ASC 340-40 Other Assets and Deferred Costs — A Concise Guide to Contract Costs

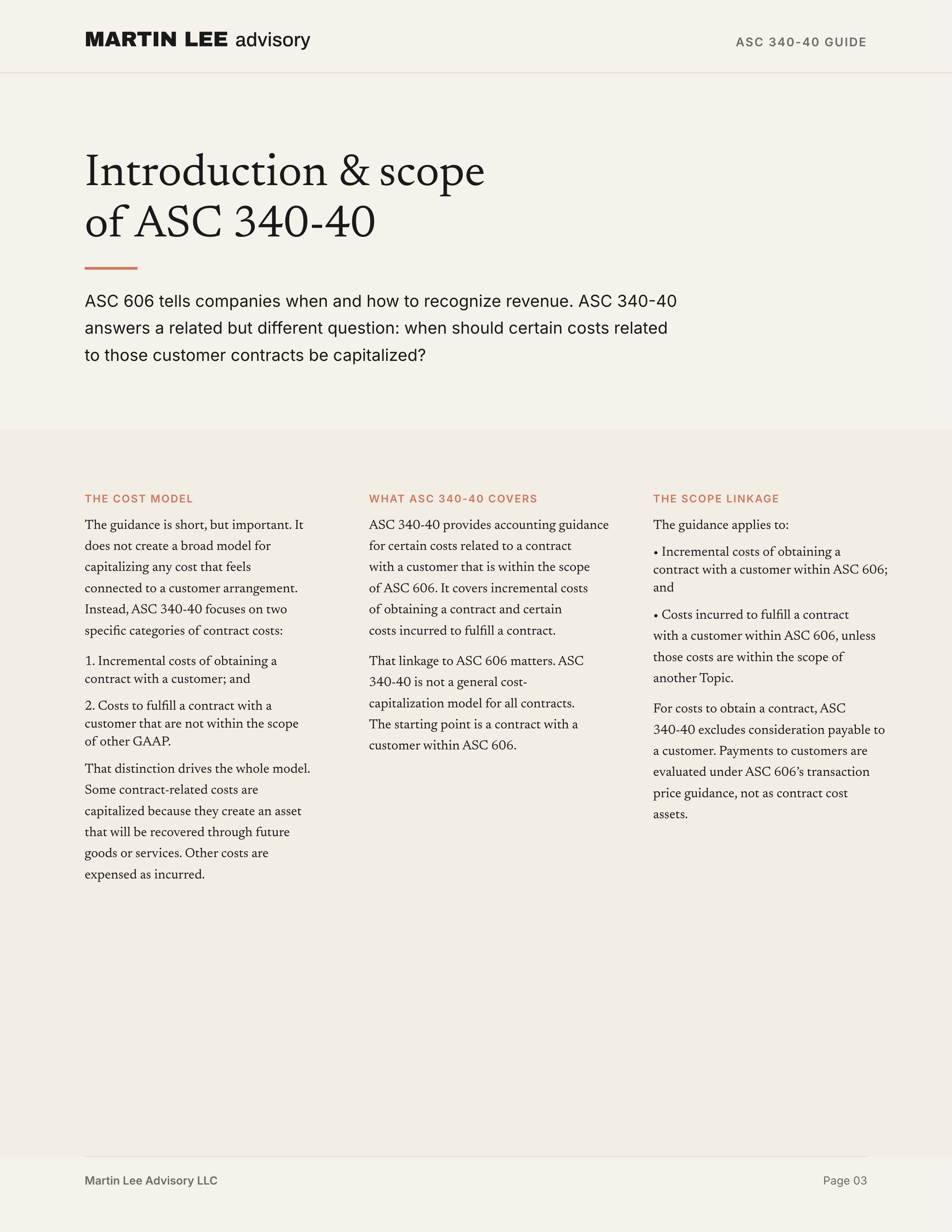

ASC 606 tells companies when and how to recognize revenue from contracts with customers. ASC 340-40 answers a related but different question: when should certain costs related to those customer contracts be capitalized?

The guidance is short, but important. It does not create a broad model for capitalizing any cost that feels connected to a customer arrangement. Instead, ASC 340-40 focuses on two specific categories of contract costs:

- incremental costs of obtaining a contract with a customer; and

- costs to fulfill a contract with a customer that are not within the scope of other GAAP.

That distinction drives the whole model. Some contract-related costs are capitalized because they create an asset that will be recovered through future goods or services. Other costs are expensed as incurred because they would have been incurred anyway, relate to past performance, do not create or enhance resources for future performance, or are covered by another accounting Topic.

What ASC 340-40 covers

ASC 340-40 provides accounting guidance for certain costs related to a contract with a customer that is within the scope of ASC 606. It covers incremental costs of obtaining a contract and certain costs incurred to fulfill a contract.

