ASC 606 Revenue from Contracts with Customers — A Concise Guide to the Core Model

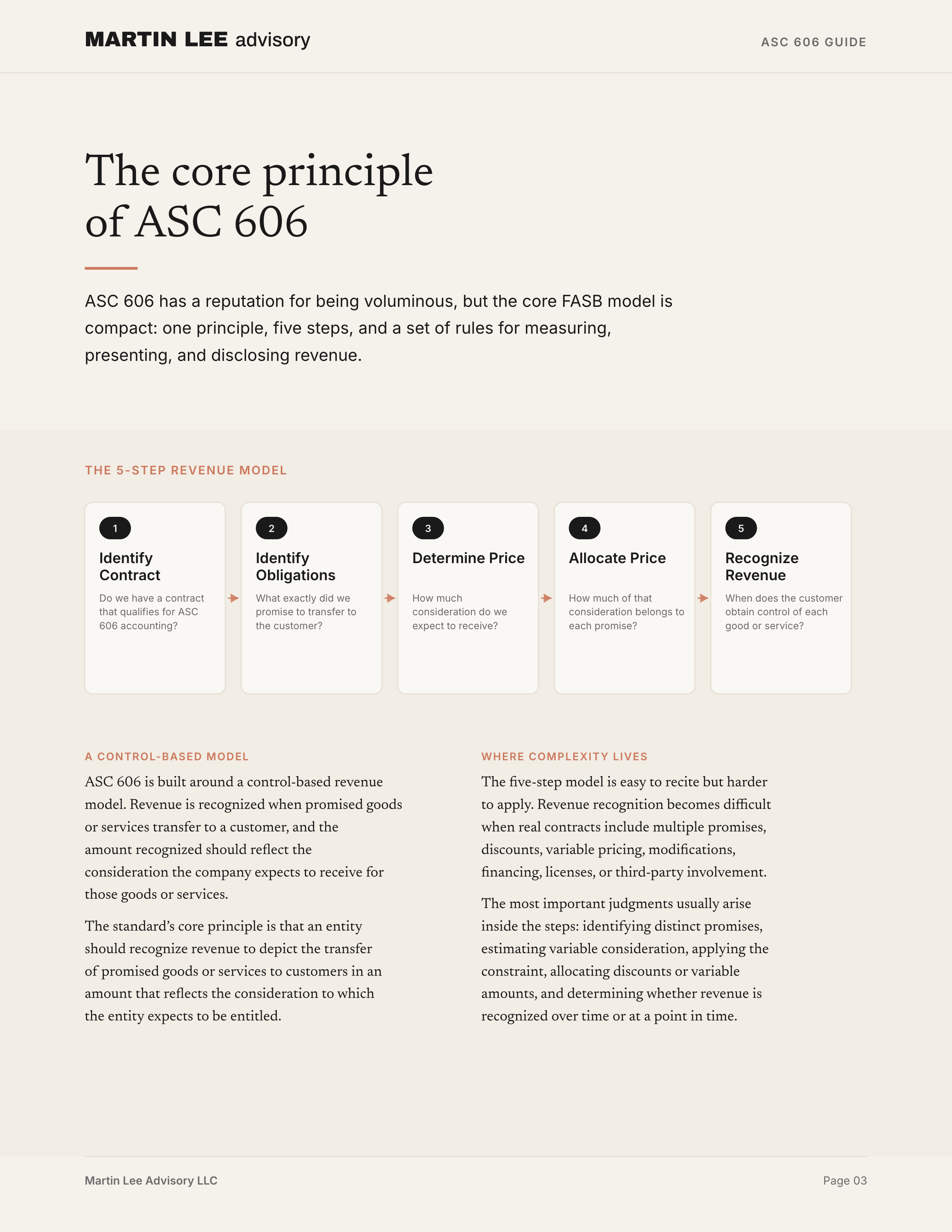

ASC 606 has a reputation for being enormous. In practice, much of that reputation comes from the interpretive literature around it. The core FASB model is much more compact: one principle, five steps, and a set of rules for measuring, presenting, and disclosing revenue from contracts with customers.

That does not mean ASC 606 is easy. Revenue recognition becomes difficult when real contracts include multiple promises, discounts, variable pricing, modifications, financing, licenses, or third-party involvement. But those complexities build on a relatively simple foundation.

This guide focuses on that foundation. It translates the core ASC 606 guidance into plain English, following the structure of the standard: scope, recognition, measurement, presentation, and disclosure. It does not try to cover every implementation topic. Those topics are important, but they are better addressed in separate, focused guides.

The core principle

ASC 606 is built around a control-based revenue model. Revenue is recognized when promised goods or services transfer to a customer, and the amount recognized should reflect the consideration the company expects to receive for those goods or services.

The standard’s core principle is that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled.

That principle is applied through five steps:

- Identify the contract with a customer.

- Identify the performance obligations in the contract.

- Determine the transaction price.

- Allocate the transaction price to the performance obligations.

- Recognize revenue when, or as, each performance obligation is satisfied.

Each step answers a practical question.

| Step | Practical question |

|---|---|

| Step 1 | Do we have a contract that qualifies for ASC 606 accounting? |

| Step 2 | What exactly did we promise to transfer to the customer? |

| Step 3 | How much consideration do we expect to receive? |

| Step 4 | How much of that consideration belongs to each promise? |

| Step 5 | When does the customer obtain control of each promised good or service? |

The five-step model is easy to recite but harder to apply. The most important judgments usually arise inside the steps: identifying distinct promises, estimating variable consideration, applying the constraint, allocating discounts or variable amounts, and determining whether revenue is recognized over time or at a point in time.

What ASC 606 covers

ASC 606 applies to contracts with customers. A customer is a party that obtains goods or services that are outputs of the company’s ordinary activities in exchange for consideration. That distinction matters because ASC 606 is not a general model for every contract or every cash inflow. It applies when the counterparty is a customer and the arrangement relates to the company’s ordinary goods or services.

The guidance applies to all entities, but it does not apply to all contracts. Several types of arrangements are excluded because they are addressed by other GAAP Topics. Common scope exceptions include lease contracts, insurance contracts, financial instruments and certain other contractual rights or obligations, guarantees other than product or service warranties, and certain nonmonetary exchanges between entities in the same line of business.

For not-for-profit entities, an additional threshold question may arise: whether the transaction is a contribution rather than a customer contract. If the transaction is a contribution, the not-for-profit contribution guidance applies instead of ASC 606.

Some arrangements are partly within ASC 606 and partly within another Topic. When a contract includes both revenue elements and elements covered by other guidance, the company first looks to the other Topic. If that Topic specifies how to separate or initially measure part of the contract, the company applies that guidance first and then applies ASC 606 to the remaining consideration. If the other Topic does not specify how to separate or initially measure the non-606 element, ASC 606 is used to separate or initially measure the relevant parts of the contract.

This guide does not address contract costs. Costs to obtain or fulfill a contract are covered separately in ASC 340-40.

Step 1: Identify the contract with a customer

The first step asks whether the arrangement qualifies as a contract for ASC 606 purposes. This is more than a formality. If the Step 1 criteria are not met, the company generally cannot apply the revenue model yet, even if it has received cash.

A contract can be written, oral, or implied by customary business practices. The form is less important than whether the arrangement creates enforceable rights and obligations. Because enforceability is a matter of law, the analysis may depend on the legal environment, the company’s contracting practices, the customer class, and the nature of the promised goods or services.

A company accounts for a contract under ASC 606 only when all of the following criteria are met:

- The parties have approved the contract and are committed to perform.

- The company can identify each party’s rights regarding the goods or services to be transferred.

- The company can identify the payment terms.

- The contract has commercial substance.

- It is probable that the company will collect substantially all of the consideration to which it expects to be entitled for the goods or services that will be transferred.

Commercial substance means the contract is expected to change the risk, timing, or amount of the company’s future cash flows. The collectibility assessment focuses on the customer’s ability and intention to pay when amounts are due. Importantly, the assessment is based on the consideration the company expects to be entitled to receive, not necessarily the stated contract price. If the company expects to provide a price concession, that expectation affects the amount used in the collectibility analysis.

