ASC 805 Business Combinations — A Concise Guide to the Acquisition Method

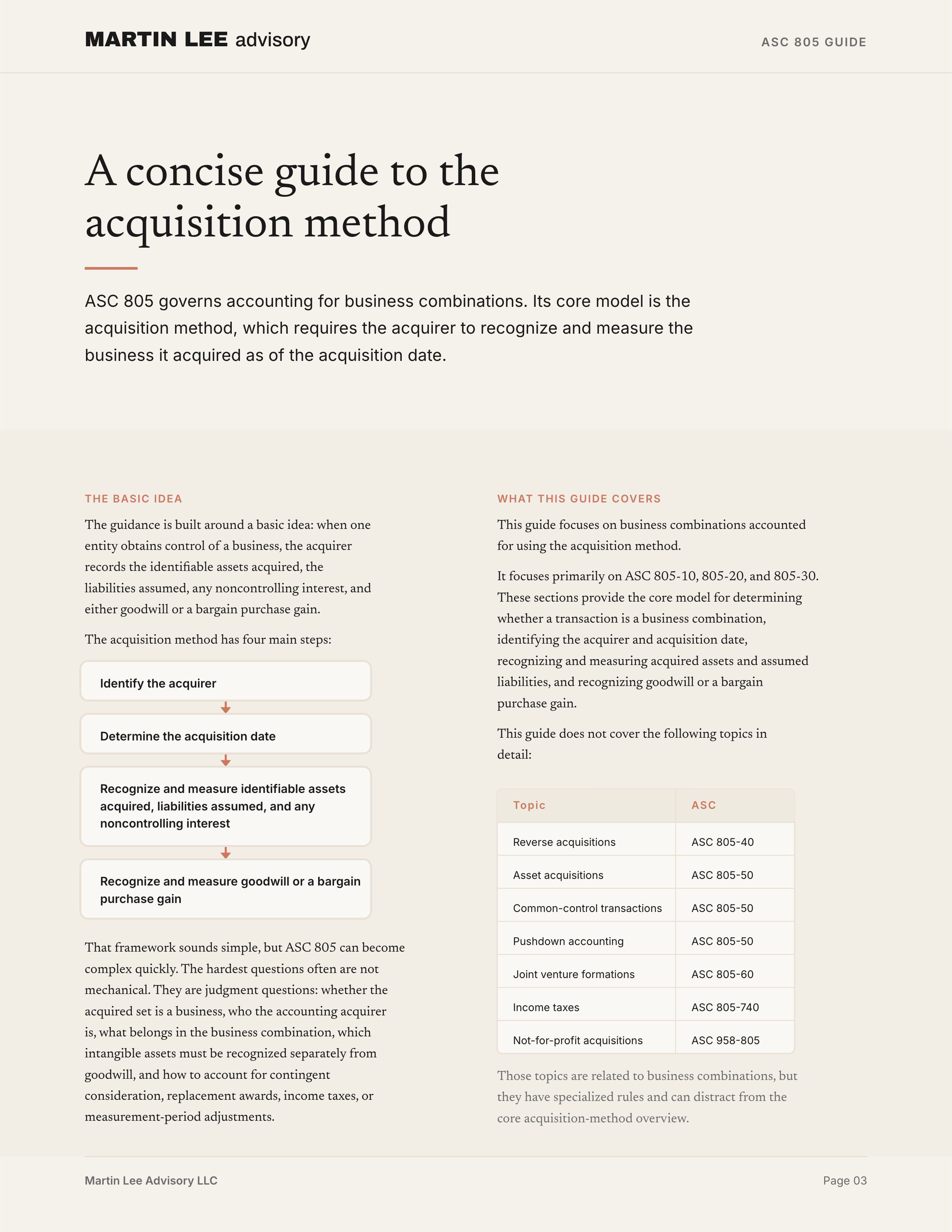

ASC 805 governs accounting for business combinations. Its core model is the acquisition method, which requires the acquirer to recognize and measure the business it acquired as of the acquisition date.

The guidance is built around a basic idea: when one entity obtains control of a business, the acquirer records the identifiable assets acquired, the liabilities assumed, any noncontrolling interest, and either goodwill or a bargain purchase gain.

The acquisition method has four main steps:

Identify the acquirer

↓

Determine the acquisition date

↓

Recognize and measure identifiable assets acquired,

liabilities assumed, and any noncontrolling interest

↓

Recognize and measure goodwill or a bargain purchase gainThat framework sounds simple, but ASC 805 can become complex quickly. The hardest questions often are not mechanical. They are judgment questions: whether the acquired set is a business, who the accounting acquirer is, what belongs in the business combination, which intangible assets must be recognized separately from goodwill, and how to account for contingent consideration, replacement awards, income taxes, or measurement-period adjustments.

This guide focuses on the core acquisition-method model.

What this guide covers — and what it does not cover

This guide focuses on business combinations accounted for using the acquisition method.

It focuses primarily on:

- ASC 805-10, Overall

- ASC 805-20, Identifiable Assets and Liabilities, and Any Noncontrolling Interest

- ASC 805-30, Goodwill or Gain from Bargain Purchase, Including Consideration Transferred

Those Subtopics provide the core model for determining whether a transaction is a business combination, identifying the acquirer and acquisition date, recognizing and measuring acquired assets and assumed liabilities, and recognizing goodwill or a bargain purchase gain.

This guide does not cover the following topics in detail:

| Topic | Primary guidance |

|---|---|

| Reverse acquisitions | ASC 805-40 |

| Asset acquisitions | ASC 805-50 |

| Common-control transactions | ASC 805-50 |

| Pushdown accounting | ASC 805-50 |

| Joint venture formations | ASC 805-60 |

| Income taxes in business combinations | ASC 805-740 |

| Not-for-profit acquisition guidance | ASC 958-805 |

Those topics are related to business combinations, but they have specialized rules and can distract from the core acquisition-method overview.

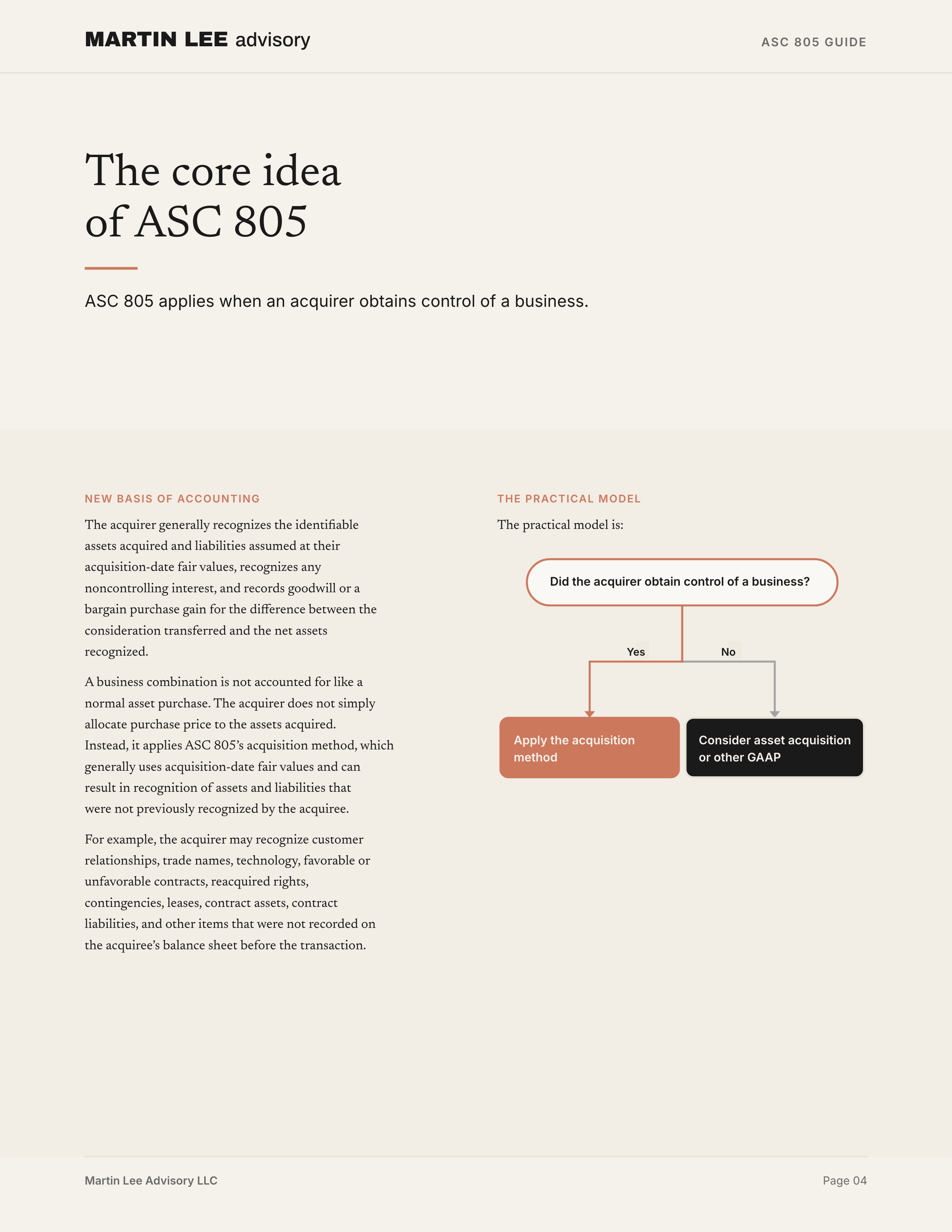

The core idea

ASC 805 applies when an acquirer obtains control of a business.

The acquirer generally recognizes the identifiable assets acquired and liabilities assumed at their acquisition-date fair values, recognizes any noncontrolling interest, and records goodwill or a bargain purchase gain for the difference between the consideration transferred and the net assets recognized.

The practical model is:

Did the acquirer obtain control of a business?

