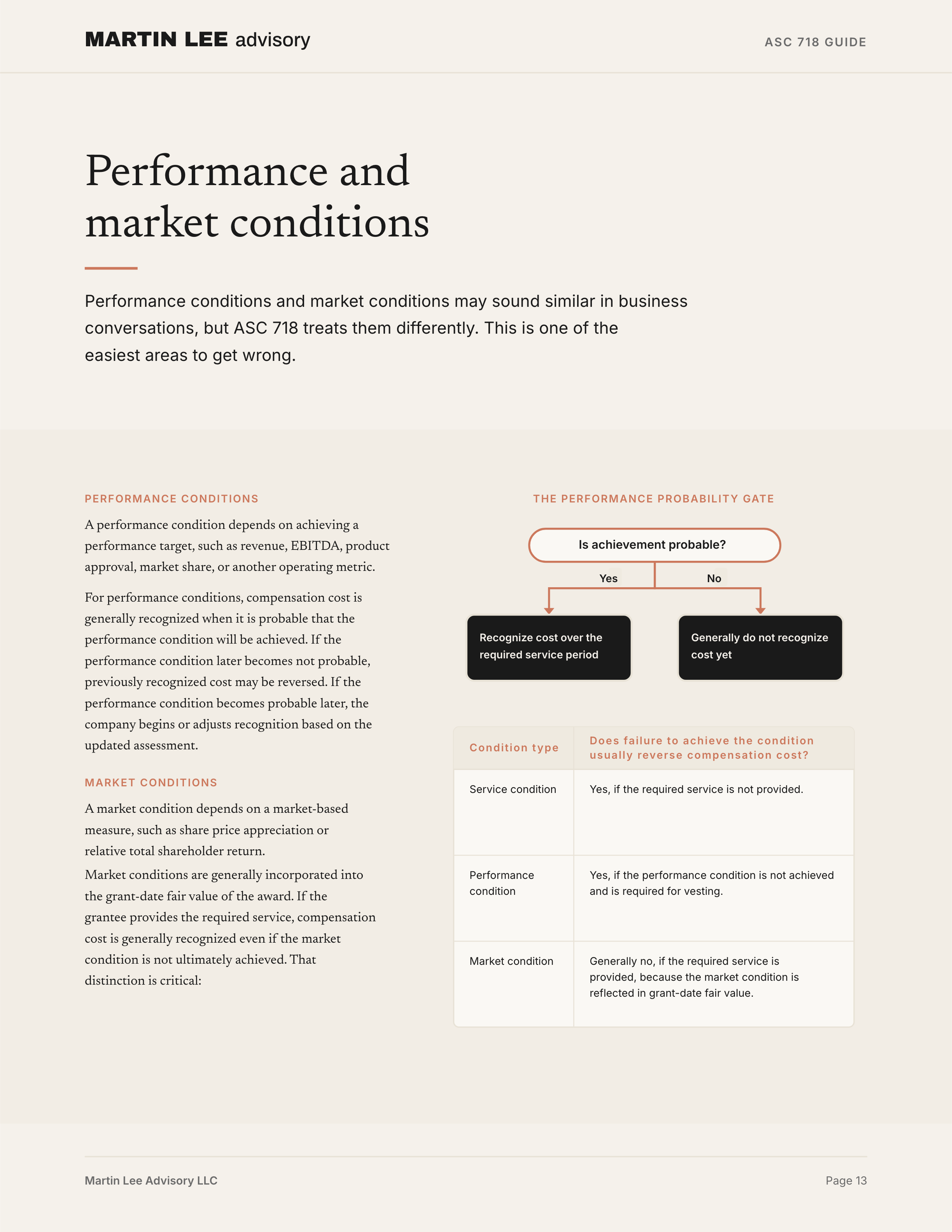

Performance conditions

A performance condition depends on achieving a performance target, such as revenue, EBITDA, product approval, market share, or another operating metric.