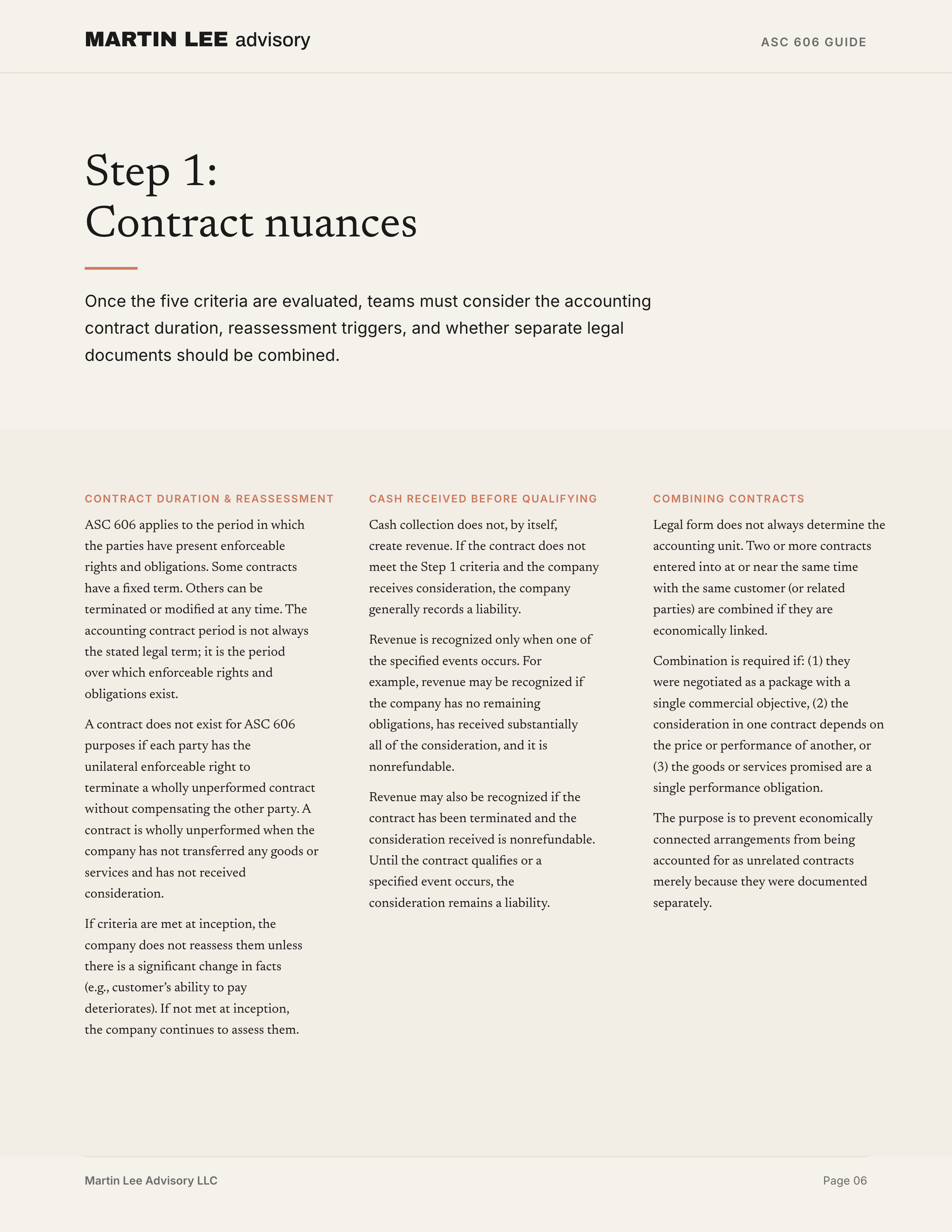

Contract duration

ASC 606 applies to the period in which the parties have present enforceable rights and obligations. Some contracts have a fixed term. Others can be terminated or modified at any time. Some automatically renew. The accounting contract period is not always the stated legal term; it is the period over which enforceable rights and obligations exist.

A contract does not exist for ASC 606 purposes if each party has the unilateral enforceable right to terminate a wholly unperformed contract without compensating the other party. A contract is wholly unperformed when the company has not transferred any promised goods or services and has not received, and is not entitled to receive, any consideration.

Reassessment

If the Step 1 criteria are met at contract inception, the company does not reassess them unless there is an indication of a significant change in facts and circumstances. For example, if the customer’s ability to pay deteriorates significantly, the company may need to reassess collectibility for the remaining goods or services.

If the criteria are not met at inception, the company continues to assess the arrangement to determine whether the criteria are met later.

Cash received before the contract qualifies

Cash collection does not, by itself, create revenue. If the contract does not meet the Step 1 criteria and the company receives consideration from the customer, the company generally records a liability.

Revenue is recognized only when one of the specified events occurs. For example, revenue may be recognized if the company has no remaining obligations, has received all or substantially all of the promised consideration, and the consideration is nonrefundable. Revenue may also be recognized if the contract has been terminated and the consideration received is nonrefundable. Until the contract qualifies for ASC 606 accounting or one of the specified events occurs, the consideration received remains a liability.

Combining contracts

Legal form does not always determine the accounting unit. Two or more contracts entered into at or near the same time with the same customer, or related parties of the customer, are combined if they are economically linked.

Combination is required if any of the following conditions are met:

- the contracts were negotiated as a package with a single commercial objective;

- the amount of consideration in one contract depends on the price or performance of another contract; or

- the goods or services promised in the contracts are a single performance obligation.

The purpose of this guidance is to prevent economically connected arrangements from being accounted for as unrelated contracts merely because they were documented separately.

Contract modifications

A contract modification is a change in scope, price, or both, that is approved by the parties and creates new enforceable rights and obligations or changes existing ones. A modification may be written, oral, or implied by customary business practices.

The parties do not always need to have agreed on the final price for a modification to exist. If the parties have approved a change in scope but have not yet determined the corresponding change in price, the company estimates the change in transaction price using the variable consideration guidance.

A modification is accounted for as a separate contract only when both of the following conditions are met:

- The modification adds distinct goods or services.

- The contract price increases by an amount that reflects the standalone selling price of the additional goods or services, adjusted as appropriate for the facts and circumstances.

If those conditions are not met, the modification is accounted for as part of the existing contract. The accounting then depends on whether the remaining goods or services are distinct from the goods or services already transferred.

| Remaining goods or services | Accounting result |

|---|---|

| Remaining goods or services are distinct from those already transferred | Account for the modification as if the existing contract were terminated and a new contract were created for the remaining goods or services. |

| Remaining goods or services are not distinct and are part of a single performance obligation that is partially satisfied | Account for the modification as part of the existing contract and recognize a cumulative catch-up adjustment to revenue. |

| Remaining goods or services include both distinct and non-distinct elements | Apply an approach consistent with the objective of the modification guidance. |

Contract modifications are one of the first areas where the five-step model becomes judgment-heavy. The accounting depends on what changed, whether the added or remaining goods and services are distinct, and whether the pricing reflects standalone selling price.

Step 2: Identify the performance obligations

Once the company has identified the contract, the next question is what the company actually promised to transfer to the customer. Those promises determine the units of account for revenue recognition.

A performance obligation is a promise to transfer either a distinct good or service, a distinct bundle of goods or services, or a series of distinct goods or services that are substantially the same and have the same pattern of transfer to the customer.

Promises can be explicit or implicit

The contract often states the promised goods or services directly, but ASC 606 also captures implied promises. A promise may arise from customary business practices, published policies, or specific statements if, at contract inception, those practices or statements create a reasonable expectation that the company will transfer a good or service to the customer.

This means the performance obligation analysis should not stop with the contract document. The company also needs to consider what the customer reasonably expects based on the company’s past practices and communications.

Fulfillment activities are not necessarily promises

Not every activity performed under a contract is a promised good or service. Some activities are necessary to fulfill the contract but do not transfer a good or service to the customer.

For example, a company may perform administrative setup activities before it begins providing a service. Those activities may be necessary, but they are not performance obligations if the customer does not receive a good or service as the activities are performed. This distinction is important because costs and effort do not, by themselves, create revenue.