↓

No → consider asset acquisition or other GAAP

↓

Yes

↓

Apply the acquisition methodA business combination is not accounted for like a normal asset purchase. The acquirer does not simply allocate purchase price to the assets acquired. Instead, it applies ASC 805’s acquisition method, which generally uses acquisition-date fair values and can result in recognition of assets and liabilities that were not previously recognized by the acquiree.

For example, the acquirer may recognize customer relationships, trade names, technology, favorable or unfavorable contracts, reacquired rights, contingencies, leases, contract assets, contract liabilities, and other items that were not recorded on the acquiree’s balance sheet before the transaction.

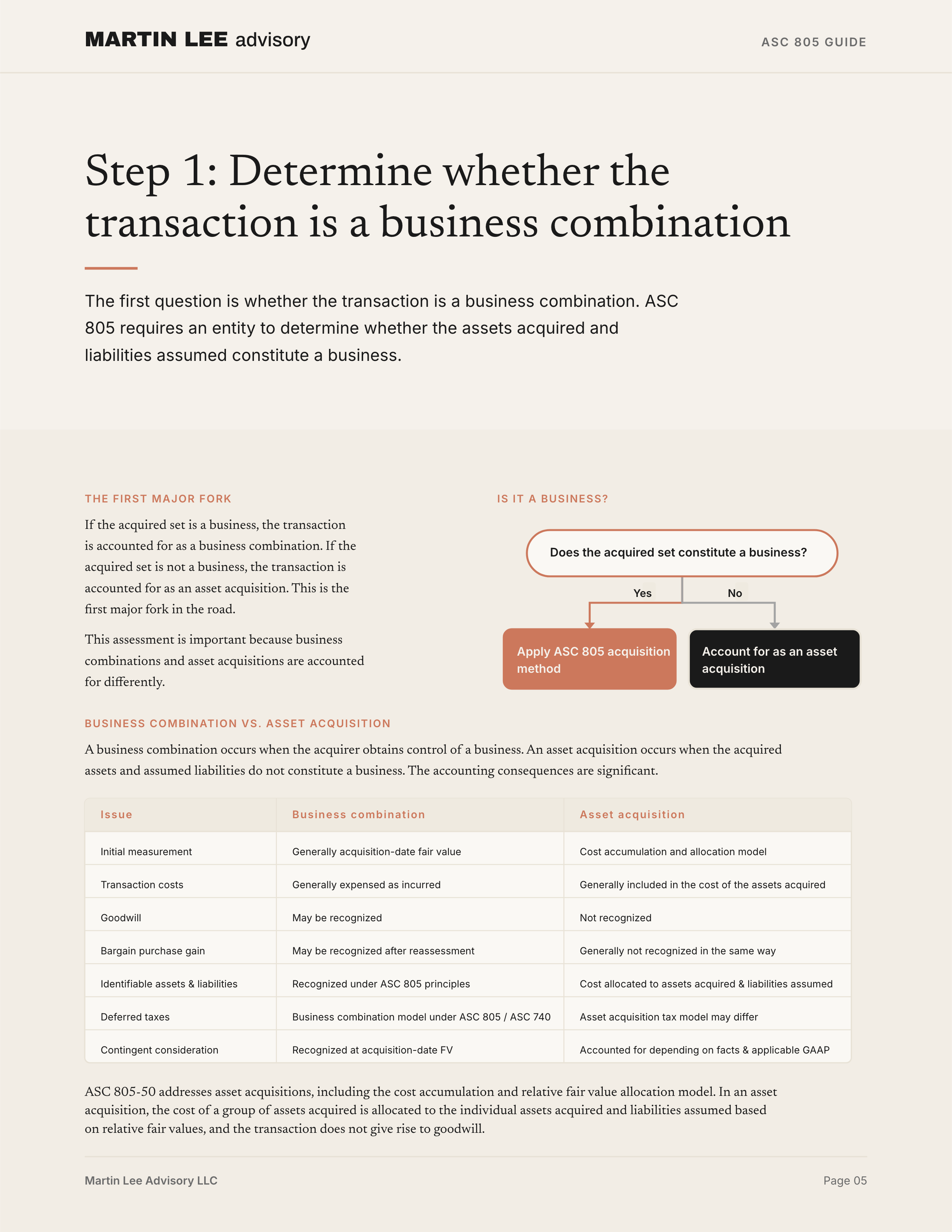

Step 1: Determine whether the transaction is a business combination

The first question is whether the transaction is a business combination.

ASC 805 requires an entity to determine whether the assets acquired and liabilities assumed constitute a business. If the acquired set is a business, the transaction is accounted for as a business combination. If the acquired set is not a business, the transaction is accounted for as an asset acquisition.

This is the first major fork in the road.

Does the acquired set constitute a business?

↓

Yes → apply ASC 805 acquisition method

↓

No → account for as an asset acquisitionThis assessment is important because business combinations and asset acquisitions are accounted for differently.

Business combination vs. asset acquisition

A business combination occurs when the acquirer obtains control of a business. An asset acquisition occurs when the acquired assets and assumed liabilities do not constitute a business.

The accounting consequences are significant.

| Issue | Business combination | Asset acquisition |

|---|---|---|

| Initial measurement | Generally acquisition-date fair value | Cost accumulation and allocation model |

| Transaction costs | Generally expensed as incurred | Generally included in the cost of the assets acquired |

| Goodwill | May be recognized | Not recognized |

| Bargain purchase gain | May be recognized after reassessment | Generally not recognized in the same way |

| Identifiable assets and liabilities | Recognized under ASC 805 recognition and measurement principles | Cost allocated to assets acquired and liabilities assumed |

| Deferred taxes | Business combination model under ASC 805 / ASC 740 | Asset acquisition tax model may differ |

| Contingent consideration | Recognized at acquisition-date fair value if part of consideration transferred | Often accounted for differently depending on facts and applicable GAAP |

ASC 805-50 addresses asset acquisitions, including the cost accumulation and relative fair value allocation model. In an asset acquisition, the cost of a group of assets acquired is allocated to the individual assets acquired and liabilities assumed based on relative fair values, and the transaction does not give rise to goodwill.

The distinction can be especially important in industries where transactions often involve asset groups that may or may not be businesses, such as real estate, life sciences, technology, energy, financial services, and asset management.

The definition of a business

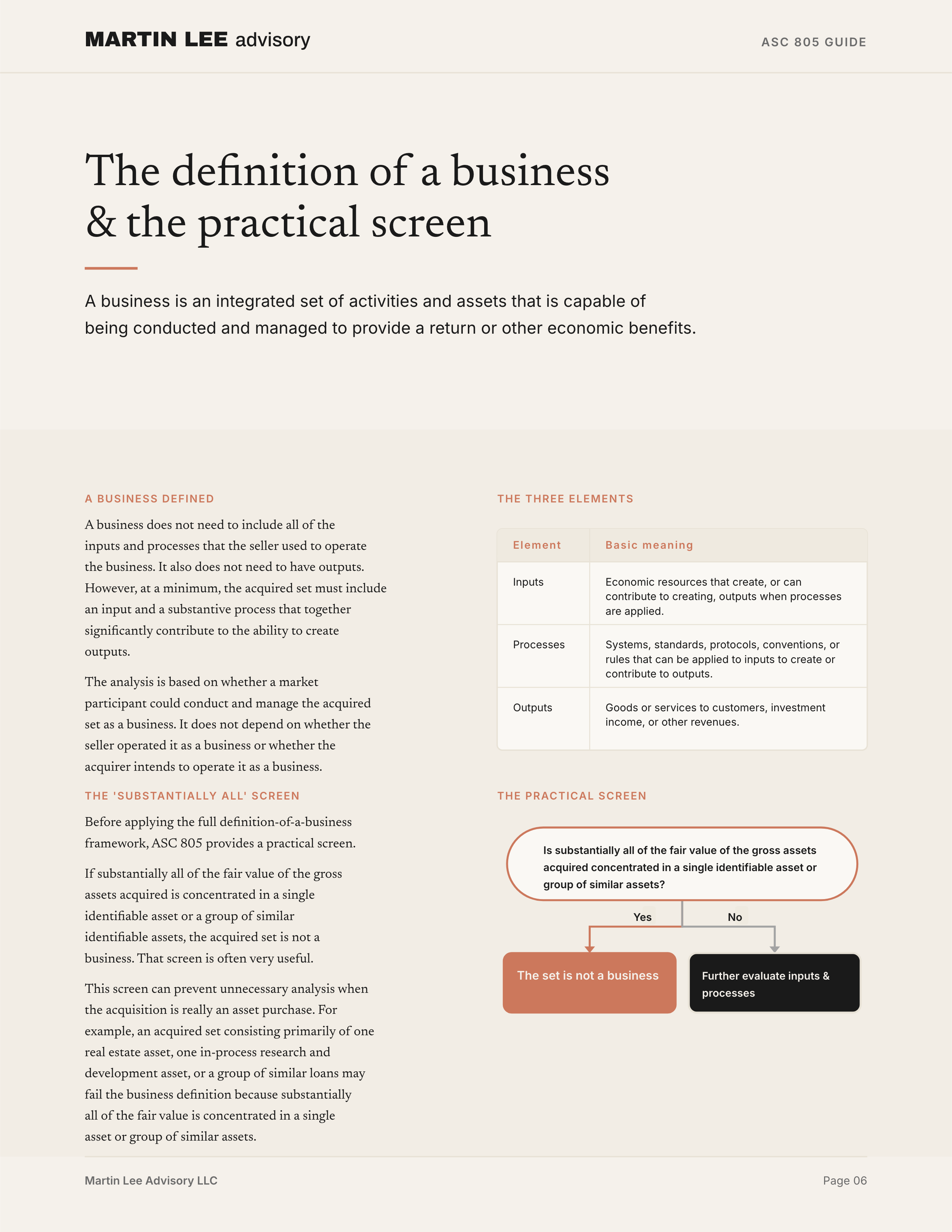

A business is an integrated set of activities and assets that is capable of being conducted and managed to provide a return or other economic benefits.