For performance conditions, compensation cost is generally recognized when it is probable that the performance condition will be achieved. If the performance condition later becomes not probable, previously recognized cost may be reversed. If the performance condition becomes probable later, the company begins or adjusts recognition based on the updated assessment.

A practical way to think about performance conditions is:

Is achievement probable?

↓

No → generally do not recognize cost yet

↓

Yes → recognize cost over the required service periodThis is different from a market condition.

Market conditions

A market condition depends on a market-based measure, such as share price appreciation or relative total shareholder return.

Market conditions are generally incorporated into the grant-date fair value of the award. If the grantee provides the required service, compensation cost is generally recognized even if the market condition is not ultimately achieved.

That distinction is critical:

| Condition type | Does failure to achieve the condition usually reverse compensation cost? |

|---|---|

| Service condition | Yes, if the required service is not provided. |

| Performance condition | Yes, if the performance condition is not achieved and is required for vesting. |

| Market condition | Generally no, if the required service is provided, because the market condition is reflected in grant-date fair value. |

This is one of the easiest areas to get wrong. Performance conditions and market conditions may sound similar in business conversations, but ASC 718 treats them differently.

Forfeitures

Forfeitures occur when an award is not earned because the grantee fails to satisfy a service condition.

ASC 718 allows an accounting policy election for forfeitures. A company may either estimate forfeitures or account for forfeitures when they occur.

| Forfeiture policy | Basic approach |

|---|---|

| Estimate forfeitures | Estimate the number of awards expected to vest and revise the estimate as facts change. |

| Account for forfeitures when they occur | Recognize cost as if awards will vest, then reverse cost when forfeitures occur. |

The policy election affects timing, not the basic principle. Ultimately, compensation cost is recognized for awards for which the required service is provided.

A forfeited award is different from an award that vests and later expires unexercised. If an employee vests in a stock option and the option later expires out of the money, previously recognized compensation cost is generally not reversed.

Equity-classified awards

Equity-classified awards are the most common awards in many compensation plans. They include many stock options, restricted stock awards, and RSUs that settle in shares.

The basic accounting model is:

Measure at grant-date fair value

↓

Recognize compensation cost over the requisite service period

↓

Credit equity

↓

Generally do not remeasure after grant dateASC 718-20 addresses awards classified as equity. The Subtopic is closely connected to ASC 718-10, which contains guidance applicable to both equity-classified and liability-classified awards.

For a typical equity-classified award, changes in the company’s share price after grant date do not change the amount of compensation cost recognized. That is true even if the award later becomes deeply out of the money, provided the required service is rendered and the award otherwise vests.

That can feel counterintuitive, especially for stock options. But the accounting model measures the cost at grant date and recognizes that cost as the related service is provided. It does not remeasure the award each period simply because the company’s share price changes.

Liability-classified awards

Liability-classified awards are accounted for differently because the company has an obligation that changes in value.

ASC 718-30 addresses share-based payment awards classified as liabilities. For public entities, liability awards are measured at fair value and remeasured at each reporting date until settlement. For nonpublic entities, certain liability awards may be measured at fair value or intrinsic value as an accounting policy election, although awards that are consideration payable to a customer are measured at fair value.

The basic model is:

Measure the liability

↓

Recognize the portion related to service received

↓

Remeasure at each reporting date

↓

Recognize changes in compensation cost

↓

Continue until settlementUnlike equity-classified awards, liability-classified awards keep moving. If the award’s value increases, compensation cost generally increases. If the award’s value decreases, compensation cost may decrease. Once the award is settled, the liability is eliminated.