That linkage to ASC 606 matters. ASC 340-40 is not a general cost-capitalization model for all contracts. The starting point is a contract with a customer within ASC 606.

The guidance applies to:

- incremental costs of obtaining a contract with a customer within ASC 606; and

- costs incurred to fulfill a contract with a customer within ASC 606, unless those costs are within the scope of another Topic.

For costs to obtain a contract, ASC 340-40 excludes consideration payable to a customer. Payments to customers are evaluated under ASC 606’s transaction price guidance, not as contract cost assets.

For costs to fulfill a contract, ASC 340-40 applies only if the costs are not already addressed by other GAAP. If another Topic applies, the company uses that other guidance first. Examples include inventory, preproduction costs related to long-term supply arrangements, internal-use software, property, plant, and equipment, and software to be sold, leased, or otherwise marketed.

How ASC 340-40 fits with ASC 606

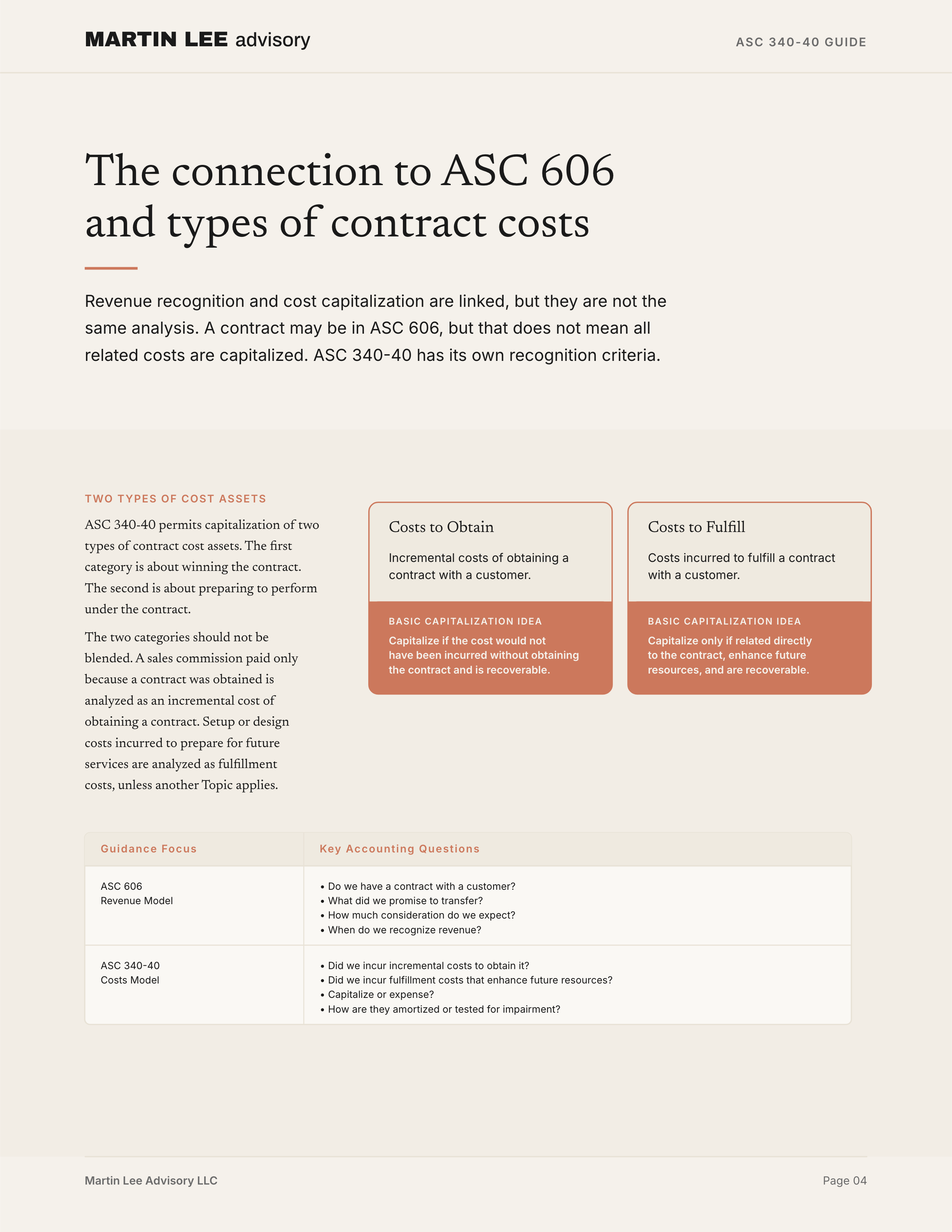

ASC 606 and ASC 340-40 are connected, but they answer different questions.