ASC 805 describes a business as consisting of:

| Element | Basic meaning |

|---|---|

| Inputs | Economic resources that create, or can contribute to creating, outputs when processes are applied. |

| Processes | Systems, standards, protocols, conventions, or rules that can be applied to inputs to create or contribute to outputs. |

| Outputs | Goods or services to customers, investment income, or other revenues. |

A business does not need to include all of the inputs and processes that the seller used to operate the business. It also does not need to have outputs. However, at a minimum, the acquired set must include an input and a substantive process that together significantly contribute to the ability to create outputs.

The analysis is based on whether a market participant could conduct and manage the acquired set as a business. It does not depend on whether the seller operated it as a business or whether the acquirer intends to operate it as a business.

The “substantially all” screen

Before applying the full definition-of-a-business framework, ASC 805 provides a practical screen.

If substantially all of the fair value of the gross assets acquired is concentrated in a single identifiable asset or a group of similar identifiable assets, the acquired set is not a business.

That screen is often very useful.

Is substantially all of the fair value of the gross assets acquired

concentrated in a single identifiable asset or group of similar assets?

↓

Yes → the set is not a business

↓

No

↓

Further evaluate whether the set includes inputs and a substantive processThis screen can prevent unnecessary analysis when the acquisition is really an asset purchase. For example, an acquired set consisting primarily of one real estate asset, one in-process research and development asset, or a group of similar loans may fail the business definition because substantially all of the fair value is concentrated in a single asset or group of similar assets.

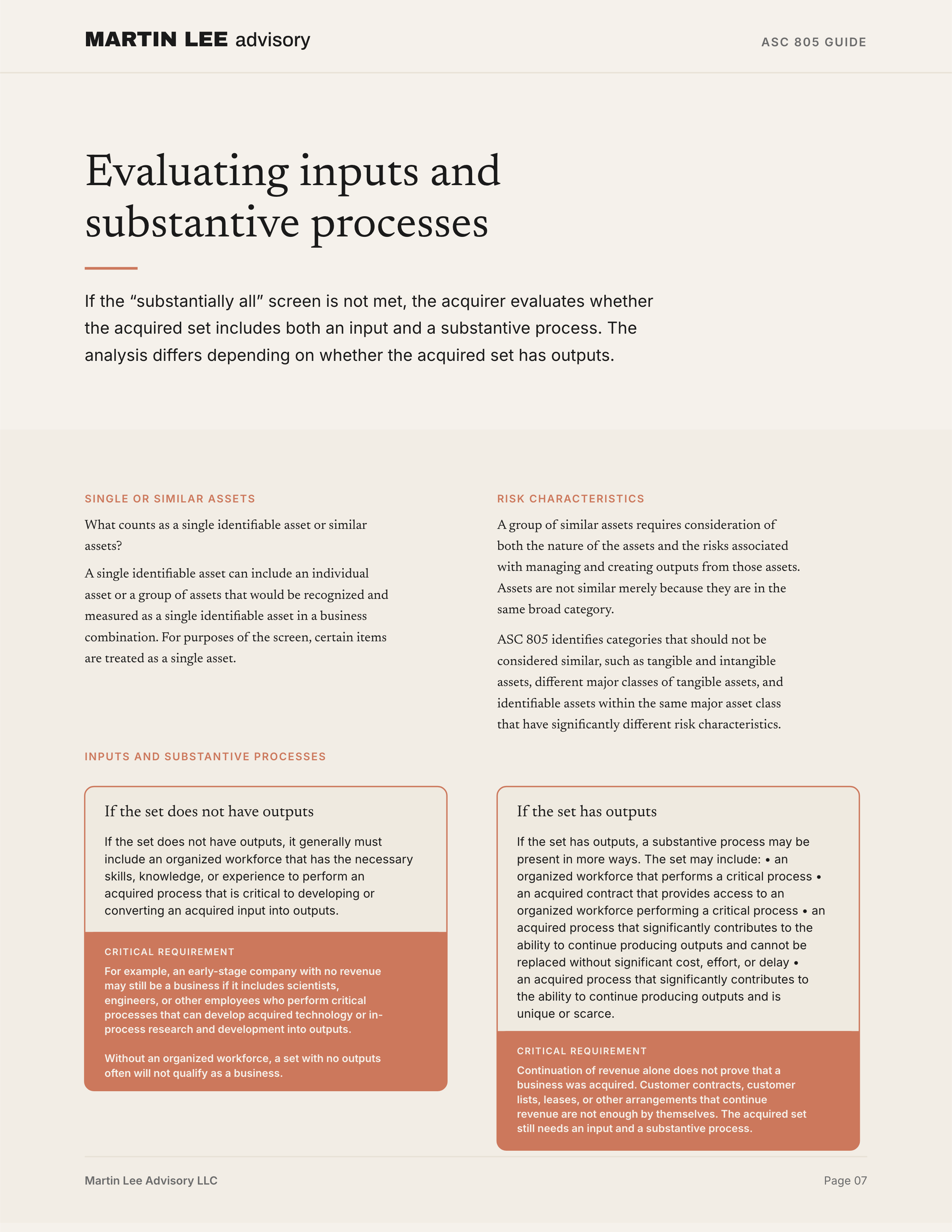

What counts as a single identifiable asset or similar assets?

A single identifiable asset can include an individual asset or a group of assets that would be recognized and measured as a single identifiable asset in a business combination.

For purposes of the screen, certain items are treated as a single asset. For example:

- land and a building may be considered a single asset if the building is attached and cannot be removed without significant cost or significant reduction in utility or fair value;

- in-place lease intangibles and related leased assets may be considered together; and

- a single in-process research and development project may be a single identifiable asset.

A group of similar assets requires consideration of both the nature of the assets and the risks associated with managing and creating outputs from those assets. Assets are not similar merely because they are in the same broad category. ASC 805 identifies categories that should not be considered similar, such as tangible and intangible assets, different major classes of tangible assets, and identifiable assets within the same major asset class that have significantly different risk characteristics.

Inputs and substantive processes

If the “substantially all” screen is not met, the acquirer evaluates whether the acquired set includes both an input and a substantive process.

The analysis differs depending on whether the acquired set has outputs.

If the set does not have outputs

If the set does not have outputs, it generally must include an organized workforce that has the necessary skills, knowledge, or experience to perform an acquired process that is critical to developing or converting an acquired input into outputs.

For example, an early-stage company with no revenue may still be a business if it includes scientists, engineers, or other employees who perform critical processes that can develop acquired technology or in-process research and development into outputs.

Without an organized workforce, a set with no outputs often will not qualify as a business.

If the set has outputs

If the set has outputs, a substantive process may be present in more ways. The set may include:

- an organized workforce that performs a critical process;

- an acquired contract that provides access to an organized workforce performing a critical process;

- an acquired process that significantly contributes to the ability to continue producing outputs and cannot be replaced without significant cost, effort, or delay; or

- an acquired process that significantly contributes to the ability to continue producing outputs and is unique or scarce.

Continuation of revenue alone does not prove that a business was acquired. Customer contracts, customer lists, leases, or other arrangements that continue revenue are not enough by themselves. The acquired set still needs an input and a substantive process.

Step 2: Identify the acquirer

For each business combination, one of the combining entities must be identified as the acquirer.

The acquirer is the entity that obtains control of the acquiree. ASC 805 generally points to the consolidation guidance in ASC 810 to determine which entity has obtained control. If that analysis does not clearly identify the acquirer, ASC 805 provides additional factors to consider.

In many transactions, identifying the acquirer is straightforward. If one entity pays cash to acquire another entity, the entity transferring cash is usually the acquirer. If one entity incurs liabilities or transfers other assets to obtain control, that entity is usually the acquirer.

In equity transactions, the analysis can be more complicated. The legal acquirer is not always the accounting acquirer.

Factors that may help identify the acquirer include:

- relative voting rights in the combined entity;

- the existence of a large minority voting interest;

- composition of the governing body;

- composition of senior management;

- terms of the exchange;

- relative size of the combining entities; and

- which entity initiated the combination.

A newly formed entity is not automatically the acquirer. If a new entity is formed to issue equity interests to effect a business combination, one of the preexisting combining entities is usually identified as the acquirer. However, a new entity that transfers cash or other assets or incurs liabilities may be the acquirer.

Step 3: Determine the acquisition date

The acquisition date is the date on which the acquirer obtains control of the acquiree.

The acquisition date is usually the closing date, because that is often when the acquirer legally transfers consideration, acquires the assets, and assumes the liabilities of the acquiree. But the acquisition date can be earlier or later than the legal closing date if control transfers on a different date.

The acquisition date matters because it is the measurement date for applying the acquisition method. The acquirer measures consideration transferred, identifiable assets acquired, liabilities assumed, noncontrolling interest, and goodwill or a bargain purchase gain as of that date.

A practical way to think about it:

When did the acquirer obtain control?

↓

That date is the acquisition date

↓

Measure the business combination as of that dateStep 4: Recognize identifiable assets acquired, liabilities assumed, and any noncontrolling interest

At the acquisition date, the acquirer recognizes, separately from goodwill:

- identifiable assets acquired;

- liabilities assumed; and

- any noncontrolling interest in the acquiree.

To be recognized as part of the business combination, identifiable assets acquired and liabilities assumed must meet the definitions of assets and liabilities at the acquisition date and must be part of what the acquirer and acquiree exchanged in the business combination.

This can result in recognizing assets and liabilities that the acquiree did not previously recognize. For example, the acquirer may recognize internally developed brands, customer relationships, technology, or other intangible assets that were not recorded by the acquiree before the acquisition.