This is the core contrast:

| Issue | Equity-classified award | Liability-classified award |

|---|---|---|

| Measurement date | Generally grant date | Settlement date |

| Remeasurement | Generally no | Yes, each reporting period through settlement |

| Credit side | Equity | Liability |

| Effect of share price changes after grant | Generally no remeasurement | Reflected in liability and compensation cost |

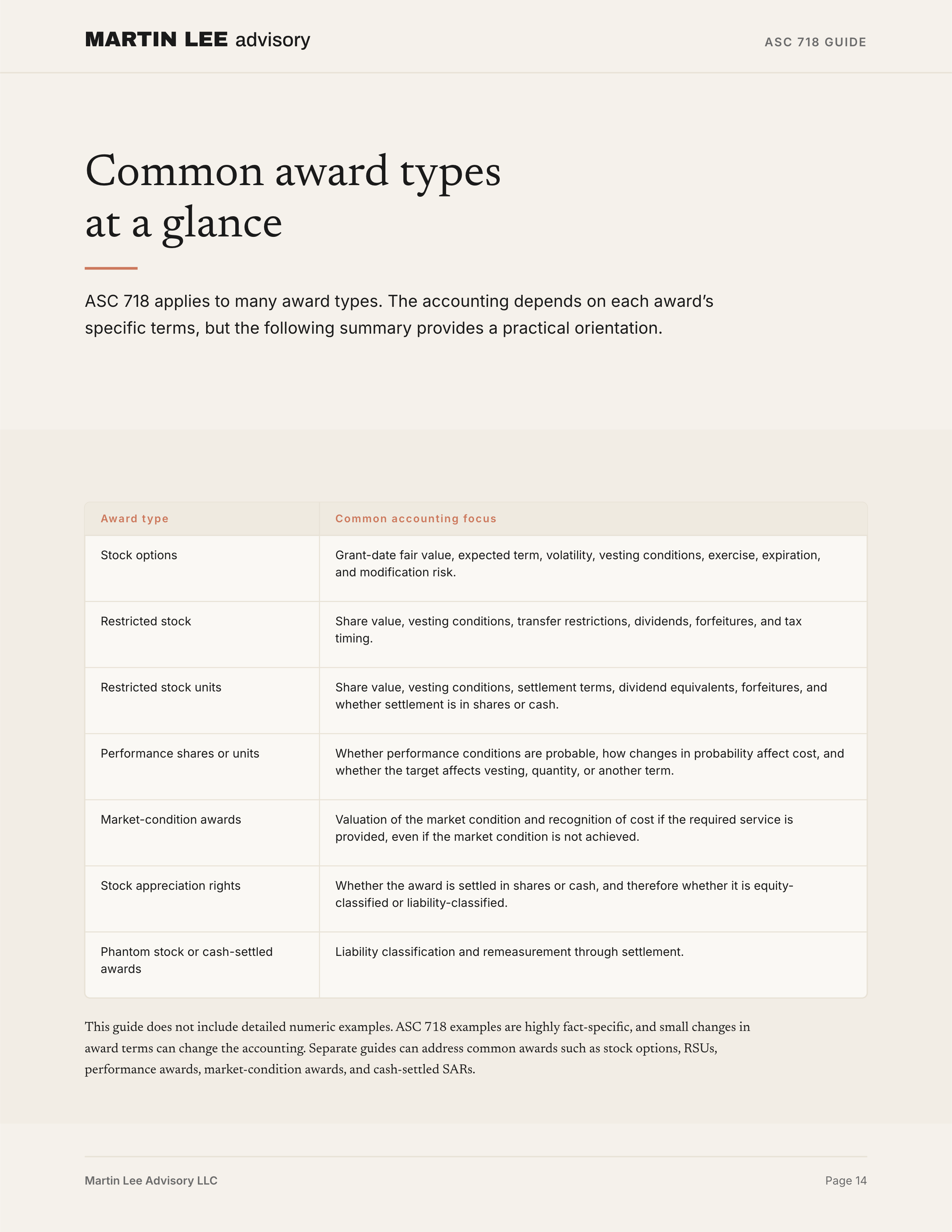

Common award types at a glance

ASC 718 applies to many award types. The accounting depends on each award’s specific terms, but the following summary provides a practical orientation.