ASC 606 focuses on revenue:

| Question | Guidance |

|---|---|

| Do we have a contract with a customer? | ASC 606 |

| What did we promise to transfer? | ASC 606 |

| How much consideration do we expect to receive? | ASC 606 |

| When do we recognize revenue? | ASC 606 |

ASC 340-40 focuses on certain related costs:

| Question | Guidance |

|---|---|

| Did we incur incremental costs to obtain the customer contract? | ASC 340-40 |

| Did we incur fulfillment costs that create or enhance resources for future performance? | ASC 340-40 |

| Should those costs be capitalized or expensed? | ASC 340-40 |

| If capitalized, how are they amortized and tested for impairment? | ASC 340-40 |

The practical point is this: revenue recognition and cost capitalization are linked, but they are not the same analysis. A contract may be in ASC 606, but that does not mean all related costs are capitalized. ASC 340-40 has its own recognition criteria.

Two types of contract cost assets

ASC 340-40 permits capitalization of two types of contract cost assets.

| Type of cost | Basic capitalization idea |

|---|---|

| Incremental costs of obtaining a contract | Capitalize if the cost would not have been incurred without obtaining the contract and the company expects to recover it. |

| Costs to fulfill a contract | Capitalize only if the costs relate directly to a specific contract or anticipated contract, generate or enhance resources used to satisfy future performance obligations, and are expected to be recovered. |

The first category is about winning the contract. The second is about preparing to perform under the contract.

The two categories should not be blended. A sales commission paid only because a contract was obtained is analyzed as an incremental cost of obtaining a contract. Setup or design costs incurred to prepare for future services are analyzed as fulfillment costs, unless another Topic applies.