The acquirer also classifies or designates identifiable assets acquired and liabilities assumed as needed to apply other GAAP after the acquisition. Those classifications generally are made based on contractual terms, economic conditions, the acquirer’s operating or accounting policies, and other pertinent conditions at the acquisition date.

Identifiable intangible assets

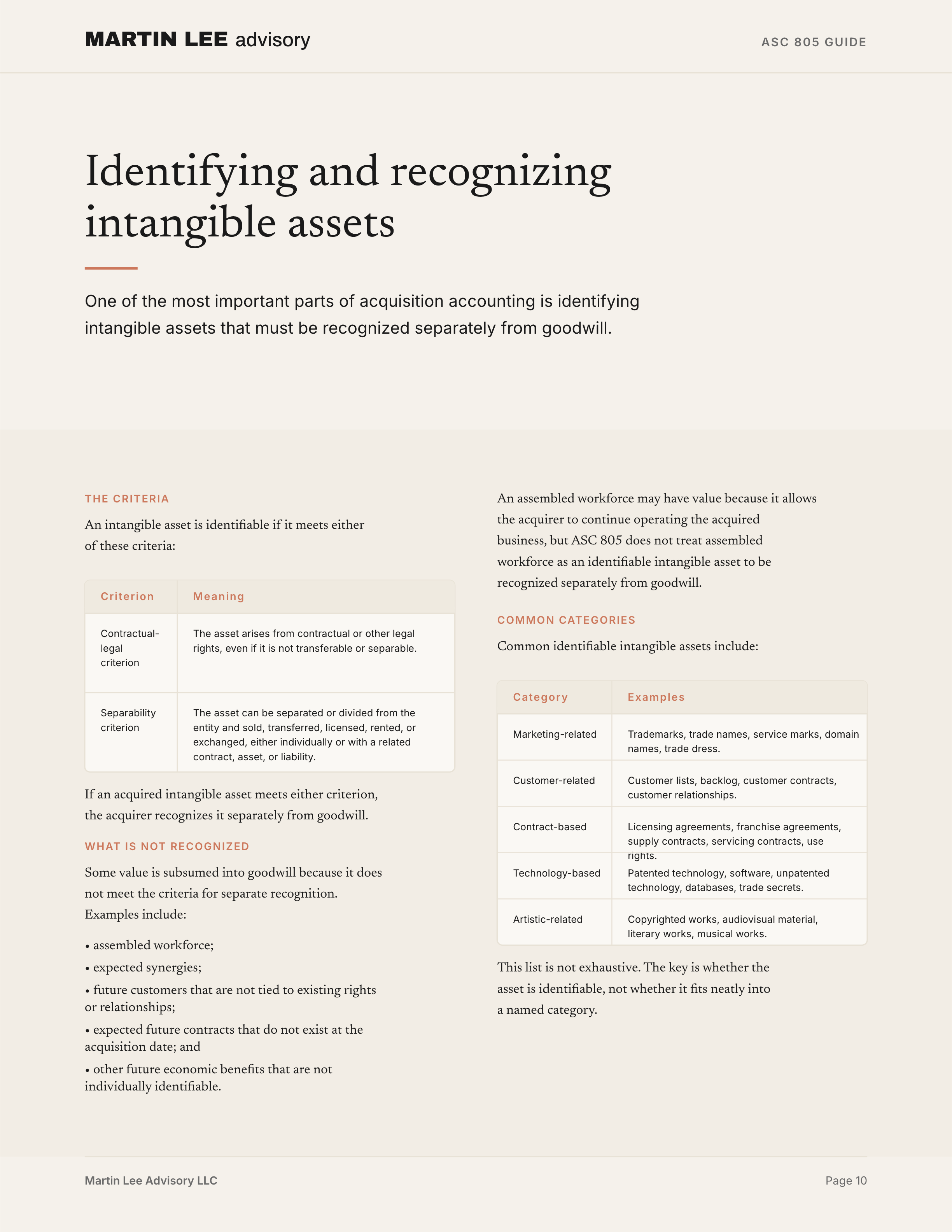

One of the most important parts of acquisition accounting is identifying intangible assets that must be recognized separately from goodwill.

An intangible asset is identifiable if it meets either of these criteria:

| Criterion | Meaning |

|---|---|

| Contractual-legal criterion | The asset arises from contractual or other legal rights, even if it is not transferable or separable. |

| Separability criterion | The asset can be separated or divided from the entity and sold, transferred, licensed, rented, or exchanged, either individually or with a related contract, asset, or liability. |

If an acquired intangible asset meets either criterion, the acquirer recognizes it separately from goodwill.

Common identifiable intangible assets include:

| Category | Examples |

|---|---|

| Marketing-related | Trademarks, trade names, service marks, domain names, trade dress. |

| Customer-related | Customer lists, backlog, customer contracts, customer relationships. |

| Contract-based | Licensing agreements, franchise agreements, supply contracts, servicing contracts, use rights. |

| Technology-based | Patented technology, software, unpatented technology, databases, trade secrets. |

| Artistic-related | Copyrighted works, audiovisual material, literary works, musical works. |

This list is not exhaustive. The key is whether the asset is identifiable, not whether it fits neatly into a named category.

What is not recognized separately from goodwill?

Some value is subsumed into goodwill because it does not meet the criteria for separate recognition.

Examples include:

- assembled workforce;

- expected synergies;

- future customers that are not tied to existing rights or relationships;

- expected future contracts that do not exist at the acquisition date; and

- other future economic benefits that are not individually identifiable.

An assembled workforce may have value because it allows the acquirer to continue operating the acquired business, but ASC 805 does not treat assembled workforce as an identifiable intangible asset to be recognized separately from goodwill.

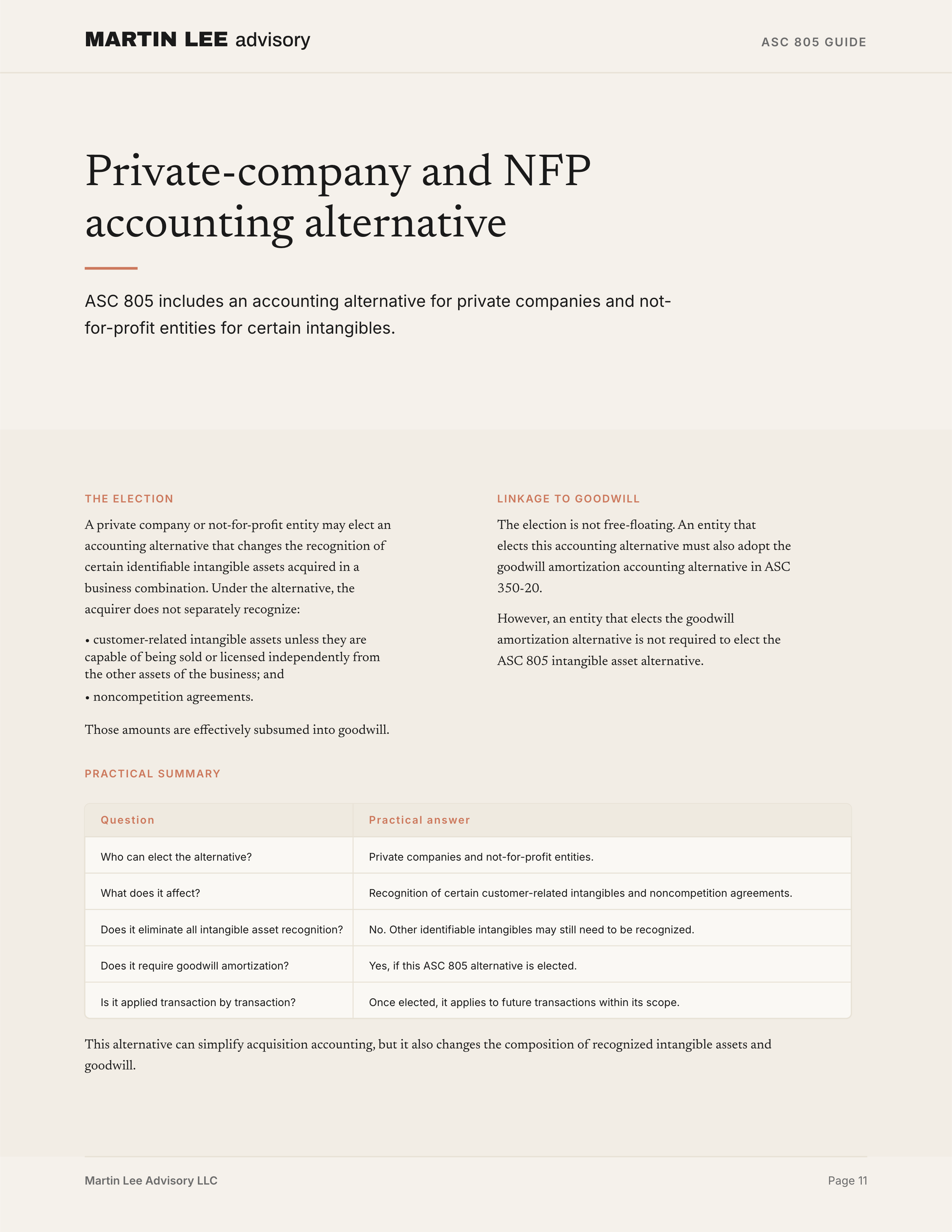

Private-company and NFP accounting alternative for certain intangibles

ASC 805 includes an accounting alternative for private companies and not-for-profit entities.

A private company or not-for-profit entity may elect an accounting alternative that changes the recognition of certain identifiable intangible assets acquired in a business combination. Under the alternative, the acquirer does not separately recognize:

- customer-related intangible assets unless they are capable of being sold or licensed independently from the other assets of the business; and

- noncompetition agreements.

Those amounts are effectively subsumed into goodwill.

The election is not free-floating. An entity that elects this accounting alternative must also adopt the goodwill amortization accounting alternative in ASC 350-20. However, an entity that elects the goodwill amortization alternative is not required to elect the ASC 805 intangible asset alternative.