| Award type | Common accounting focus |

|---|---|

| Stock options | Grant-date fair value, expected term, volatility, vesting conditions, exercise, expiration, and modification risk. |

| Restricted stock | Share value, vesting conditions, transfer restrictions, dividends, forfeitures, and tax timing. |

| Restricted stock units | Share value, vesting conditions, settlement terms, dividend equivalents, forfeitures, and whether settlement is in shares or cash. |

| Performance shares or units | Whether performance conditions are probable, how changes in probability affect cost, and whether the target affects vesting, quantity, or another term. |

| Market-condition awards | Valuation of the market condition and recognition of cost if the required service is provided, even if the market condition is not achieved. |

| Stock appreciation rights | Whether the award is settled in shares or cash, and therefore whether it is equity-classified or liability-classified. |

| Phantom stock or cash-settled awards | Liability classification and remeasurement through settlement. |

This guide does not include detailed numeric examples. ASC 718 examples are highly fact-specific, and small changes in award terms can change the accounting. Separate guides can address common awards such as stock options, RSUs, performance awards, market-condition awards, and cash-settled SARs.

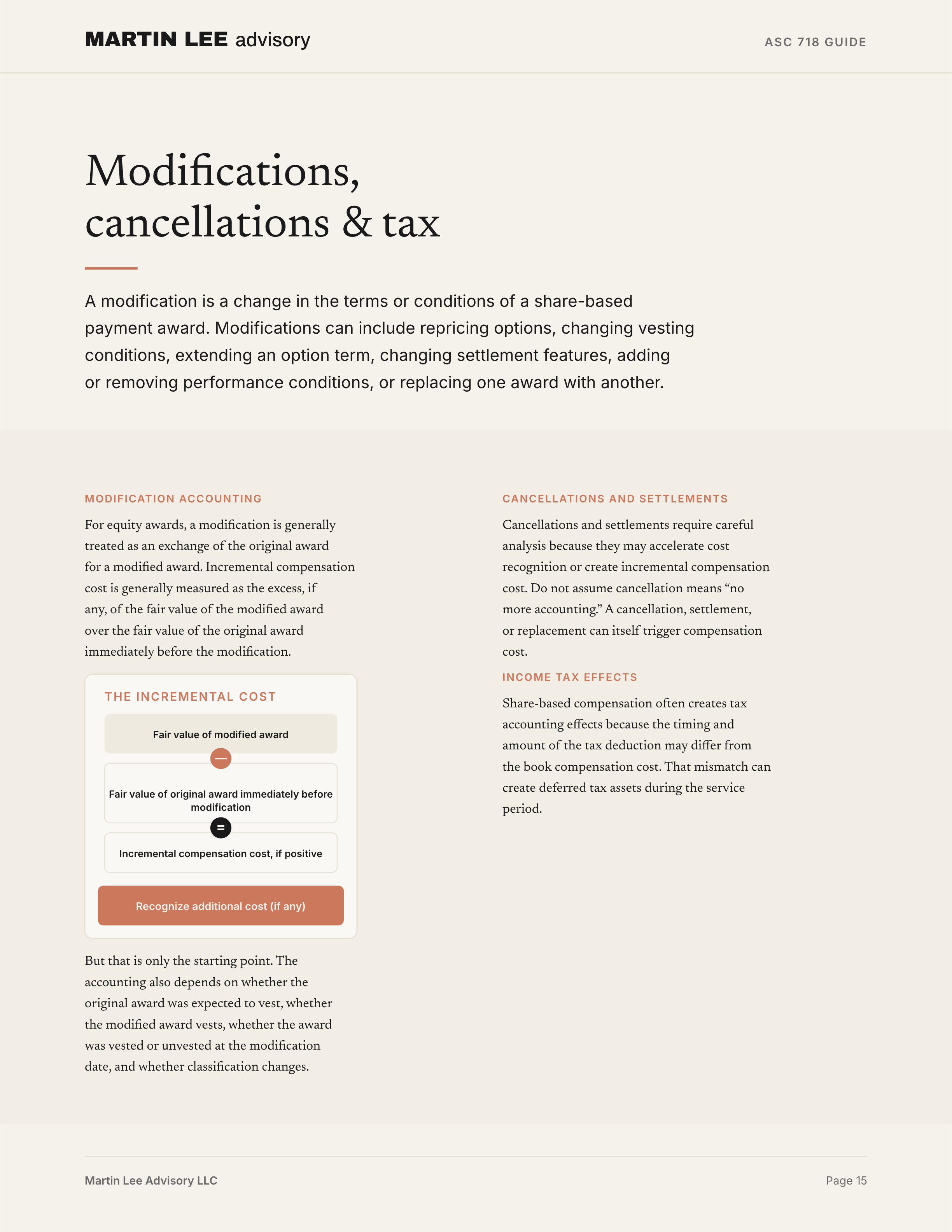

Modifications, cancellations, and settlements

A modification is a change in the terms or conditions of a share-based payment award.

Modifications can include repricing options, changing vesting conditions, extending an option term, changing settlement features, adding or removing performance conditions, or replacing one award with another.

For equity awards, a modification is generally treated as an exchange of the original award for a modified award. Incremental compensation cost is generally measured as the excess, if any, of the fair value of the modified award over the fair value of the original award immediately before the modification.

In simplified form:

Fair value of modified award

minus

Fair value of original award immediately before modification

=

Incremental compensation cost, if positiveBut that is only the starting point. The accounting also depends on whether the original award was expected to vest, whether the modified award vests, whether the award was vested or unvested at the modification date, and whether classification changes.