Immaterial promises

A company does not need to assess whether promised goods or services are performance obligations if they are immaterial in the context of the contract. That relief does not apply to a customer option that provides a material right.

Examples of promised goods or services

Promised goods or services can take many forms. They may include selling goods, reselling purchased goods, reselling rights to goods or services, performing services, standing ready to provide goods or services, arranging for another party to transfer goods or services, constructing or developing an asset for a customer, granting a license, or granting an option to purchase additional goods or services.

The point is not to categorize every activity mechanically. The question is whether the company has promised to transfer something to the customer.

Shipping and handling

Shipping and handling depends on timing. If shipping and handling activities occur before the customer obtains control of the related good, they are fulfillment activities rather than a separate promised service.

If shipping and handling activities occur after the customer obtains control, the company may elect to account for them as fulfillment activities rather than as a separate promised service. That election must be applied consistently to similar transactions. If revenue for the related good is recognized before shipping and handling occurs, the related costs are accrued.

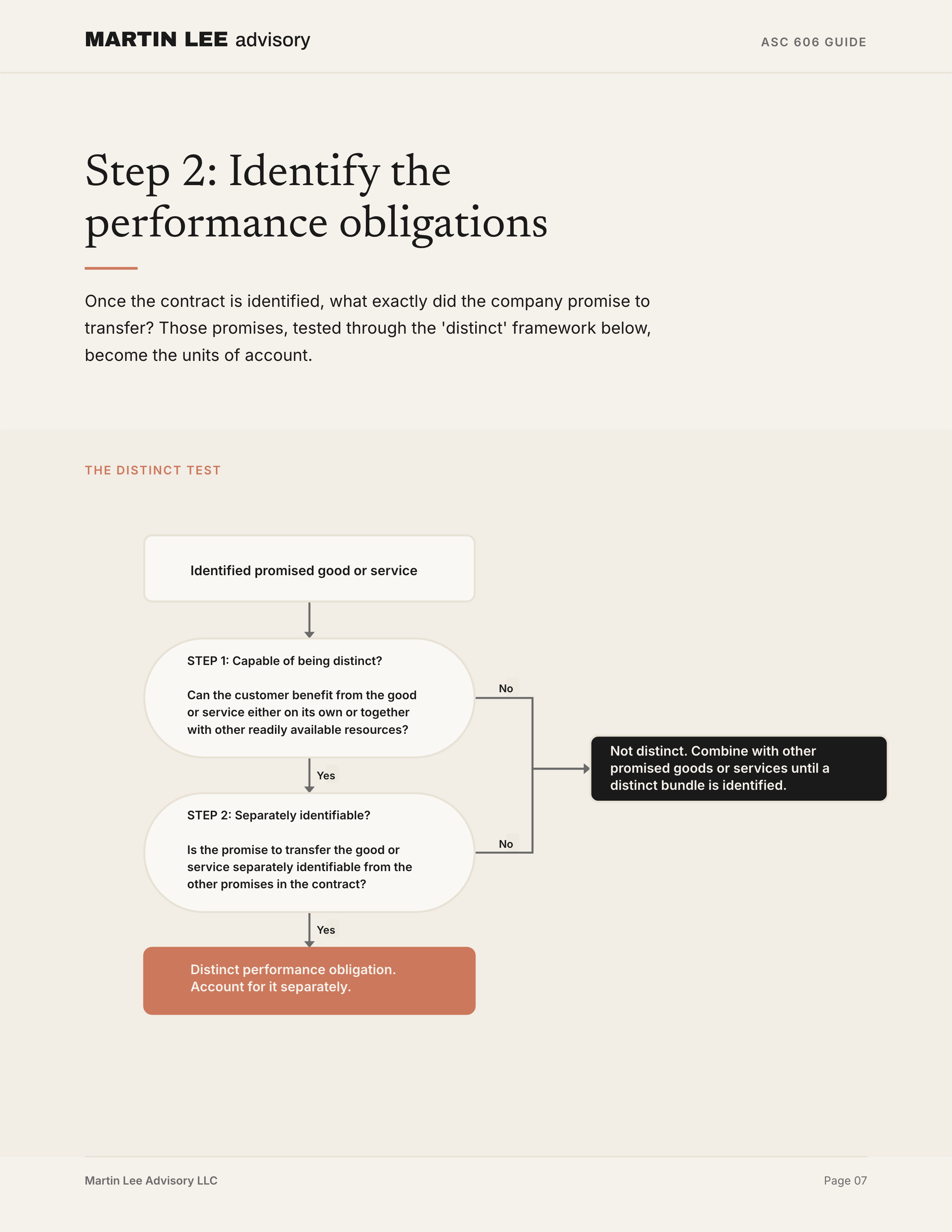

The distinct test

A promised good or service is distinct only if both conditions are met:

- The customer can benefit from the good or service either on its own or together with other readily available resources.

- The promise to transfer the good or service is separately identifiable from the other promises in the contract.

The first condition asks whether the good or service is capable of being distinct. The second asks whether the promise is distinct in the context of the contract.

The first condition is usually more straightforward. A customer can benefit from a good or service if it can be used, consumed, sold for more than scrap value, or otherwise held in a way that generates economic benefits. A readily available resource may be something sold separately by the company or another entity, or something the customer already has.

The second condition often requires more judgment. The question is whether the company is promising to transfer individual goods or services, or whether the company is promising to transfer a combined item for which the individual goods or services are inputs.

Factors that indicate promises are not separately identifiable include:

- the company provides a significant integration service;

- one or more goods or services significantly modifies or customizes another good or service; or

- the goods or services are highly interdependent or highly interrelated.

If a promised good or service is not distinct, the company combines it with other promised goods or services until it identifies a distinct bundle. In some arrangements, all promised goods or services are accounted for as a single performance obligation.

Series guidance

A series of distinct goods or services can be accounted for as one performance obligation if the goods or services are substantially the same and have the same pattern of transfer to the customer.

The same pattern of transfer exists when each distinct good or service in the series would be satisfied over time and the same method would be used to measure progress for each distinct good or service. This guidance is common in recurring service arrangements where the company provides substantially the same service over a period of time.

Step 3: Determine the transaction price

The transaction price is the amount of consideration the company expects to be entitled to receive in exchange for transferring promised goods or services to the customer. It excludes amounts collected on behalf of third parties, such as some sales taxes.

The transaction price may be fixed, variable, or a combination of both. The company determines the transaction price based on the contract terms and its customary business practices. For this purpose, the company assumes the existing contract will be performed as promised and will not be cancelled, renewed, or modified.

ASC 606 identifies five areas that may affect the transaction price:

- variable consideration;

- the constraint on variable consideration;

- significant financing components;

- noncash consideration; and

- consideration payable to a customer.