A practical summary:

| Question | Practical answer |

|---|---|

| Who can elect the alternative? | Private companies and not-for-profit entities. |

| What does it affect? | Recognition of certain customer-related intangibles and noncompetition agreements. |

| Does it eliminate all intangible asset recognition? | No. Other identifiable intangibles may still need to be recognized. |

| Does it require goodwill amortization? | Yes, if this ASC 805 alternative is elected. |

| Is it applied transaction by transaction? | Once elected, it applies to future transactions within its scope. |

This alternative can simplify acquisition accounting, but it also changes the composition of recognized intangible assets and goodwill.

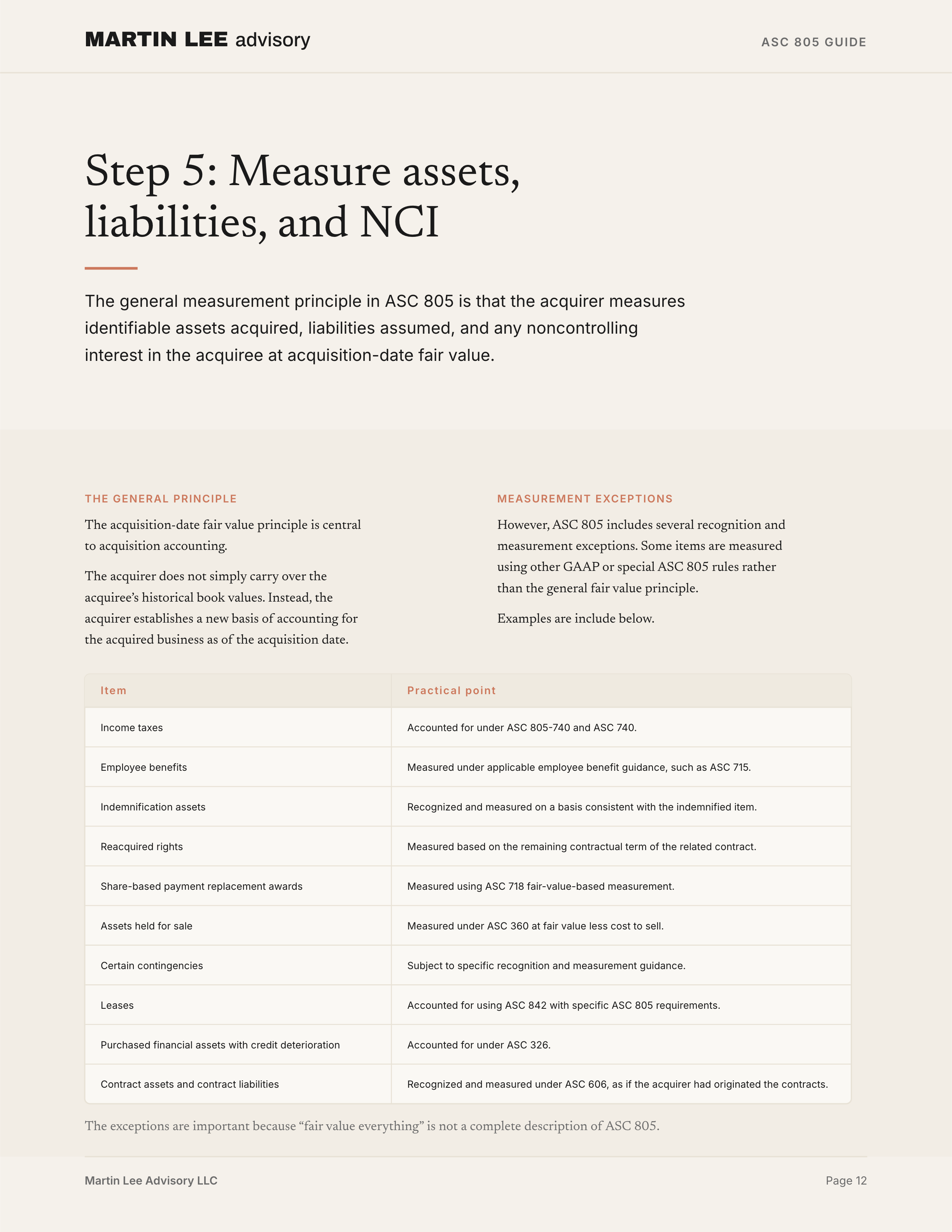

Step 5: Measure assets, liabilities, and noncontrolling interest

The general measurement principle in ASC 805 is that the acquirer measures identifiable assets acquired, liabilities assumed, and any noncontrolling interest in the acquiree at acquisition-date fair value.

That principle is central to acquisition accounting. The acquirer does not simply carry over the acquiree’s historical book values. Instead, the acquirer establishes a new basis of accounting for the acquired business as of the acquisition date.

However, ASC 805 includes several recognition and measurement exceptions. Some items are measured using other GAAP or special ASC 805 rules rather than the general fair value principle.

Examples include:

| Item | Practical point |

|---|---|

| Income taxes | Accounted for under ASC 805-740 and ASC 740. |

| Employee benefits | Measured under applicable employee benefit guidance, such as ASC 715. |

| Indemnification assets | Recognized and measured on a basis consistent with the indemnified item, subject to collectibility and contractual limitations. |

| Reacquired rights | Measured based on the remaining contractual term of the related contract. |

| Share-based payment replacement awards | Measured using ASC 718 fair-value-based measurement. |

| Assets held for sale | Measured under ASC 360 at fair value less cost to sell. |

| Certain contingencies | Subject to specific recognition and measurement guidance. |

| Leases | Accounted for using ASC 842 with specific ASC 805 requirements. |

| Purchased financial assets with credit deterioration | Accounted for under ASC 326. |

| Contract assets and contract liabilities | Recognized and measured under ASC 606, as if the acquirer had originated the contracts. |

The exceptions are important because “fair value everything” is not a complete description of ASC 805.

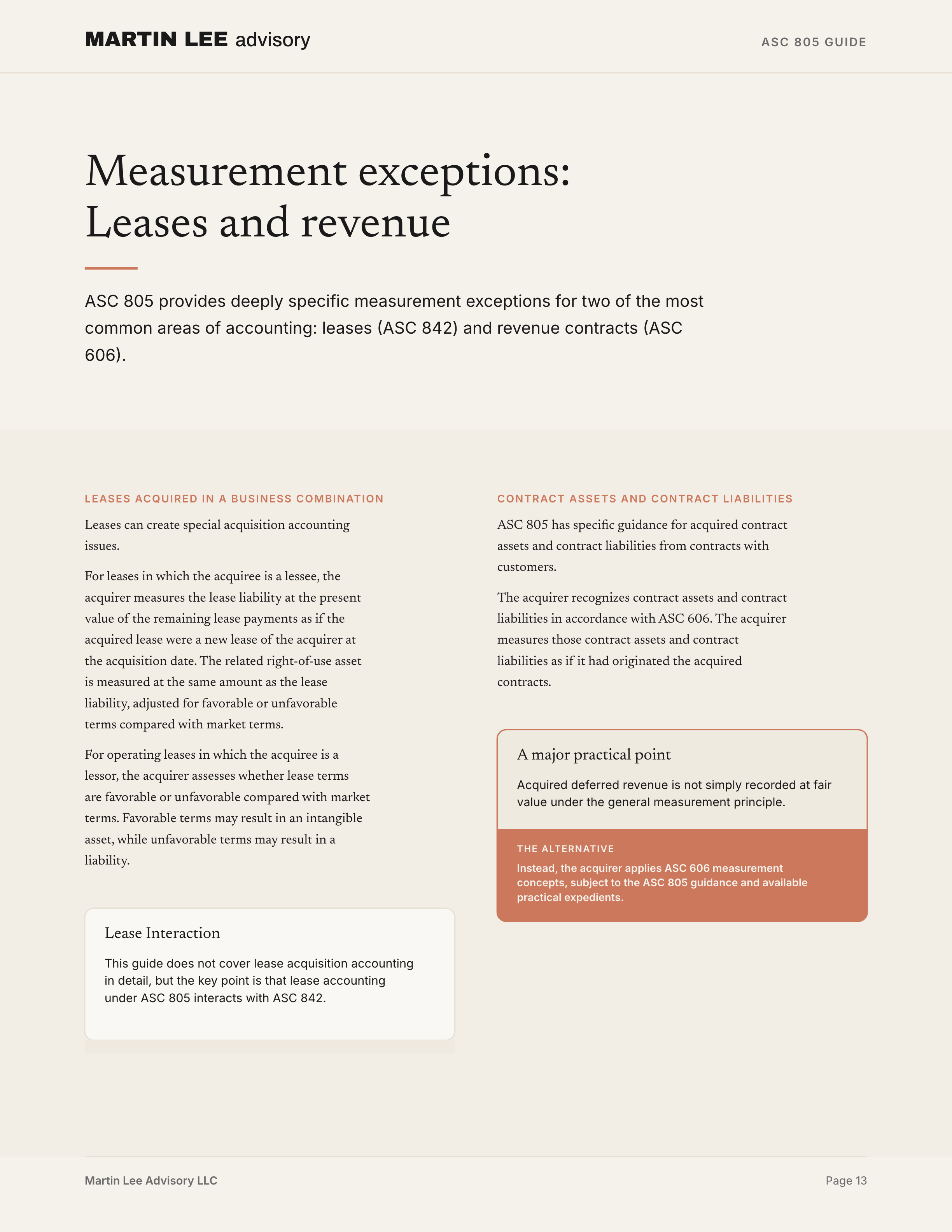

Leases acquired in a business combination

Leases can create special acquisition accounting issues.

For leases in which the acquiree is a lessee, the acquirer measures the lease liability at the present value of the remaining lease payments as if the acquired lease were a new lease of the acquirer at the acquisition date. The related right-of-use asset is measured at the same amount as the lease liability, adjusted for favorable or unfavorable terms compared with market terms.