ASC 718 also includes relief from modification accounting in certain cases. If a modification does not change the award’s fair value, vesting conditions, or classification, the company may not need to apply full modification accounting, although disclosure requirements still apply.

For liability awards, modifications are generally less dramatic from a measurement perspective because the award is already remeasured at each reporting date. ASC 718-30 notes that because liability awards are remeasured at fair value, or intrinsic value for a qualifying nonpublic entity that elects that method, no special guidance is generally necessary when a liability award remains a liability after modification.

Modifications are a good example of why ASC 718 deserves focused add-on guides. The core idea is understandable, but the detailed outcomes can vary significantly.

Cancellations and settlements

Cancellations and settlements require careful analysis because they may accelerate cost recognition or create incremental compensation cost.

For equity awards, a repurchase or settlement is generally evaluated by comparing the consideration transferred to the fair value of the award repurchased or settled. If the company pays more than fair value, the excess is generally additional compensation cost. If an unvested award is repurchased or effectively vested through settlement, previously unrecognized compensation cost may need to be recognized immediately.

A cancellation with a concurrent replacement award is generally treated as a modification. A cancellation without a replacement award is generally treated as a repurchase for no consideration, which can result in recognition of previously unrecognized compensation cost at the cancellation date.

For an overview, the practical takeaway is:

Do not assume cancellation means “no more accounting.”

A cancellation, settlement, or replacement can itself trigger compensation cost.Income tax effects — short practical overview

Share-based compensation often creates tax accounting effects because the timing and amount of the tax deduction may differ from the book compensation cost.

For book purposes, compensation cost is often recognized over the service period based on grant-date fair value. For tax purposes, the deduction may occur later, such as when an option is exercised or restricted stock vests. The tax deduction may also be based on intrinsic value at that later date rather than the grant-date fair value used for book purposes.

That mismatch can create deferred tax assets during the service period. When the tax deduction occurs, the company compares the tax benefit from the actual deduction with the deferred tax asset recorded for book purposes. Differences affect income tax expense or benefit.