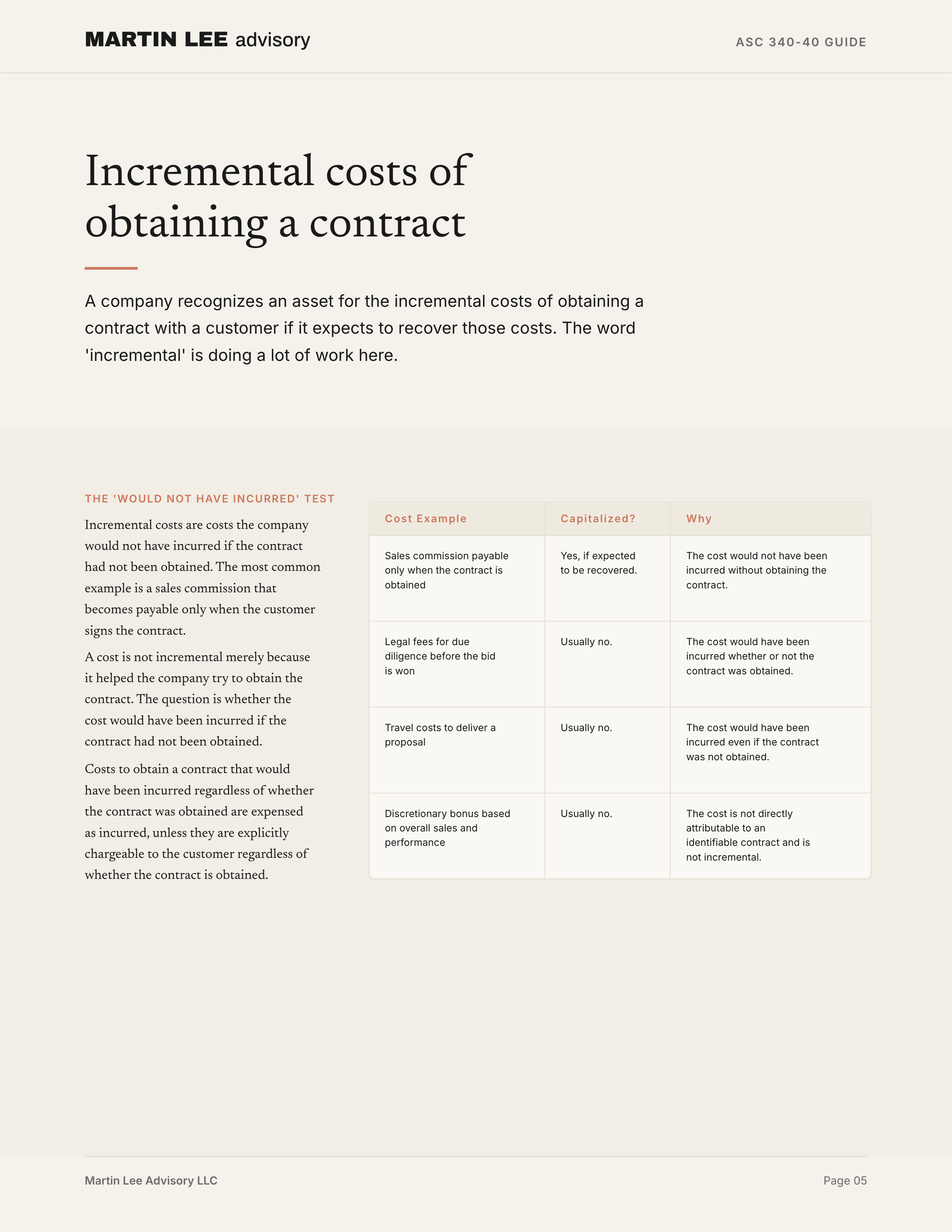

Incremental costs of obtaining a contract

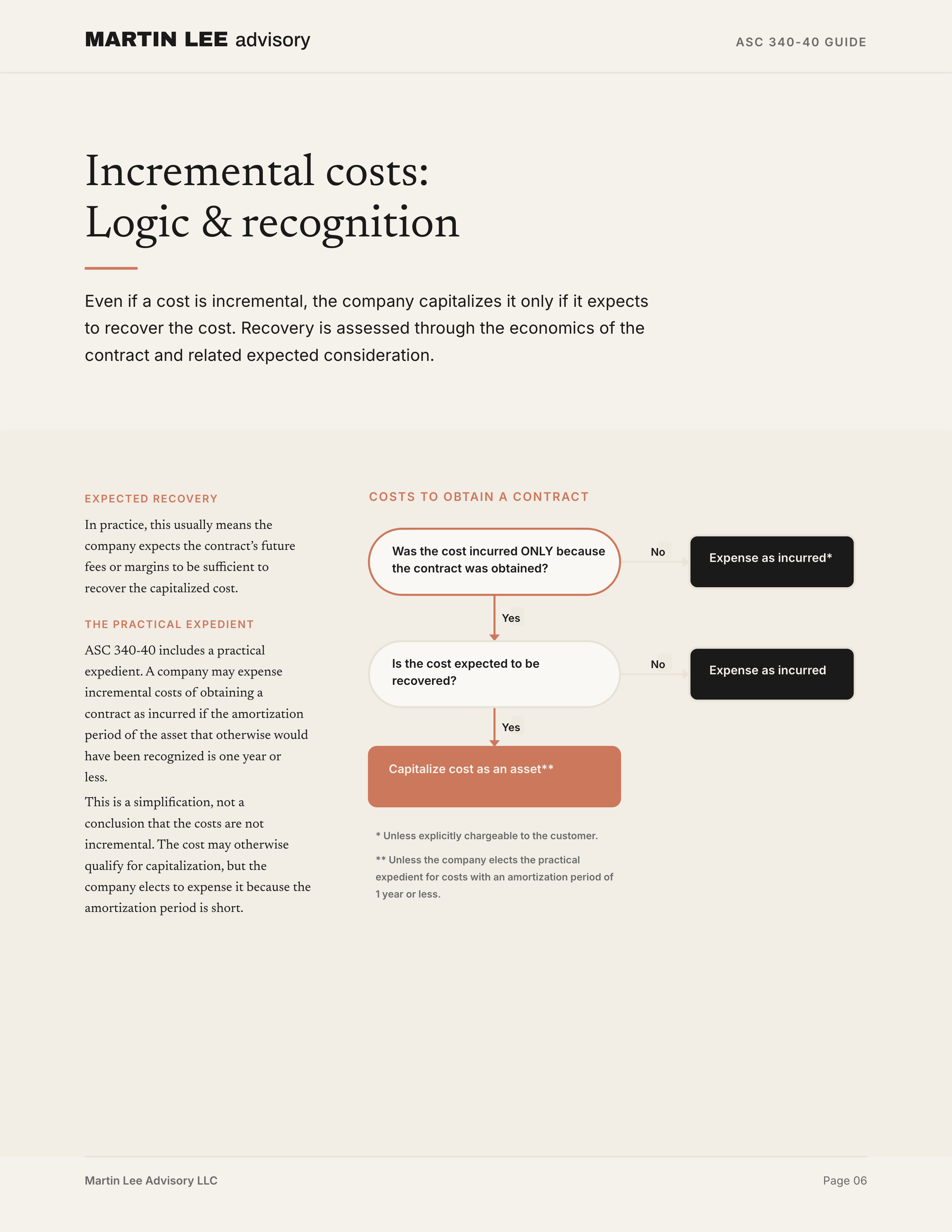

A company recognizes an asset for the incremental costs of obtaining a contract with a customer if it expects to recover those costs.

The word “incremental” is doing a lot of work. Incremental costs are costs the company would not have incurred if the contract had not been obtained. The most common example is a sales commission that becomes payable only when the customer signs the contract.

A cost is not incremental merely because it helped the company try to obtain the contract. The question is whether the cost would have been incurred if the contract had not been obtained.