For operating leases in which the acquiree is a lessor, the acquirer assesses whether lease terms are favorable or unfavorable compared with market terms. Favorable terms may result in an intangible asset, while unfavorable terms may result in a liability.

This guide does not cover lease acquisition accounting in detail, but the key point is that lease accounting under ASC 805 interacts with ASC 842.

Contract assets and contract liabilities

ASC 805 has specific guidance for acquired contract assets and contract liabilities from contracts with customers.

The acquirer recognizes contract assets and contract liabilities in accordance with ASC 606. The acquirer measures those contract assets and contract liabilities as if it had originated the acquired contracts.

This is a major practical point. Acquired deferred revenue is not simply recorded at fair value under the general measurement principle. Instead, the acquirer applies ASC 606 measurement concepts, subject to the ASC 805 guidance and available practical expedients.

Step 6: Measure consideration transferred

Consideration transferred in a business combination is generally measured at acquisition-date fair value.

Consideration may include:

- cash;

- other assets;

- a business or subsidiary of the acquirer;

- liabilities incurred by the acquirer to former owners of the acquiree;

- common or preferred shares;

- options;

- warrants;

- member interests; and

- contingent consideration.

If the acquirer transfers assets or liabilities with carrying amounts different from their acquisition-date fair values, the acquirer generally remeasures those transferred assets or liabilities to fair value and recognizes the resulting gain or loss in earnings.

However, if the transferred assets or liabilities remain within the combined entity after the business combination, the acquirer generally measures those assets and liabilities at their carrying amounts immediately before the acquisition date and does not recognize a gain or loss on assets or liabilities it controls both before and after the combination.

Contingent consideration

Contingent consideration is a common feature of business combinations. It usually requires the acquirer to transfer additional assets or equity interests to the former owners if specified future events occur or conditions are met. It also can give the acquirer the right to the return of previously transferred consideration if specified conditions are met.

ASC 805 requires the acquirer to recognize the acquisition-date fair value of contingent consideration as part of the consideration transferred in exchange for the acquiree.

The subsequent accounting depends on classification.

| Classification | Subsequent accounting |

|---|---|

| Equity | Not remeasured; settlement is accounted for within equity. |

| Asset or liability | Remeasured to fair value each reporting date until resolved; changes generally recognized in earnings. |

This classification matters. A liability-classified earnout can create post-acquisition earnings volatility because changes in fair value are recognized through earnings unless the arrangement qualifies for hedge accounting treatment.

Not every future payment to sellers is contingent consideration. Some payments are compensation, settlement of a preexisting relationship, reimbursement of acquisition costs, or another separate transaction. The acquirer must determine what is part of the exchange for the acquiree and what should be accounted for separately.

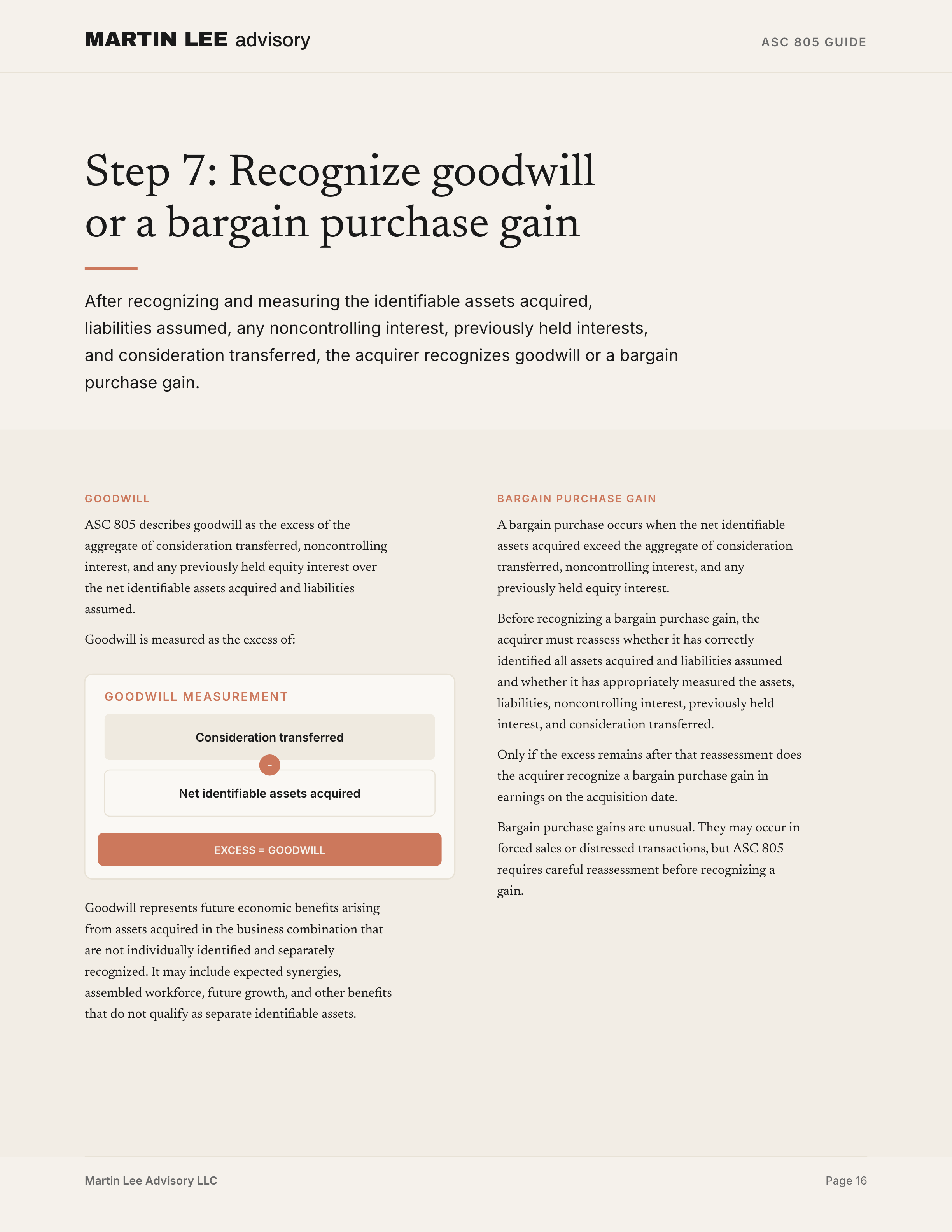

Step 7: Recognize goodwill or a bargain purchase gain

After recognizing and measuring the identifiable assets acquired, liabilities assumed, any noncontrolling interest, previously held interests, and consideration transferred, the acquirer recognizes goodwill or a bargain purchase gain.

Goodwill is measured as the excess of:

Consideration transferred

+ fair value of any noncontrolling interest

+ fair value of any previously held equity interest

over

Identifiable assets acquired

- liabilities assumedASC 805 describes goodwill as the excess of the aggregate of consideration transferred, noncontrolling interest, and any previously held equity interest over the net identifiable assets acquired and liabilities assumed.

Goodwill represents future economic benefits arising from assets acquired in the business combination that are not individually identified and separately recognized. It may include expected synergies, assembled workforce, future growth, and other benefits that do not qualify as separate identifiable assets.

Bargain purchase gain

A bargain purchase occurs when the net identifiable assets acquired exceed the aggregate of consideration transferred, noncontrolling interest, and any previously held equity interest.

Before recognizing a bargain purchase gain, the acquirer must reassess whether it has correctly identified all assets acquired and liabilities assumed and whether it has appropriately measured the assets, liabilities, noncontrolling interest, previously held interest, and consideration transferred.

Only if the excess remains after that reassessment does the acquirer recognize a bargain purchase gain in earnings on the acquisition date.

A practical summary:

Net identifiable assets exceed consideration and related amounts?

↓

Yes

↓

Reassess identification and measurement of all relevant items

↓

Excess still remains?

↓

Yes → recognize bargain purchase gain in earningsBargain purchase gains are unusual. They may occur in forced sales or distressed transactions, but ASC 805 requires careful reassessment before recognizing a gain.