Sales tax and similar taxes

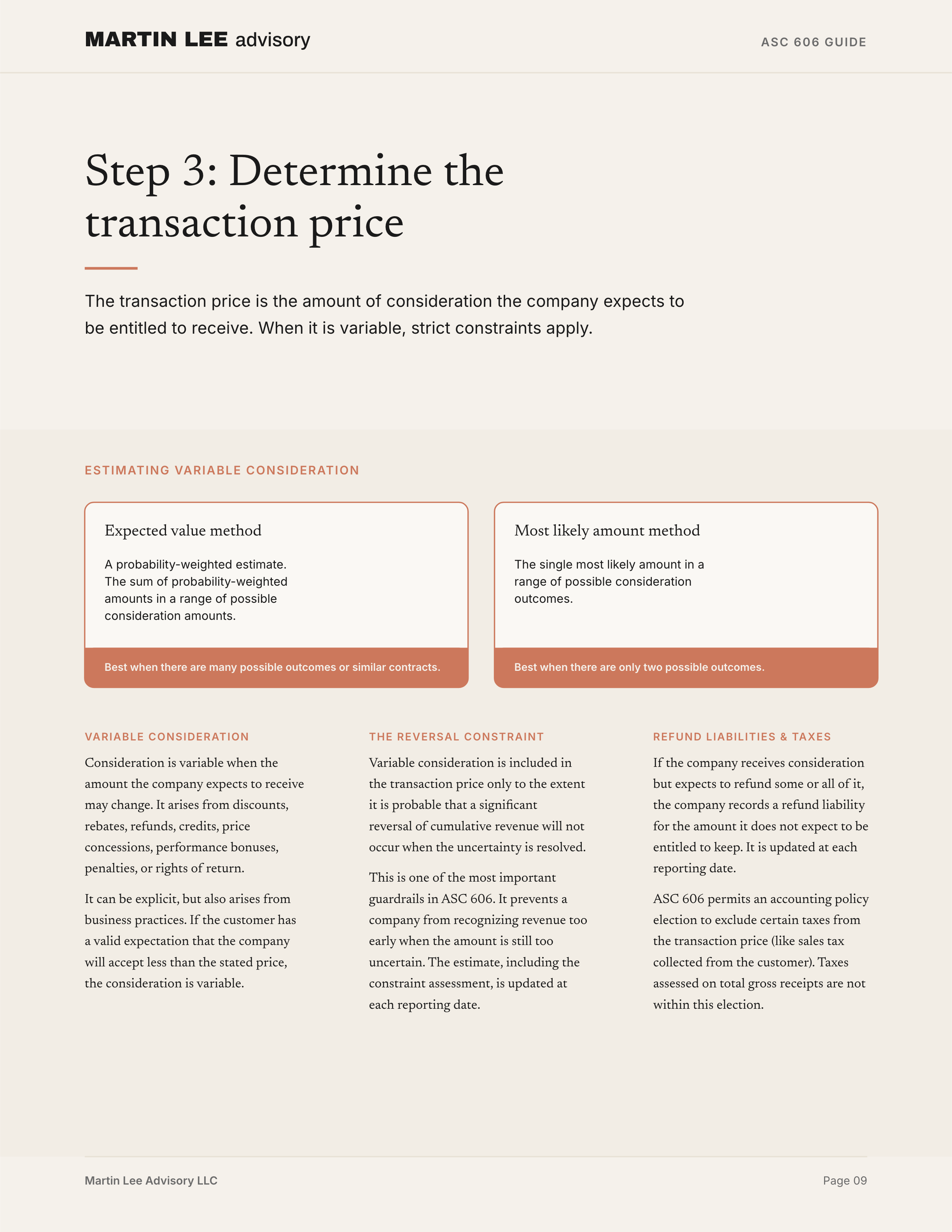

ASC 606 permits an accounting policy election to exclude certain taxes from the transaction price. The election applies to taxes assessed by a governmental authority that are both imposed on, and concurrent with, a specific revenue-producing transaction and collected from the customer. Examples may include some sales, use, value added, and excise taxes.

Taxes assessed on total gross receipts or imposed during inventory procurement are not within this election.

Variable consideration

Consideration is variable when the amount the company expects to receive may change. Variable consideration can arise from discounts, rebates, refunds, credits, price concessions, incentives, performance bonuses, penalties, rights of return, or similar items.

Variable consideration may be stated explicitly in the contract, but it can also arise from business practices. If the customer has a valid expectation that the company will accept less than the stated price, the promised consideration is variable even if the written contract appears fixed.

Estimating variable consideration

The company estimates variable consideration using the method that better predicts the amount it expects to receive. ASC 606 permits two methods:

| Method | Description |

|---|---|

| Expected value | A probability-weighted estimate. This method may be more appropriate when there are many possible outcomes or many similar contracts. |

| Most likely amount | The single most likely outcome. This method may be more appropriate when there are only a few possible outcomes, such as receiving or not receiving a performance bonus. |

The company applies the selected method consistently throughout the contract for the same uncertainty. The estimate should consider historical, current, and forecast information that is reasonably available.

Refund liabilities

If the company receives consideration but expects to refund some or all of it, the company records a refund liability for the amount it does not expect to be entitled to keep. The refund liability is updated at each reporting date for changes in facts and circumstances.

Constraint on variable consideration

Variable consideration is included in the transaction price only to the extent it is probable that a significant reversal of cumulative revenue will not occur when the uncertainty is resolved.

This is one of the most important guardrails in ASC 606. It prevents a company from recognizing revenue too early when the amount is still too uncertain.

The company considers both the likelihood and magnitude of a potential revenue reversal. Factors that may increase the risk of reversal include:

- the amount of consideration is highly susceptible to factors outside the company’s influence;

- the uncertainty is not expected to be resolved for a long period of time;

- the company has limited experience with similar contracts, or that experience has limited predictive value;

- the company has a practice of offering broad price concessions or changing payment terms; or

- the contract has a large number and broad range of possible consideration amounts.

The estimate of variable consideration, including the constraint assessment, is updated at each reporting date.

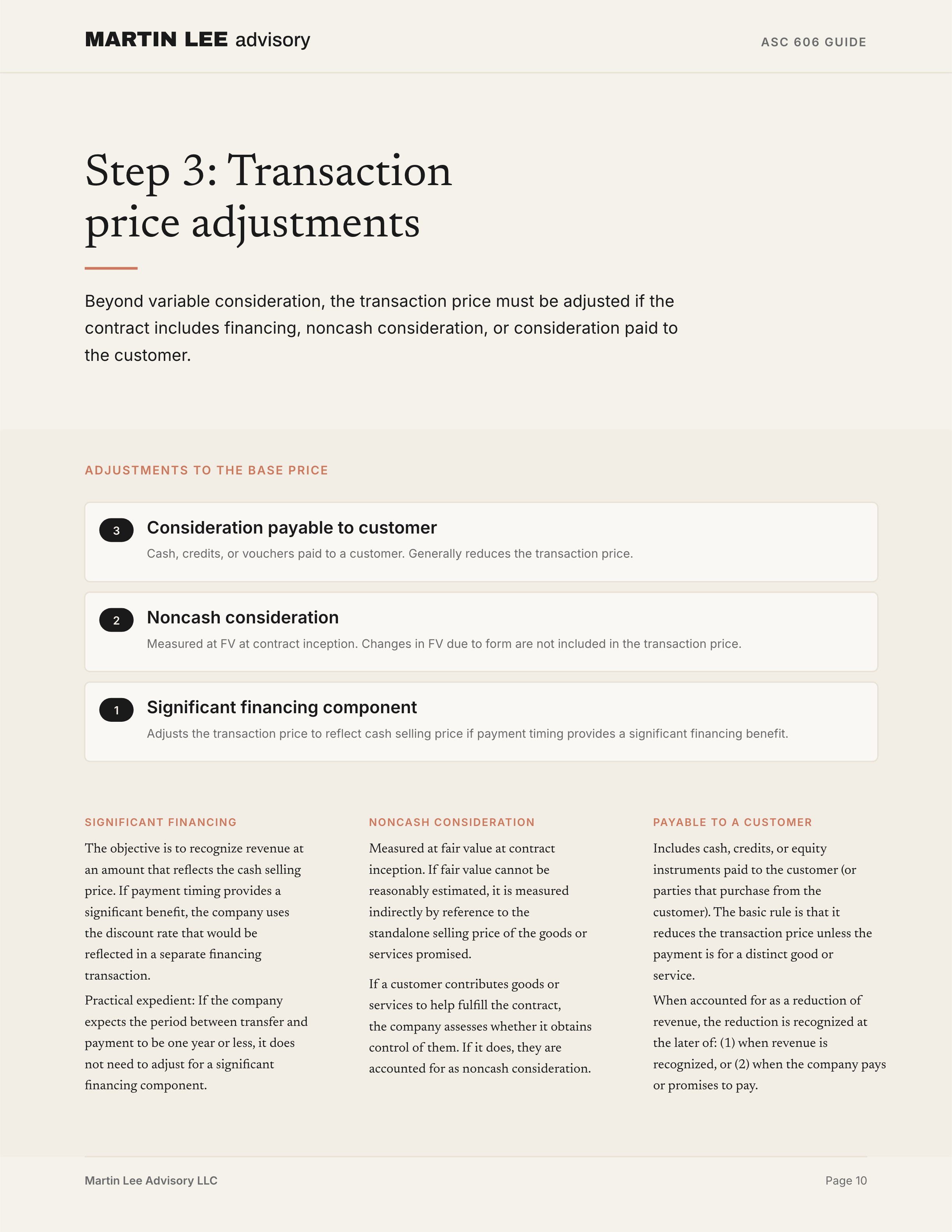

Significant financing component

A contract may include a significant financing component if the timing of payment provides a significant financing benefit to either the customer or the company. The financing component may be explicit in the contract or implicit in the payment terms.