For example:

| Cost | Usually capitalized? | Why |

|---|---|---|

| Sales commission payable only when the contract is obtained | Yes, if expected to be recovered | The cost would not have been incurred without obtaining the contract. |

| Legal fees for due diligence before the bid is won | Usually no | The cost would have been incurred whether or not the contract was obtained. |

| Travel costs to deliver a proposal | Usually no | The cost would have been incurred even if the contract was not obtained. |

| Discretionary bonus based on overall sales, profitability, and performance | Usually no | The cost is not directly attributable to an identifiable contract and is not incremental to obtaining that contract. |

Costs to obtain a contract that would have been incurred regardless of whether the contract was obtained are expensed as incurred, unless they are explicitly chargeable to the customer regardless of whether the contract is obtained.

Expected recovery

Even if a cost is incremental, the company capitalizes it only if it expects to recover the cost. Recovery is assessed through the economics of the contract and related expected consideration. In practice, this usually means the company expects the contract’s future fees or margins to be sufficient to recover the capitalized cost.

Practical expedient for short amortization periods

ASC 340-40 includes a practical expedient. A company may expense incremental costs of obtaining a contract as incurred if the amortization period of the asset that otherwise would have been recognized is one year or less.

This is a simplification, not a conclusion that the costs are not incremental. The cost may otherwise qualify for capitalization, but the company elects to expense it because the amortization period is short.

Costs to fulfill a contract

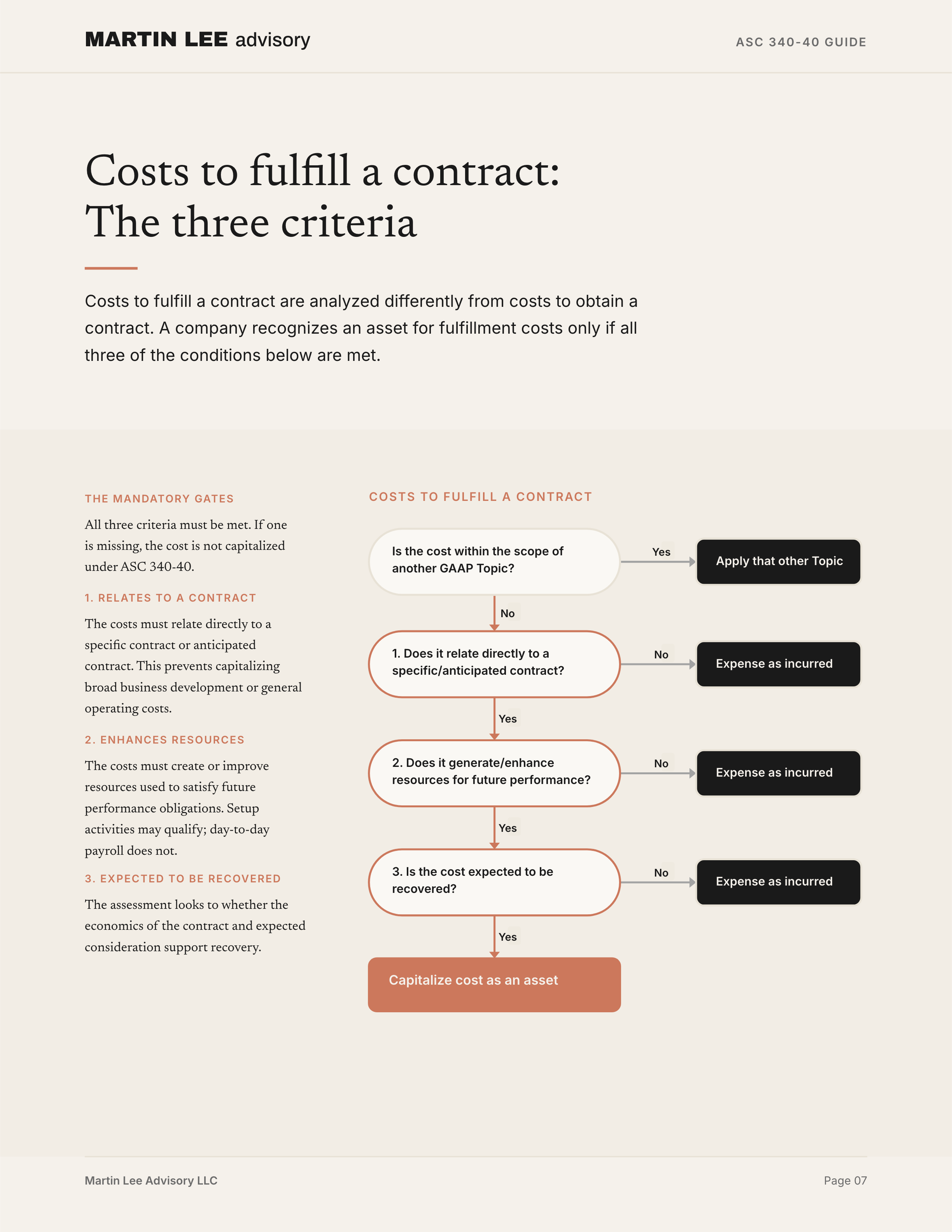

Costs to fulfill a contract are analyzed differently from costs to obtain a contract.