A simple way to think about the tax model is:

Book compensation cost recognized over service period

↓

Deferred tax asset recognized if deductible for tax purposes in the future

↓

Tax deduction occurs later, often at exercise or vesting

↓

Difference between actual tax benefit and recorded deferred tax asset

affects income tax expense or benefitThis guide keeps the tax discussion short because ASC 718 tax accounting can become its own topic quickly. The key point is that book compensation cost and tax deductions often differ in timing and amount.

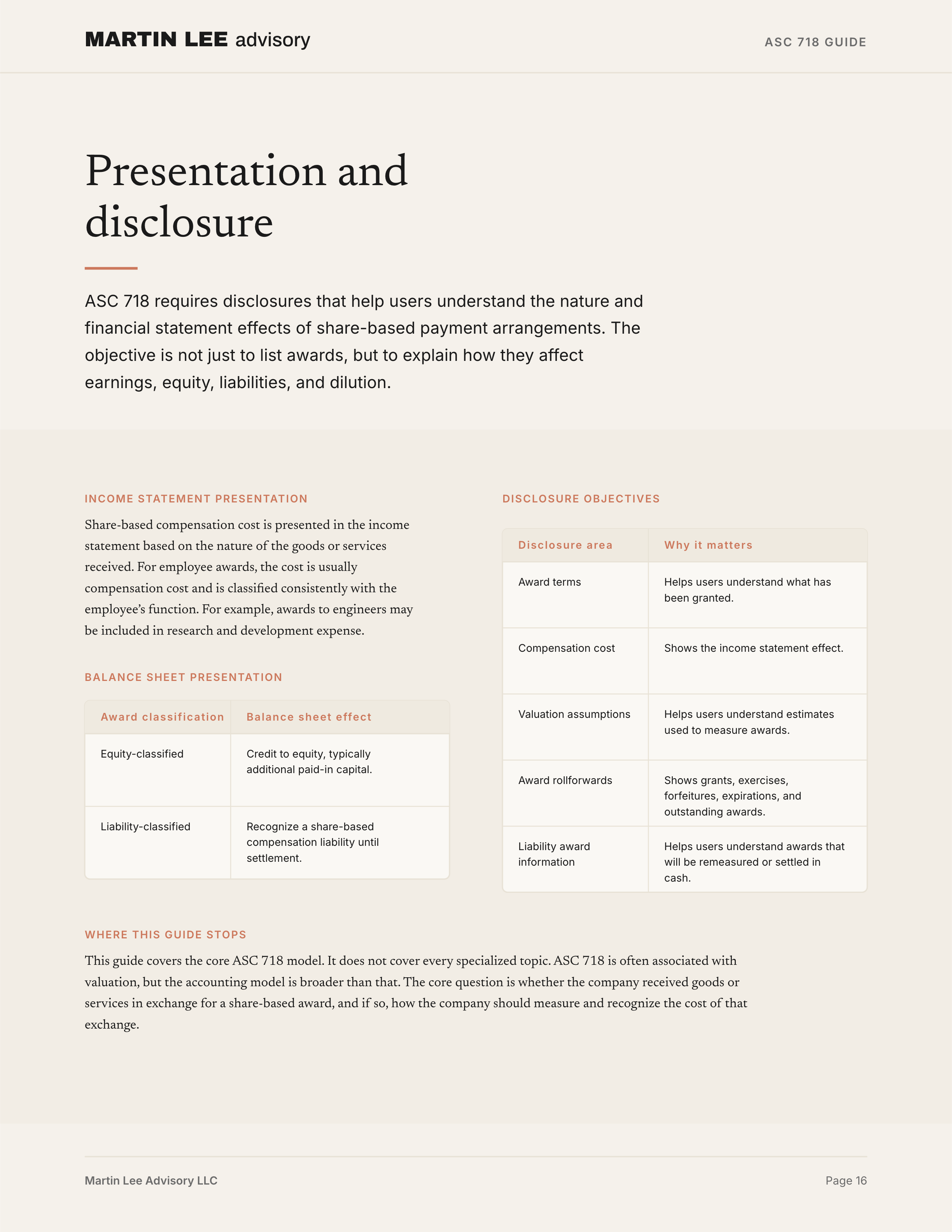

Presentation

Share-based compensation cost is presented in the income statement based on the nature of the goods or services received.