The objective is to recognize revenue at an amount that reflects the cash selling price of the promised goods or services. In other words, revenue should reflect the price the customer would have paid if it had paid cash when the goods or services transferred.

A company considers factors such as the difference between the promised consideration and the cash selling price, the expected length of time between transfer and payment, and prevailing market interest rates.

Not every difference between payment timing and performance timing creates a significant financing component. ASC 606 identifies situations in which the timing difference may exist for reasons other than financing. For example, a customer may pay in advance while the timing of transfer is at the customer’s discretion. Consideration may be variable and depend on future events outside the control of both parties. Or the payment terms may be designed to protect one party from the other party’s failure to perform rather than to provide financing.

ASC 606 also includes a practical expedient. If, at contract inception, the company expects the period between transfer of the promised good or service and payment to be one year or less, the company does not need to adjust for a significant financing component.

If a significant financing component exists, the company uses the discount rate that would be reflected in a separate financing transaction between the company and the customer at contract inception. The rate is not updated after contract inception for changes in interest rates or credit risk. Interest income or interest expense from the financing component is presented separately from revenue.

Noncash consideration

If the customer promises consideration in a form other than cash, the company measures the noncash consideration at fair value at contract inception. If fair value cannot be reasonably estimated, the company measures the consideration indirectly by reference to the standalone selling price of the goods or services promised to the customer.

Changes in the fair value of noncash consideration after contract inception are treated differently depending on why the fair value changes. Changes due to the form of the consideration, such as changes in the price of shares, are not included in the transaction price. Changes due to reasons other than the form of the consideration may be treated as variable consideration.

If a customer contributes goods or services to help the company fulfill the contract, the company assesses whether it obtains control of those goods or services. If it does, the contributed goods or services are accounted for as noncash consideration.

Consideration payable to a customer

Consideration payable to a customer includes cash, credits, coupons, vouchers, or equity instruments that the company pays or expects to pay to the customer, or to other parties that purchase the company’s goods or services from the customer.

The basic rule is that consideration payable to a customer reduces the transaction price unless the payment is for a distinct good or service that the customer transfers to the company.

If the payment is for a distinct good or service from the customer, the company accounts for it like any other purchase from a supplier. If the payment exceeds the fair value of the distinct good or service, the excess reduces the transaction price. If the company cannot reasonably estimate the fair value of the good or service received from the customer, the entire payment reduces the transaction price.

When consideration payable to a customer is accounted for as a reduction of revenue, the reduction is recognized at the later of:

- when the company recognizes revenue for the related goods or services; or

- when the company pays or promises to pay the consideration.

The promise to pay may be explicit, or it may be implied by the company’s customary business practices.

Step 4: Allocate the transaction price

If a contract has only one performance obligation, allocation is usually straightforward: the transaction price is attributed to that performance obligation.

If a contract has more than one performance obligation, the company allocates the transaction price to each performance obligation in an amount that depicts the consideration the company expects to receive for transferring the related promised goods or services. The general approach is allocation based on relative standalone selling prices.

Standalone selling price

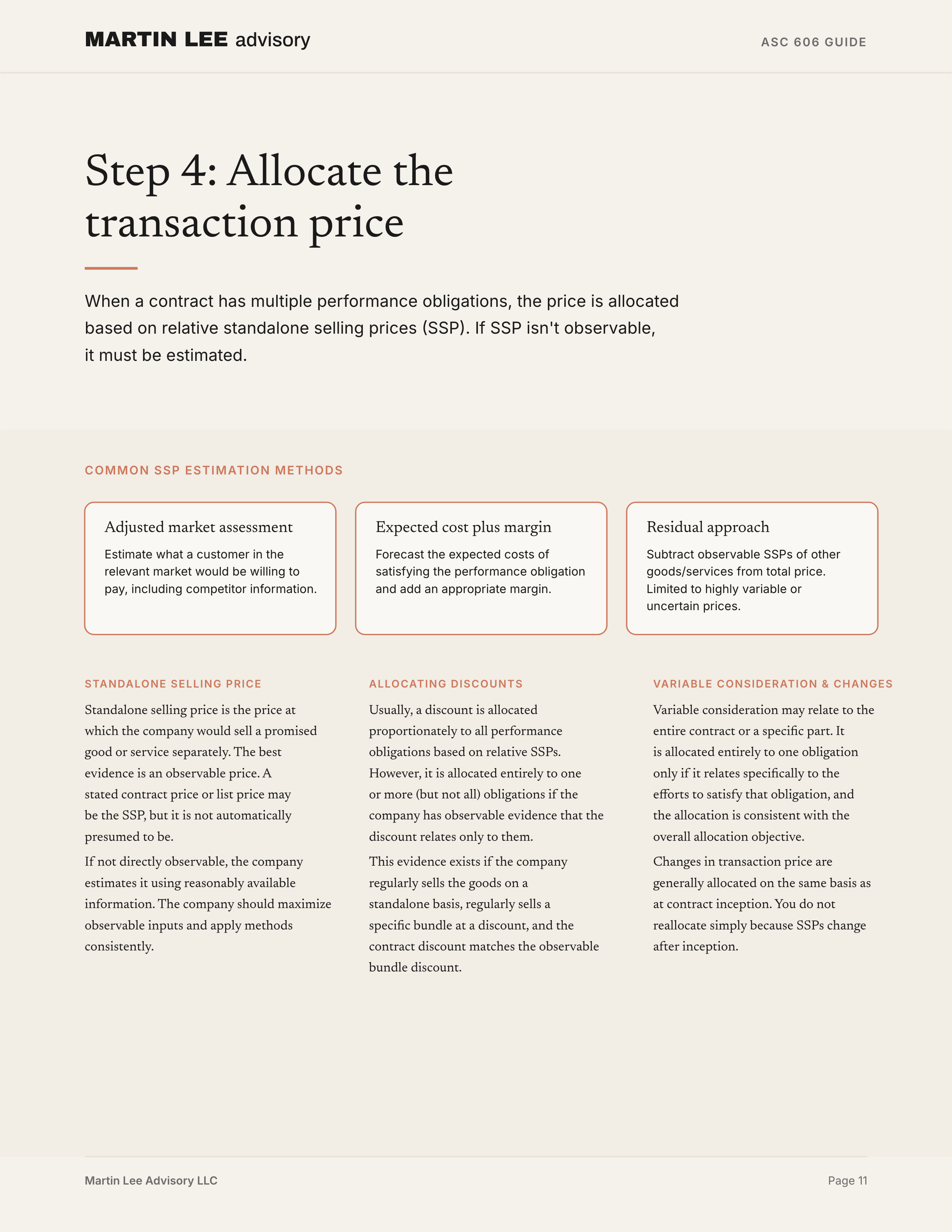

Standalone selling price is the price at which the company would sell a promised good or service separately to a customer.

The best evidence is an observable price when the company sells that good or service separately in similar circumstances and to similar customers. A stated contract price or list price may be the standalone selling price, but it is not automatically presumed to be the standalone selling price.

If the standalone selling price is not directly observable, the company estimates it using reasonably available information. That information may include market conditions, company-specific factors, and information about the customer or customer class. The company should maximize observable inputs and apply estimation methods consistently in similar circumstances.

Common estimation methods include:

| Method | Description |

|---|---|

| Adjusted market assessment | Estimate what a customer in the relevant market would be willing to pay, including competitor information if useful. |

| Expected cost plus margin | Forecast the expected costs of satisfying the performance obligation and add an appropriate margin. |

| Residual approach | Estimate the standalone selling price by subtracting observable standalone selling prices of other goods or services from the total transaction price. This approach is limited to specific circumstances. |

The residual approach can be used only when the selling price of the good or service is highly variable or uncertain.