A company recognizes an asset for costs incurred to fulfill a contract only if all three conditions are met:

- The costs relate directly to a contract or to a specific anticipated contract that the company can identify.

- The costs generate or enhance resources of the company that will be used to satisfy, or continue satisfying, performance obligations in the future.

- The costs are expected to be recovered.

All three criteria must be met. If one is missing, the cost is not capitalized under ASC 340-40.

Criterion 1: The costs relate directly to a specific contract or anticipated contract

The costs must relate directly to a specific contract or to a specific anticipated contract that the company can identify. This can include costs related to services expected to be provided under renewal of an existing contract or costs of designing an asset to be transferred under a specific contract that has not yet been approved.

This criterion prevents companies from capitalizing broad business development, general operating, or speculative costs that are not tied to a specific customer contract or identifiable anticipated contract.

Criterion 2: The costs generate or enhance resources used for future performance

The costs must create or improve resources that the company will use to satisfy performance obligations in the future.

This is often the hardest part of the analysis. It is not enough that the cost is related to the contract. The cost must generate or enhance a resource of the company. That resource must then be used in satisfying, or continuing to satisfy, performance obligations in the future.

For example, setup activities may qualify if they create resources that will be used to provide future services. By contrast, payroll costs for employees providing day-to-day services to a customer generally do not create or enhance a resource for future performance; they are costs of current performance.

Criterion 3: The costs are expected to be recovered

The company must expect to recover the costs. Similar to costs of obtaining a contract, this assessment looks to whether the economics of the contract and related expected consideration support recovery.

Costs that relate directly to a contract

ASC 340-40 gives examples of costs that may relate directly to a contract or a specific anticipated contract, including:

- direct labor, such as salaries and wages of employees who provide the promised services directly to the customer;

- direct materials, such as supplies used in providing promised services;

- allocations of costs that relate directly to the contract or contract activities, such as contract management and supervision, insurance, and depreciation of tools and equipment used in fulfilling the contract;

- costs that are explicitly chargeable to the customer under the contract; and

- other costs incurred only because the company entered into the contract, such as payments to subcontractors.

This list does not mean all of those costs are automatically capitalized. The three capitalization criteria still apply. For example, a direct labor cost may relate directly to a contract, but if it relates to a satisfied or partially satisfied performance obligation, or does not generate or enhance resources for future performance, it is expensed as incurred.

Costs accounted for under other GAAP

ASC 340-40 is a residual model for fulfillment costs. It applies only when the fulfillment costs are not within the scope of another Topic.

If another Topic applies, the company accounts for the cost under that Topic instead of ASC 340-40. Examples include:

| Type of cost | Apply first |

|---|---|

| Inventory | ASC 330 |

| Preproduction costs related to long-term supply arrangements | ASC 340-10 |

| Internal-use software | ASC 350-40 |

| Property, plant, and equipment | ASC 360 |

| Software to be sold, leased, or otherwise marketed | ASC 985-20 |

This is important because a cost may be related to a customer contract but still not be evaluated under ASC 340-40. For example, hardware acquired to support a customer arrangement may be accounted for under property, plant, and equipment guidance. Internal-use software developed to support service delivery may be accounted for under ASC 350-40.

Costs expensed as incurred

ASC 340-40 specifically identifies costs that are expensed as incurred. These include:

- general and administrative costs, unless they are explicitly chargeable to the customer under the contract;

- wasted materials, labor, or other resources that were not reflected in the contract price;

- costs that relate to satisfied or partially satisfied performance obligations; and

- costs for which the company cannot distinguish whether they relate to unsatisfied performance obligations or to satisfied or partially satisfied performance obligations.

These rules are designed to keep the model tied to future performance. Costs related to past performance are expensed. Costs that cannot be connected to future performance are expensed. Waste is expensed unless it was reflected in the pricing of the contract. General administrative costs are expensed unless the contract explicitly makes them chargeable to the customer.

The practical takeaway is that ASC 340-40 does not allow companies to defer costs simply because the related revenue will be recognized later. The cost must meet the applicable capitalization model.

Amortization

A contract cost asset recognized under ASC 340-40 is amortized on a systematic basis consistent with the transfer to the customer of the goods or services to which the asset relates.

This means the amortization pattern follows the related goods or services. If the asset relates to services transferred over time, amortization typically follows the pattern of those services. If the asset relates to goods or services expected to be transferred under a specific anticipated contract, the amortization period includes those expected goods or services.

The amortization period may extend beyond the initial contract term if the asset relates to expected renewals or extensions. The standard’s examples show a commission asset amortized over seven years when the initial contract term is five years and the entity anticipates two additional one-year renewal periods based on the expected customer term.