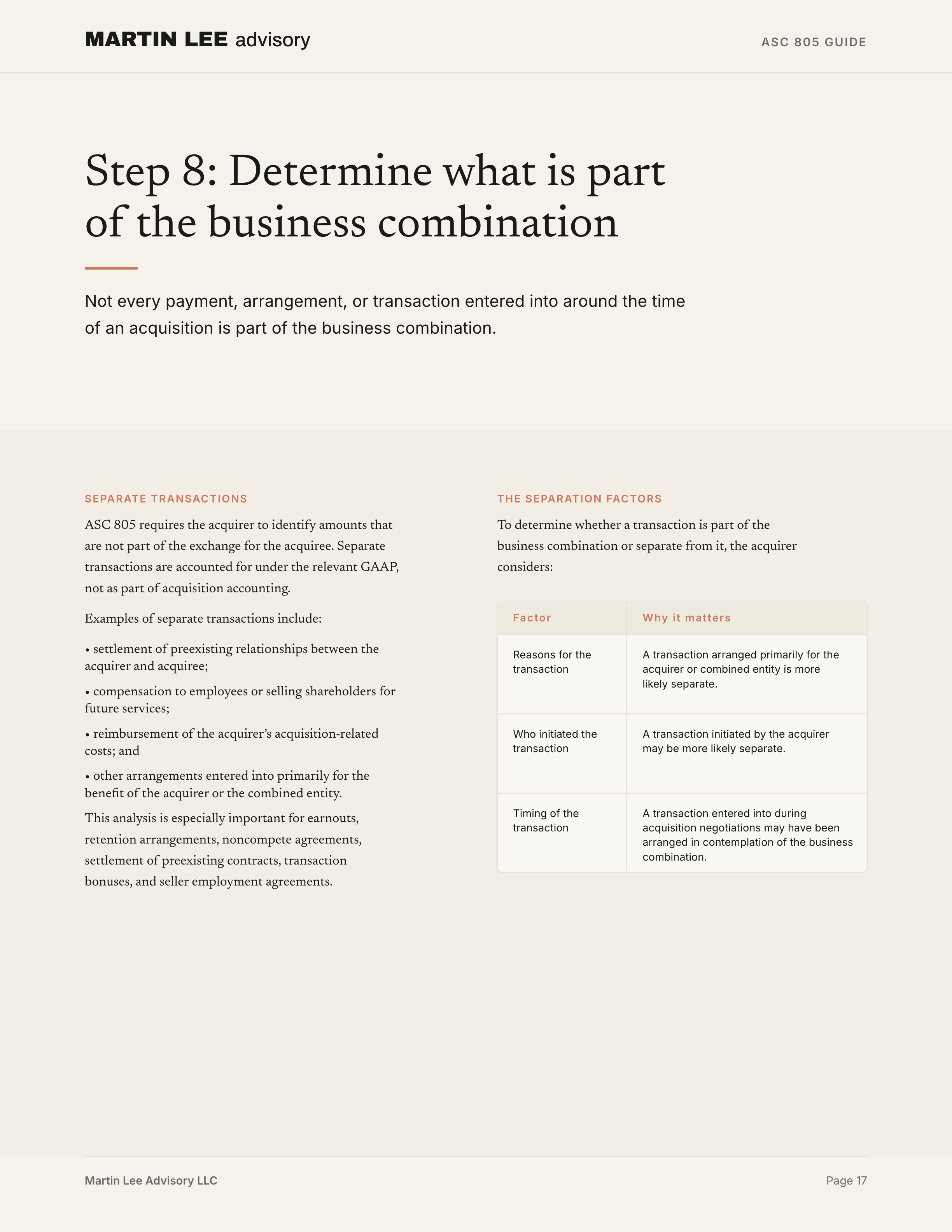

Step 8: Determine what is part of the business combination

Not every payment, arrangement, or transaction entered into around the time of an acquisition is part of the business combination.

ASC 805 requires the acquirer to identify amounts that are not part of the exchange for the acquiree. Separate transactions are accounted for under the relevant GAAP, not as part of acquisition accounting.

Examples of separate transactions include:

- settlement of preexisting relationships between the acquirer and acquiree;

- compensation to employees or selling shareholders for future services;

- reimbursement of the acquirer’s acquisition-related costs; and

- other arrangements entered into primarily for the benefit of the acquirer or the combined entity.

To determine whether a transaction is part of the business combination or separate from it, the acquirer considers:

| Factor | Why it matters |

|---|---|

| Reasons for the transaction | A transaction arranged primarily for the acquirer or combined entity is more likely separate. |

| Who initiated the transaction | A transaction initiated by the acquirer may be more likely separate. |

| Timing of the transaction | A transaction entered into during acquisition negotiations may have been arranged in contemplation of the business combination. |

This analysis is especially important for earnouts, retention arrangements, noncompete agreements, settlement of preexisting contracts, transaction bonuses, and seller employment agreements.

Contingent payments to employees or selling shareholders

Contingent payments to sellers are not automatically purchase consideration.

If selling shareholders become employees of the acquirer or combined company, ASC 805 requires careful evaluation of whether contingent payments are consideration for the acquiree or compensation for postcombination services.

A key indicator is continuing employment. If contingent payments are automatically forfeited when employment terminates, the arrangement is compensation for postcombination services. If payments are not affected by employment termination, that may indicate the payments are additional consideration.

Other indicators include:

- duration of required employment;

- level of other compensation;

- whether employee-sellers receive incremental payments compared with nonemployee sellers;

- relative ownership of selling shareholders who remain as employees;

- linkage to the valuation of the acquiree;

- formula for determining the payment; and

- other related agreements, such as leases, consulting agreements, or noncompetes.

This is one of the most practical areas of ASC 805 because legal deal terms may describe an arrangement one way, while GAAP accounting substance may point somewhere else.

Acquisition-related costs

Acquisition-related costs are not included in consideration transferred.

ASC 805 requires the acquirer to expense acquisition-related costs in the periods in which the costs are incurred and services are received, except for costs to issue debt or equity securities, which are accounted for under other applicable GAAP.

Acquisition-related costs include:

- finder’s fees;

- advisory fees;

- legal fees;

- accounting fees;

- valuation fees;

- consulting fees;

- general administrative costs related to the acquisition; and

- costs of maintaining an internal acquisition department.

This treatment differs from asset acquisitions, where transaction costs generally are included in the cost of the assets acquired.

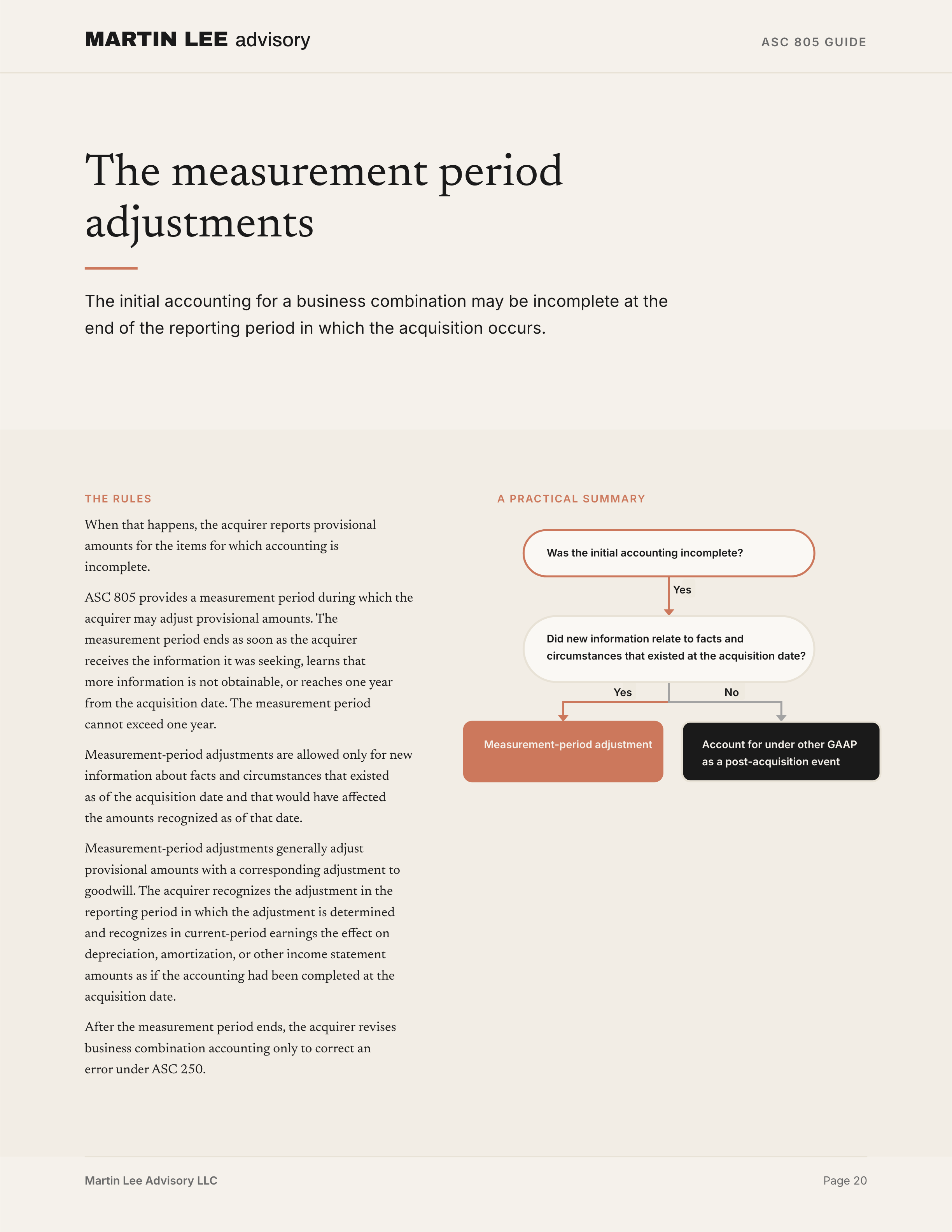

Measurement-period adjustments

The initial accounting for a business combination may be incomplete at the end of the reporting period in which the acquisition occurs. When that happens, the acquirer reports provisional amounts for the items for which accounting is incomplete.

ASC 805 provides a measurement period during which the acquirer may adjust provisional amounts. The measurement period ends as soon as the acquirer receives the information it was seeking, learns that more information is not obtainable, or reaches one year from the acquisition date. The measurement period cannot exceed one year.

Measurement-period adjustments are allowed only for new information about facts and circumstances that existed as of the acquisition date and that would have affected the amounts recognized as of that date.

A practical summary:

Was the initial accounting incomplete?

↓

Yes

↓

Did new information relate to facts and circumstances

that existed at the acquisition date?

↓

Yes → measurement-period adjustment

↓

No → account for under other GAAP as a post-acquisition eventMeasurement-period adjustments generally adjust provisional amounts with a corresponding adjustment to goodwill. The acquirer recognizes the adjustment in the reporting period in which the adjustment is determined and recognizes in current-period earnings the effect on depreciation, amortization, or other income statement amounts as if the accounting had been completed at the acquisition date.

After the measurement period ends, the acquirer revises business combination accounting only to correct an error under ASC 250.

Step acquisitions

A step acquisition occurs when the acquirer obtains control of an acquiree in which it previously held an equity interest.

In a business combination achieved in stages, the acquirer remeasures its previously held equity interest in the acquiree at acquisition-date fair value and recognizes any resulting gain or loss in earnings. Amounts previously recognized in other comprehensive income related to that interest may also need to be reclassified and included in the calculation of the gain or loss.

The acquisition-date fair value of the previously held interest is included in measuring goodwill or a bargain purchase gain.