Allocating discounts

A customer receives a discount when the sum of the standalone selling prices of the promised goods or services exceeds the promised consideration in the contract.

Usually, the discount is allocated proportionately to all performance obligations based on relative standalone selling prices. However, a discount is allocated entirely to one or more, but not all, performance obligations if the company has observable evidence that the discount relates only to those performance obligations.

That evidence exists when all of the following are true:

- The company regularly sells each distinct good or service, or each bundle of distinct goods or services, on a standalone basis.

- The company also regularly sells a bundle of some of those goods or services at a discount.

- The discount in the contract is substantially the same as the discount in those observable bundles, showing which performance obligation or obligations the discount belongs to.

If those criteria are not met, the discount is allocated proportionately across all performance obligations.

Allocating variable consideration

Variable consideration may relate to the entire contract or to a specific part of the contract. For example, a bonus may relate to one performance obligation, or an inflation adjustment may relate to a specific period in a series of distinct services.

A company allocates variable consideration entirely to one performance obligation, or to a distinct good or service within a series, only if both conditions are met:

- The variable payment relates specifically to the company’s efforts to satisfy that performance obligation or transfer that distinct good or service.

- Allocating the variable amount entirely to that performance obligation or distinct good or service is consistent with the overall allocation objective.

If those conditions are not met, the company applies the general allocation model.

Changes in transaction price

The transaction price can change after contract inception as uncertainties are resolved or circumstances change. In general, changes in transaction price are allocated to the performance obligations on the same basis as at contract inception. The company does not reallocate the transaction price simply because standalone selling prices change after inception.

If a change in transaction price is allocated to a performance obligation that has already been satisfied, the company recognizes the amount as revenue, or as a reduction of revenue, in the period of the change.

When the change in transaction price arises from a contract modification, the company applies the modification guidance first.

Step 5: Recognize revenue when or as performance obligations are satisfied

Revenue is recognized when, or as, the company satisfies a performance obligation by transferring control of a promised good or service to the customer.

Control means the ability to direct the use of, and obtain substantially all of the remaining benefits from, an asset. Control also includes the ability to prevent others from directing the use of, or obtaining the benefits from, that asset.

Benefits from an asset may come from using it, consuming it, selling it, exchanging it, pledging it, holding it, using it to produce goods or services, using it to enhance other assets, or using it to settle liabilities or reduce expenses.

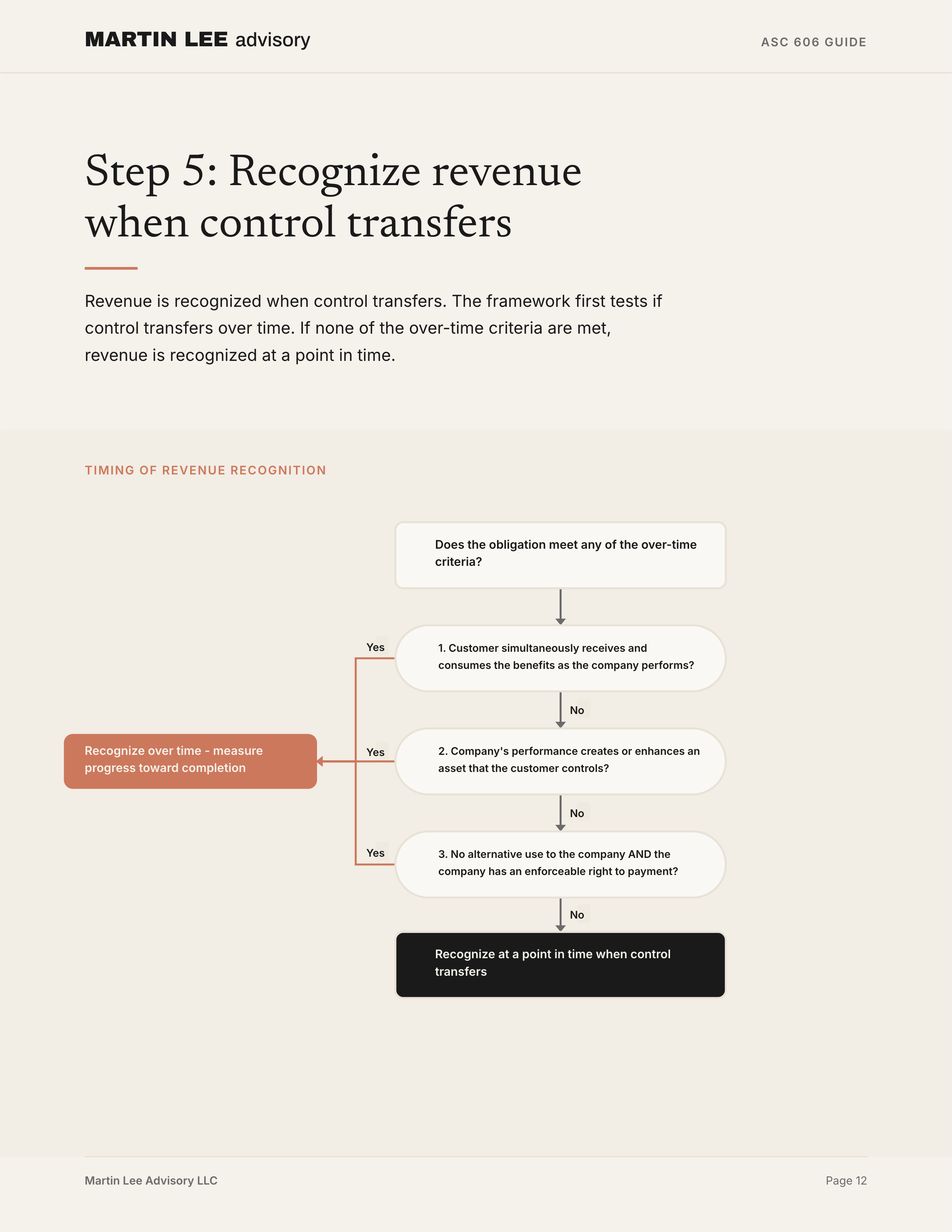

For each performance obligation, the company determines at contract inception whether the obligation is satisfied over time or at a point in time. If the obligation is not satisfied over time, it is satisfied at a point in time.

Performance obligations satisfied over time

A performance obligation is satisfied over time if any one of the following criteria is met:

- The customer simultaneously receives and consumes the benefits of the company’s performance as the company performs.

- The company’s performance creates or enhances an asset that the customer controls as the asset is created or enhanced.

- The company’s performance does not create an asset with an alternative use to the company, and the company has an enforceable right to payment for performance completed to date.

The third criterion has two parts, and both must be met.

First, the asset must have no alternative use to the company. That may be because the company is contractually restricted from redirecting the asset during development, or because the company is practically limited from redirecting the completed asset without significant economic loss. This assessment is made at contract inception and is not updated unless the parties approve a contract modification that substantively changes the performance obligation.

Second, the company must have an enforceable right to payment for performance completed to date. The right does not need to be a present unconditional right to payment, but throughout the contract the company must be entitled to an amount that at least compensates it for performance completed to date if the customer or another party terminates the contract for reasons other than the company’s failure to perform.