If the expected timing of transfer changes significantly, the company updates the amortization pattern. That change is accounted for as a change in accounting estimate.

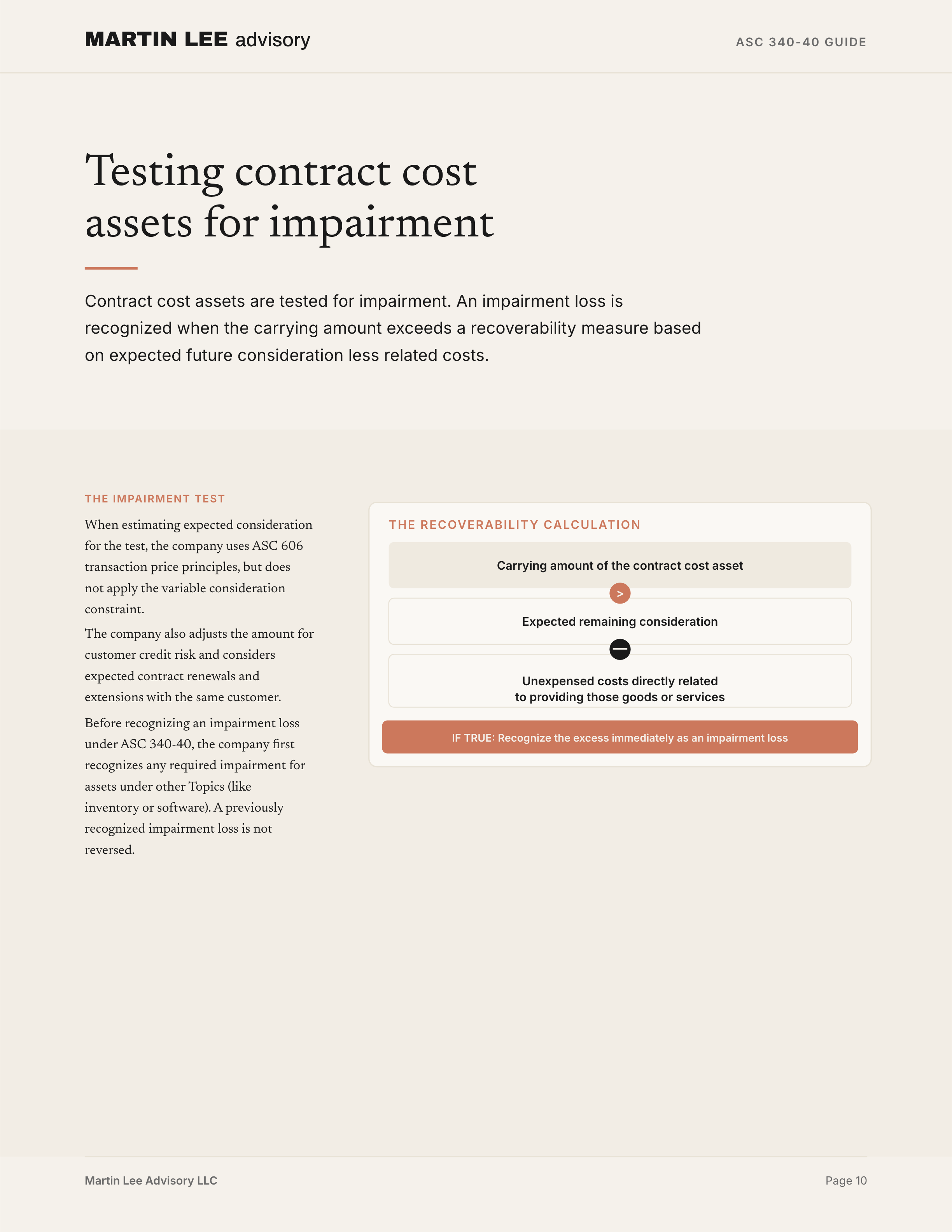

Impairment

Contract cost assets are tested for impairment. An impairment loss is recognized in profit or loss when the carrying amount of the asset exceeds a recoverability measure based on expected future consideration less related costs.

In simplified terms, the company compares:

Carrying amount of the contract cost asset

to

Expected remaining consideration

minus

costs directly related to providing the remaining goods or services

that have not yet been expensedIf the carrying amount is higher, the excess is recognized as an impairment loss.

When estimating expected consideration for the impairment test, the company uses the transaction price principles from ASC 606, but does not apply the variable consideration constraint. The company also adjusts the amount for customer credit risk and considers expected contract renewals and extensions with the same customer.