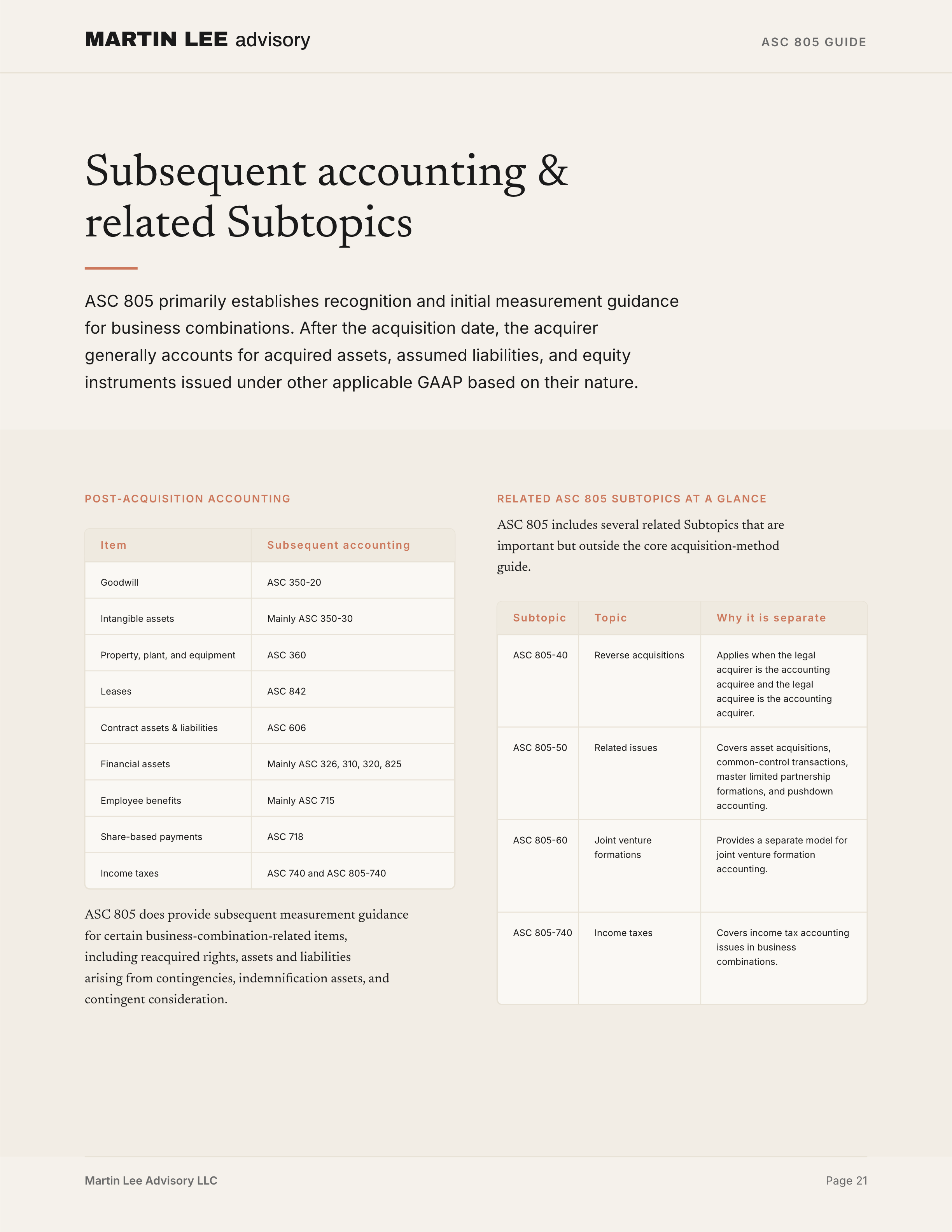

Subsequent accounting

ASC 805 primarily establishes recognition and initial measurement guidance for business combinations. After the acquisition date, the acquirer generally accounts for acquired assets, assumed liabilities, and equity instruments issued under other applicable GAAP based on their nature.

For example:

| Item | Subsequent accounting |

|---|---|

| Goodwill | ASC 350-20 |

| Identifiable intangible assets | ASC 350-30 or other applicable guidance |

| Property, plant, and equipment | ASC 360 |

| Leases | ASC 842 |

| Contract assets and contract liabilities | ASC 606 |

| Financial assets | ASC 326, ASC 310, ASC 320, ASC 825, or other applicable guidance |

| Employee benefits | ASC 715 or other employee benefit guidance |

| Share-based payment replacement awards | ASC 718 |

| Income taxes | ASC 740 and ASC 805-740 |

ASC 805 does provide subsequent measurement guidance for certain business-combination-related items, including reacquired rights, assets and liabilities arising from contingencies, indemnification assets, and contingent consideration.

Related ASC 805 Subtopics at a glance

ASC 805 includes several related Subtopics that are important but outside the core acquisition-method guide.

| Subtopic | Topic | Why it is separate |

|---|---|---|

| ASC 805-40 | Reverse acquisitions | Applies when the legal acquirer is the accounting acquiree and the legal acquiree is the accounting acquirer. |

| ASC 805-50 | Related issues | Covers asset acquisitions, common-control transactions, master limited partnership formations, and pushdown accounting. |

| ASC 805-60 | Joint venture formations | Provides a separate model for joint venture formation accounting. |

| ASC 805-740 | Income taxes | Covers income tax accounting issues in business combinations. |

Reverse acquisitions can occur when a legal acquirer issues equity interests but is identified as the acquiree for accounting purposes. ASC 805-40 provides incremental guidance for applying the acquisition method in those transactions.

ASC 805-50 includes guidance for transactions that may be associated with business combinations but are not necessarily accounted for as business combinations, including asset acquisitions, common-control transactions, and pushdown accounting.

ASC 805-60 provides guidance for joint venture formations. Unlike the acquisition method, joint venture formation accounting does not identify an acquirer. Instead, the joint venture establishes a new basis of accounting upon formation using aspects of the acquisition method adapted for joint ventures.

Disclosure

ASC 805 disclosure is designed to help users understand the nature and financial effects of a business combination.

For each material business combination, the acquirer generally discloses information such as:

- the name and description of the acquiree;

- the acquisition date;

- the percentage of voting equity interests acquired;

- the primary reasons for the business combination;

- how the acquirer obtained control;

- the acquisition-date fair value of consideration transferred, by major class;

- the recognized amounts of major classes of assets acquired and liabilities assumed;

- the fair value of any noncontrolling interest and how it was measured;

- the amount of goodwill recognized and a qualitative description of the factors that make up goodwill;

- the amount of goodwill expected to be deductible for tax purposes;

- contingent consideration arrangements;

- acquisition-related costs expensed;

- separately recognized transactions;

- bargain purchase gains, if any;

- step acquisition gains or losses, if any;

- measurement-period adjustments; and

- pro forma information for public entities, when required.

The disclosure requirements can be extensive, but the objective is practical: users should be able to understand what was acquired, why it was acquired, how it was measured, and how the transaction affected the financial statements.

Practical summary

ASC 805 can be summarized through a series of practical questions.

Is the transaction a business combination?

Did the acquirer obtain control?

↓

No → not a business combination

↓

Yes

↓

Does the acquired set constitute a business?

↓

No → account for as an asset acquisition

↓

Yes → apply the acquisition methodDoes the acquired set constitute a business?

Is substantially all fair value concentrated

in a single identifiable asset or group of similar assets?

↓

Yes → not a business

↓

No

↓

Does the set include an input and a substantive process

that together significantly contribute to the ability to create outputs?

↓

No → not a business

↓

Yes → businessWhat are the acquisition method steps?

Identify the acquirer

↓

Determine the acquisition date

↓

Recognize identifiable assets acquired,

liabilities assumed, and any NCI

↓

Measure those items under ASC 805

↓

Measure consideration transferred

↓

Recognize goodwill or bargain purchase gainIs an intangible asset recognized separately from goodwill?

Does the intangible asset arise from contractual or legal rights?

↓

Yes → recognize separately from goodwill

↓

No

↓

Is it separable, either alone or with a related asset,

liability, or contract?

↓

Yes → recognize separately from goodwill

↓

No → subsume into goodwillIs a payment part of the business combination?

Was the payment part of the exchange for the acquiree?

↓

Yes → include in acquisition accounting

↓

No

↓

Account for separately under other GAAPWhere this guide stops

This guide covers the core ASC 805 acquisition-method model: determining whether a transaction is a business combination, distinguishing business combinations from asset acquisitions, applying the definition of a business, identifying the acquirer and acquisition date, recognizing and measuring identifiable assets acquired and liabilities assumed, recognizing identifiable intangible assets, considering the private-company and NFP intangible asset alternative, measuring consideration transferred, accounting for contingent consideration at a high level, recognizing goodwill or a bargain purchase gain, identifying separate transactions, accounting for acquisition-related costs, applying measurement-period guidance, and understanding disclosure at a high level.

It does not cover every specialized issue in ASC 805.

Topics that deserve separate focused guides include:

- asset acquisitions under ASC 805-50;

- common-control transactions under ASC 805-50;

- pushdown accounting under ASC 805-50;

- reverse acquisitions under ASC 805-40;

- joint venture formations under ASC 805-60;

- income taxes in business combinations under ASC 805-740;

- acquired contingencies;

- acquired revenue contracts and contract liabilities;

- acquired leases;

- replacement share-based payment awards;

- reacquired rights;

- indemnification assets;

- contingent consideration valuation and classification;

- bargain purchase transactions; and

- business combination disclosures for public entities.

ASC 805 is often described as purchase accounting, but that phrase understates the model. The standard is not merely about allocating a purchase price. It is about identifying whether a business was acquired, determining who acquired it and when, recognizing the assets and liabilities that were part of the exchange, and measuring the resulting goodwill or bargain purchase gain under a structured acquisition-date model.