Performance obligations satisfied at a point in time

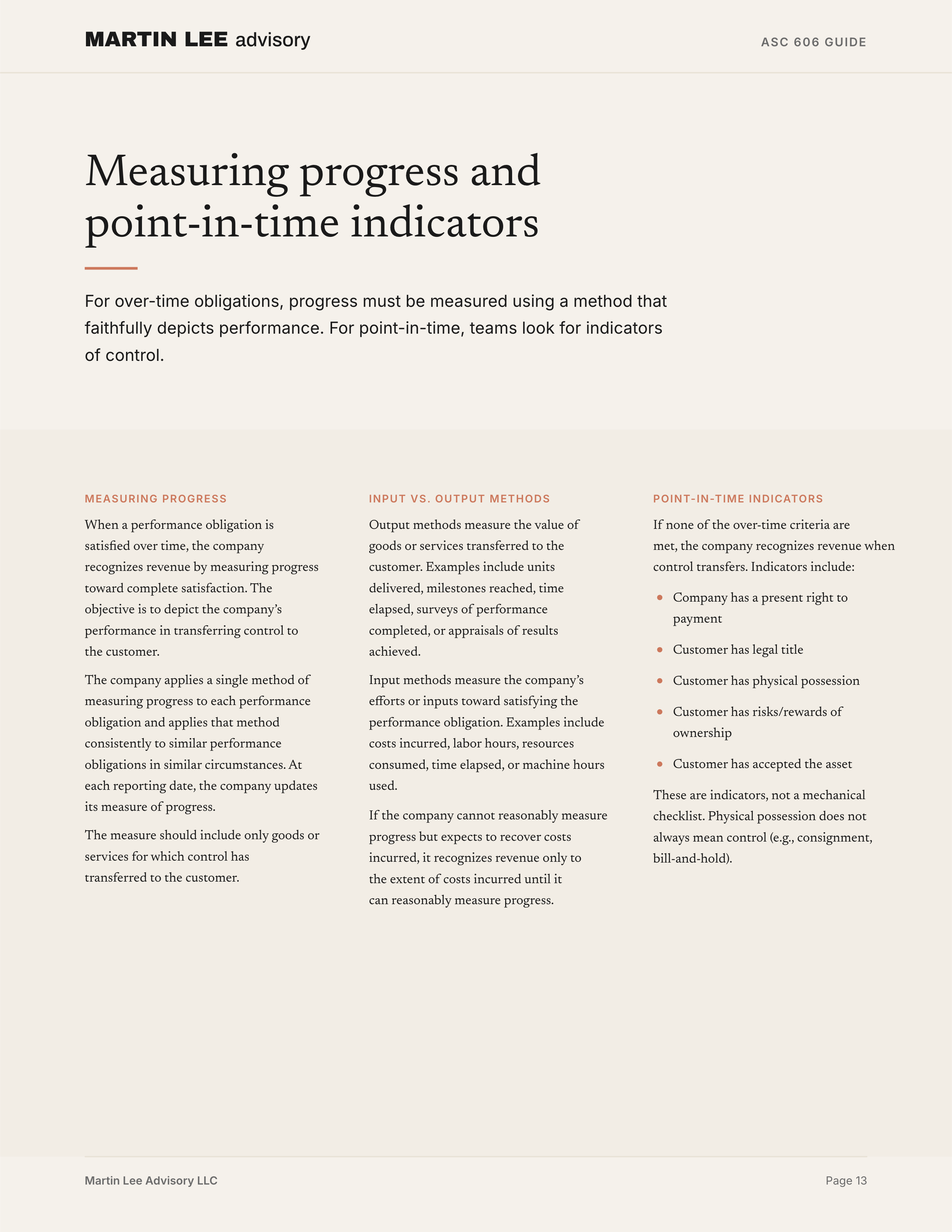

If none of the over-time criteria are met, the performance obligation is satisfied at a point in time. The company recognizes revenue when control transfers to the customer.

Indicators of control transfer include:

- the company has a present right to payment;

- the customer has legal title;

- the customer has physical possession;

- the customer has the significant risks and rewards of ownership; and

- the customer has accepted the asset.

These are indicators, not a mechanical checklist. The purpose is to determine when the customer obtains control.

Physical possession does not always mean control has transferred. In some repurchase or consignment arrangements, the customer may have physical possession of an asset that the company still controls. In some bill-and-hold arrangements, the company may have physical possession of an asset that the customer controls.

Measuring progress for performance obligations satisfied over time

When a performance obligation is satisfied over time, the company recognizes revenue by measuring progress toward complete satisfaction of the obligation. The objective is to depict the company’s performance in transferring control of promised goods or services to the customer.

The company applies a single method of measuring progress to each performance obligation and applies that method consistently to similar performance obligations in similar circumstances. At each reporting date, the company updates its measure of progress.

Appropriate methods include output methods and input methods.

Output methods measure the value of goods or services transferred to the customer. Examples include units delivered, milestones reached, time elapsed, surveys of performance completed, or appraisals of results achieved.

Input methods measure the company’s efforts or inputs toward satisfying the performance obligation. Examples include costs incurred, labor hours, resources consumed, time elapsed, or machine hours used.

The measure of progress should include only goods or services for which control has transferred to the customer. It should exclude goods or services for which control has not transferred. If the company cannot reasonably measure progress but expects to recover the costs incurred, it recognizes revenue only to the extent of costs incurred until it can reasonably measure progress.

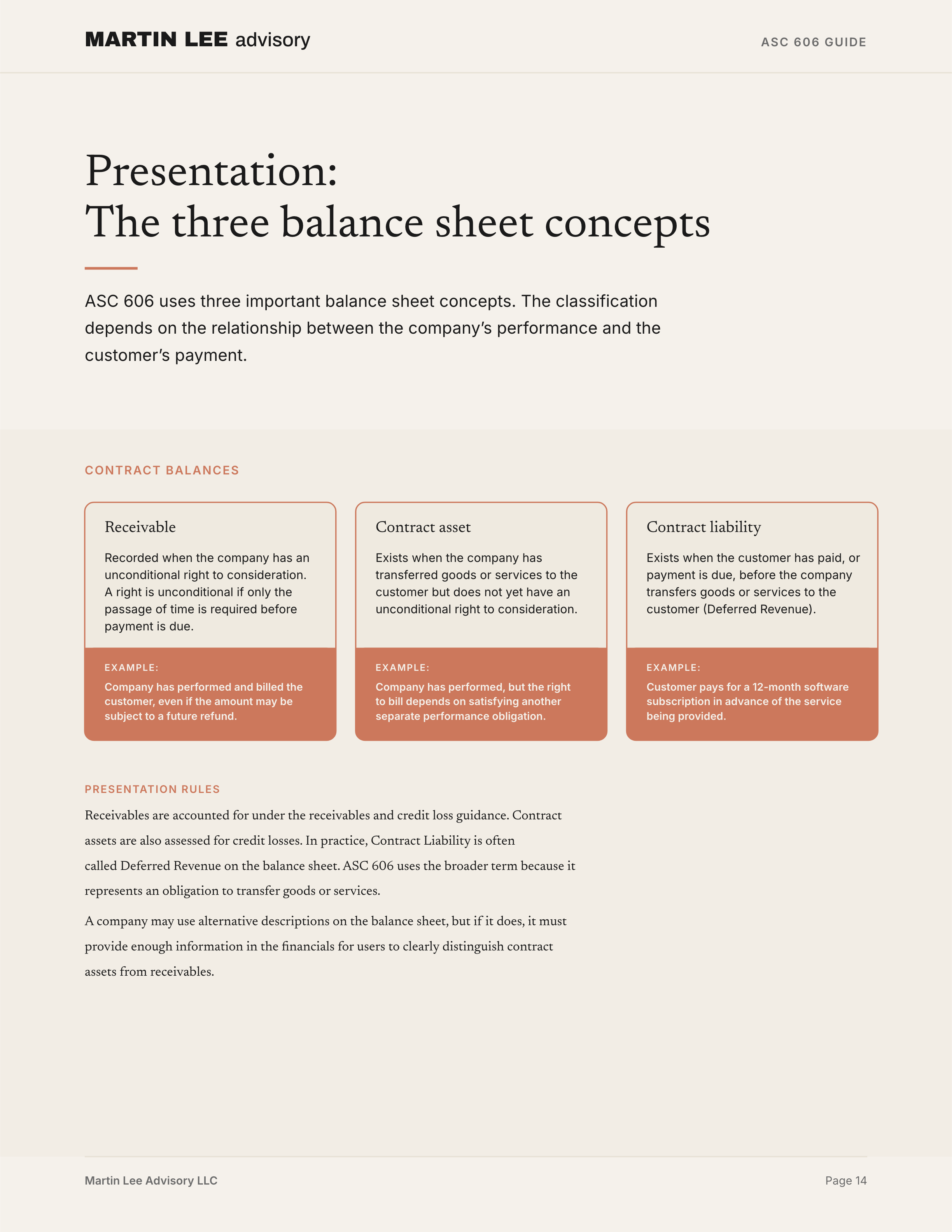

Presentation: receivable, contract asset, or contract liability

ASC 606 uses three important balance sheet concepts: receivable, contract asset, and contract liability. The classification depends on the relationship between the company’s performance and the customer’s payment.