Before recognizing an impairment loss on a contract cost asset under ASC 340-40, the company first recognizes any impairment loss required for related assets accounted for under certain other Topics, such as inventory or software to be sold, leased, or otherwise marketed. After applying the ASC 340-40 impairment test, the resulting carrying amount is included in the relevant asset group or reporting unit for purposes of applying ASC 360 or ASC 350, if applicable.

A previously recognized impairment loss is not reversed.

Disclosure

The disclosure objective for contract cost assets is connected to ASC 606’s broader disclosure objective. Users should be able to understand the assets recognized from costs to obtain or fulfill contracts with customers.

A company discloses:

- the judgments made in determining the amount of costs incurred to obtain or fulfill contracts with customers;

- the method used to determine amortization for each reporting period;

- closing balances of assets recognized from costs to obtain or fulfill contracts, by main category of asset; and

- the amount of amortization and any impairment losses recognized during the reporting period.

Examples of asset categories include costs to obtain contracts with customers, precontract costs, and setup costs.

ASC 340-40 also requires disclosure if the company elects the practical expedient to expense incremental costs of obtaining a contract when the amortization period would have been one year or less. Certain nonpublic entities may elect not to provide some of the ASC 340-40 disclosures.

The disclosure section is short, but it is still important. Capitalized contract costs often involve judgment, especially when determining whether costs are incremental, whether fulfillment costs create or enhance resources for future performance, and what amortization period should be used.

Simple examples

Example 1: Costs to obtain a contract

Assume a consulting firm wins a competitive bid to provide services to a new customer. It incurs the following costs:

| Cost | Amount |

|---|---|

| External legal fees for due diligence | $15,000 |

| Travel costs to deliver proposal | $25,000 |

| Sales commissions | $10,000 |

| Total | $50,000 |

The sales commission is capitalized if the company expects to recover it, because it is incremental to obtaining the contract. The company would not have incurred that cost if the contract had not been obtained.

The legal fees and travel costs are expensed as incurred because they would have been incurred regardless of whether the contract was obtained. They may have helped the company pursue the contract, but they are not incremental to obtaining it.

If the company also pays discretionary bonuses to sales supervisors based on overall sales targets, profitability, and individual performance, those bonuses are not capitalized merely because the company won the contract. They are not directly attributable to an identifiable contract and are not incremental to obtaining that contract.

Example 2: Setup costs for a service contract

Assume a company enters into a five-year service contract to manage a customer’s IT data center. The contract is renewable for one-year periods, and the average customer term is seven years. The company pays a $10,000 sales commission when the customer signs the contract.

The commission is capitalized if the company expects to recover it. If the asset relates to services expected to be provided over seven years, including anticipated renewals, the company amortizes the commission asset over seven years.

Before providing the service, the company designs and builds a technology platform for its own internal use that interfaces with the customer’s systems. The platform is not transferred to the customer, but it will be used to deliver services.

Assume the setup costs include:

| Cost | Accounting analysis |

|---|---|

| Hardware | Account for under ASC 360, not ASC 340-40. |

| Software | Account for under ASC 350-40, not ASC 340-40. |

| Design, migration, and testing | Evaluate under ASC 340-40 if not within another Topic. Capitalize only if the three fulfillment-cost criteria are met. |

| Payroll for employees providing the ongoing service | Expense as incurred if the costs do not generate or enhance resources for future performance. |

This example shows how ASC 340-40 interacts with other Topics. A cost may relate to a customer contract, but that does not mean ASC 340-40 is the right guidance. Hardware, software, and other assets may fall under other GAAP first.

Practical summary

ASC 340-40 can be summarized in a few questions.

Costs to obtain a contract

Was the cost incurred only because the contract was obtained?

↓

No → expense as incurred, unless explicitly chargeable to the customer

↓

Yes

↓

Is the cost expected to be recovered?

↓

No → expense as incurred

↓

Yes

↓

Capitalize, unless the company elects the practical expedient

for costs with an amortization period of one year or lessCosts to fulfill a contract

Is the cost within the scope of another Topic?

↓

Yes → apply that other Topic

↓

No

↓

Does the cost relate directly to a specific contract

or identifiable anticipated contract?

↓

No → expense as incurred

↓

Yes

↓

Does the cost generate or enhance resources used

to satisfy future performance obligations?

↓

No → expense as incurred

↓

Yes

↓

Is the cost expected to be recovered?

↓

No → expense as incurred

↓

Yes → capitalizeWhere this guide stops

This guide covers the core ASC 340-40 model: scope, capitalization of costs to obtain and fulfill contracts, costs expensed as incurred, amortization, impairment, disclosure, and the standard’s examples.

It does not address every practical issue that may arise in applying the guidance. Common areas that may require further analysis include sales commission plans, clawbacks, renewals, contract modifications, customer acquisition costs, setup activities, implementation activities, and the interaction between ASC 340-40 and other Topics such as ASC 350-40, ASC 360, and ASC 330.

Those topics are better handled in focused guides or examples that build on the core model explained here.