For employee awards, the cost is usually compensation cost and is classified consistently with the employee’s function. For example, awards to engineers may be included in research and development expense, while awards to sales personnel may be included in sales and marketing expense.

If the share-based payment relates to goods or services that qualify for capitalization under other GAAP, the cost may be capitalized as part of an asset rather than immediately expensed.

The balance sheet presentation depends on classification.

| Award classification | Balance sheet effect |

|---|---|

| Equity-classified | Credit to equity, typically additional paid-in capital. |

| Liability-classified | Recognize a share-based compensation liability until settlement. |

Cash flow presentation depends on the nature of the transaction and related tax effects, and may require separate analysis.

Disclosure

ASC 718 requires disclosures that help users understand the nature and financial statement effects of share-based payment arrangements.

The disclosures generally explain:

- the nature and terms of share-based payment arrangements;

- the effect of compensation cost on the income statement;

- how fair value was measured;

- key valuation assumptions;

- award activity during the period;

- information about options outstanding and exercisable;

- total intrinsic value of awards exercised or outstanding, where applicable;

- cash received from option exercises;

- tax benefits realized; and

- information about liabilities from share-based payment awards, if applicable.

The disclosure objective is not just to list awards. Users should be able to understand how share-based compensation affects earnings, equity, liabilities, and future dilution.

For an overview, the most important disclosure categories are:

| Disclosure area | Why it matters |

|---|---|

| Award terms | Helps users understand what has been granted. |

| Compensation cost | Shows the income statement effect. |

| Valuation assumptions | Helps users understand estimates used to measure awards. |

| Award rollforwards | Shows grants, exercises, forfeitures, expirations, and outstanding awards. |

| Liability award information | Helps users understand awards that will be remeasured or settled in cash. |

Practical summary

ASC 718 can be summarized through a few practical questions.

Core model

Is the arrangement a share-based payment for goods or services?

↓

No → consider other GAAP

↓

Yes

↓

Who is the grantee and what is the company receiving?

↓

Determine grant date

↓

Classify the award as equity or liability

↓

Measure the award

↓

Recognize cost as goods or services are received

↓

Apply subsequent accounting based on classificationEquity versus liability

Is the award equity-classified?

↓

Yes → generally measure at grant-date fair value

↓

Recognize cost over the requisite service period

↓

Generally do not remeasure after grant dateIs the award liability-classified?

↓

Yes → remeasure at each reporting date until settlement

↓

Recognize changes through compensation cost

↓

Settle the liability when cash or other assets are transferredConditions

Service condition

→ recognize cost for awards for which service is provided

Performance condition

→ recognize cost when achievement is probable

→ reverse if the condition is not achieved and the award does not vest

Market condition

→ include in grant-date fair value

→ generally do not reverse cost solely because the market condition is not achieved

if the required service is providedWhere this guide stops

This guide covers the core ASC 718 model: scope, grant date, classification, measurement, recognition, service/performance/market conditions, forfeitures, equity awards, liability awards, modifications, income tax effects, presentation, disclosure, and common award types.

It does not cover every specialized topic in ASC 718.

Topics that deserve separate focused guides include:

- equity versus liability classification;

- stock option valuation;

- private-company practical expedients;

- RSUs and restricted stock;

- performance awards and market-condition awards;

- modifications, cancellations, and settlements;

- cash-settled awards and stock appreciation rights;

- income tax effects of share-based compensation;

- employee share purchase plans under ASC 718-50; and

- employee stock ownership plans under ASC 718-40.

ASC 718 is often associated with valuation, but the accounting model is broader than that. The core question is whether the company received goods or services in exchange for a share-based award, and if so, how the company should measure and recognize the cost of that exchange.