Receivable

A receivable is recorded when the company has an unconditional right to consideration. A right is unconditional if only the passage of time is required before payment is due.

For example, if the company has a present right to payment, it records a receivable even if the amount may be subject to refund in the future. Receivables are accounted for under the receivables and credit loss guidance.

Contract asset

A contract asset exists when the company has transferred goods or services to the customer but does not yet have an unconditional right to consideration.

For example, the company may have performed, but its right to payment may depend on satisfying another performance obligation. Contract assets are assessed for credit losses.

Contract liability

A contract liability exists when the customer has paid, or payment is due, before the company transfers goods or services to the customer.

In practice, this is often called deferred revenue. ASC 606 uses the broader term contract liability because the liability represents an obligation to transfer goods or services to the customer.

A company may use alternative descriptions on the balance sheet, but if it does, it must provide enough information for users to distinguish contract assets from receivables.

Disclosure: what users need to understand

The disclosure objective is to help users understand the nature, amount, timing, and uncertainty of revenue and cash flows from contracts with customers. The point is not to produce a checklist for its own sake. The point is to explain how revenue is generated, when it is recognized, what judgments affect it, and what uncertainty remains.

ASC 606 requires qualitative and quantitative information about:

- contracts with customers;

- significant judgments, and changes in judgments, made in applying the guidance; and

- assets recognized from costs to obtain or fulfill contracts with customers.

The level of detail should be useful. The standard cautions against obscuring useful information by including too much insignificant detail or by aggregating items that have substantially different characteristics.

Contracts with customers

Companies disclose revenue recognized from contracts with customers separately from other sources of revenue unless it is already separately presented. They also disclose credit losses on receivables or contract assets from contracts with customers separately from credit losses from other contracts.

Disaggregated revenue

Companies disaggregate revenue into categories that show how economic factors affect the nature, amount, timing, and uncertainty of revenue and cash flows.

Possible categories include type of good or service, geography, market or customer type, contract type, contract duration, timing of transfer, and sales channel. Private companies and certain other nonpublic entities have relief from some quantitative disaggregation requirements, but they still must provide certain minimum information if they elect that relief.

Contract balances

Companies disclose opening and closing balances of receivables, contract assets, and contract liabilities if those balances are not otherwise presented or disclosed. They also disclose revenue recognized during the period that was included in the beginning contract liability balance.

The company explains how the timing of performance relates to the timing of payment and how that relationship affects contract asset and contract liability balances.

Performance obligations

Companies disclose information about their performance obligations, including when performance obligations are typically satisfied, significant payment terms, the nature of promised goods or services, whether the company is arranging for another party to transfer goods or services, obligations for returns and refunds, and types of warranties.

Public business entities and certain other entities also disclose information about remaining performance obligations, including the aggregate amount of transaction price allocated to unsatisfied or partially unsatisfied performance obligations and when the company expects to recognize that amount as revenue. ASC 606 includes optional exemptions for certain remaining performance obligation disclosures.

Significant judgments

Companies disclose judgments, and changes in judgments, that significantly affect the amount and timing of revenue.

These judgments may include:

- when performance obligations are satisfied;

- methods used to recognize revenue over time;

- why those methods faithfully depict transfer of goods or services;

- when control transfers for point-in-time obligations;

- determining the transaction price;

- estimating and constraining variable consideration;

- measuring noncash consideration;

- allocating the transaction price;

- estimating standalone selling prices;

- allocating discounts and variable consideration; and

- measuring obligations for returns, refunds, and similar items.

Practical expedients

Companies disclose certain practical expedients they elect, such as the practical expedient for significant financing components when the period between transfer and payment is expected to be one year or less.

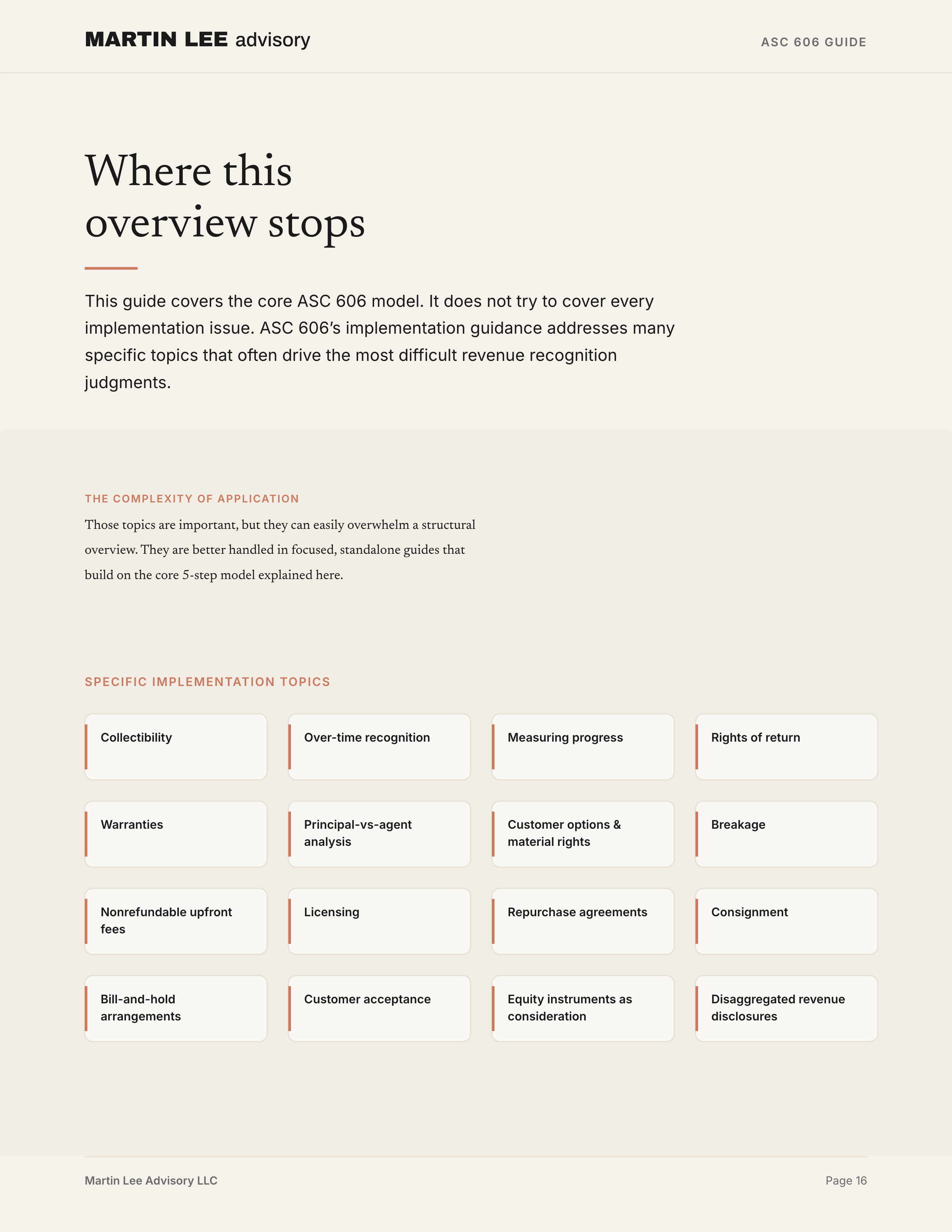

Where this overview stops

This guide covers the core ASC 606 model. It does not cover every implementation issue.

ASC 606’s implementation guidance addresses many topics that often drive the most difficult revenue recognition judgments, including:

- collectibility,

- over-time recognition,

- measuring progress,

- rights of return,

- warranties,

- principal-versus-agent analysis,

- customer options and material rights,

- breakage,

- nonrefundable upfront fees,

- licensing,

- repurchase agreements,

- consignment,

- bill-and-hold arrangements,

- customer acceptance,

- equity instruments granted as consideration payable to a customer, and

- disaggregated revenue disclosures.

Those topics are important, but they can overwhelm an overview. They are better handled in focused guides that build on the core model explained here.