Page 01: IPO Accounting

The Visual Accounting Guide Series: IPO Accounting — The 1 to 6 Months Before Pricing.

The complete playbook for CFOs and controllers to structure, execute, and defend the accounting workstream before a U.S. IPO.

Page 02: Guide Map

How to use this guide: This guide follows the IPO accounting workstream from transaction sprint through S-1 support, audit readiness, comfort letters, SEC comments, operating model, and execution support.

The Critical Path: Accounting is the longest lead-time workstream in an IPO. The transaction timeline cannot outpace the delivery of PCAOB audits, SEC-compliant financials, and auditor comfort letters.

- 03. IPO transaction sprint: The 1–6 month transaction timeline and accounting workstreams underneath.

- 04. What changes in IPO mode: How private-company accounting changes under IPO pressure.

- 05. EGC assumption: What the EGC path means and what changes if relief is not available or not used.

- 06. Accounting deliverables map: Inputs, workstreams, outputs, and users of the S-1 accounting package.

- 07. From AICPA audit to PCAOB audit: The critical path from historical audit to IPO-ready audit support.

- 08. S-1 financial information stack: The controlled package of numbers, disclosures, metrics, and transaction data.

- 09. Five accounting danger zones: The issues most likely to create late disclosure, audit, or SEC friction.

- 10. Comfort letters: What accounting has to make possible before auditors can provide comfort.

- 11. Confidential filing treadmill: How submissions, SEC comments, amendments, refreshes, and pricing interact.

- 12. IPO accounting operating model: The roles, rituals, trackers, and escalation model for the accounting workstream.

- 13. How Martin Lee Advisory can help: The outsourced IPO accounting execution layer.

- 14. Contact: Firm information, contact details, and publication notice.

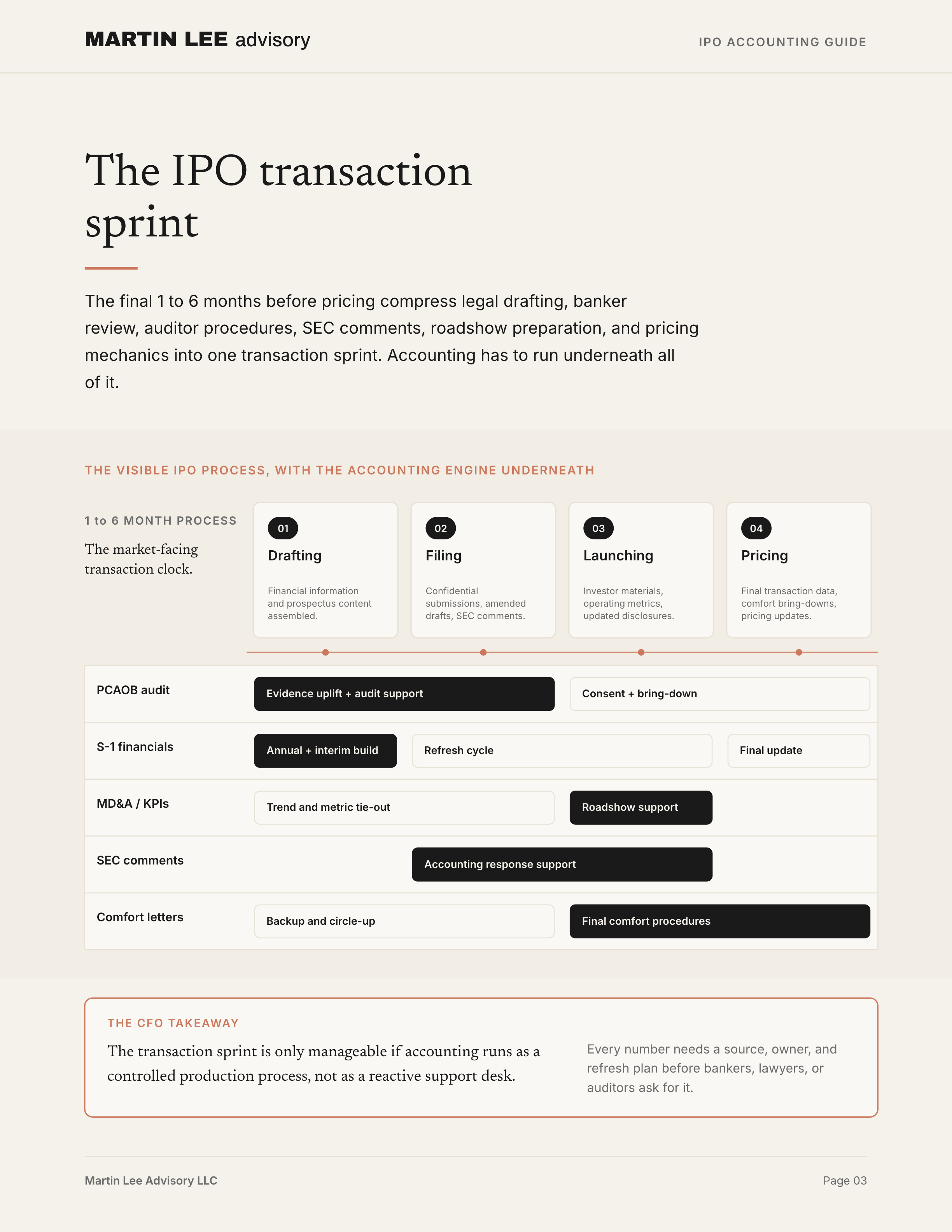

Page 03: The IPO Transaction Sprint

The final 1 to 6 months before pricing compress legal drafting, banker review, auditor procedures, SEC comments, roadshow preparation, and pricing mechanics into one transaction sprint. Accounting has to run underneath all of it.

- 01. Drafting: Financial information and prospectus content assembled.

- 02. Filing: Confidential submissions, amended drafts, SEC comments.

- 03. Launching: Investor materials, operating metrics, updated disclosures.

- 04. Pricing: Final transaction data, comfort bring-downs, pricing updates.

The CFO Takeaway: The transaction sprint is only manageable if accounting runs as a controlled production process, not as a reactive support desk. Every number needs a source, owner, and refresh plan before bankers, lawyers, or auditors ask for it.

Page 04: What Changes When Accounting Enters IPO Mode

IPO accounting is not just private-company accounting with more disclosure. The audit standard, evidence burden, disclosure regime, liability environment, and timeline velocity all change at once.

- Audit lens: Shifts from an AICPA audit focused on private-company financial statements to a PCAOB audit and S-1 readiness, with public-company expectations.

- Evidence burden: Support can no longer live across finance, legal, tax, and spreadsheets. Numbers need controlled sources, owners, reviewers, and refresh plans.

- Disclosure regime: Shifts from financial statements and lender/investor materials to S-1 financials, MD&A, risk factors, KPIs, non-GAAP, EPS, equity, and capitalization.

- Timing: Instead of annual close and audit cycles, filing dates, stale dates, SEC comments, roadshow timing, and pricing drive the sprint.

- Liability environment: Moves from mostly contractual and investor-facing accountability to underwriter diligence, auditor procedures, SEC review, and public-market scrutiny.

The CFO Takeaway: IPO mode is a production environment. The finance team needs issue ownership, tie-out discipline, audit support, and escalation rhythms before the filing calendar takes over.

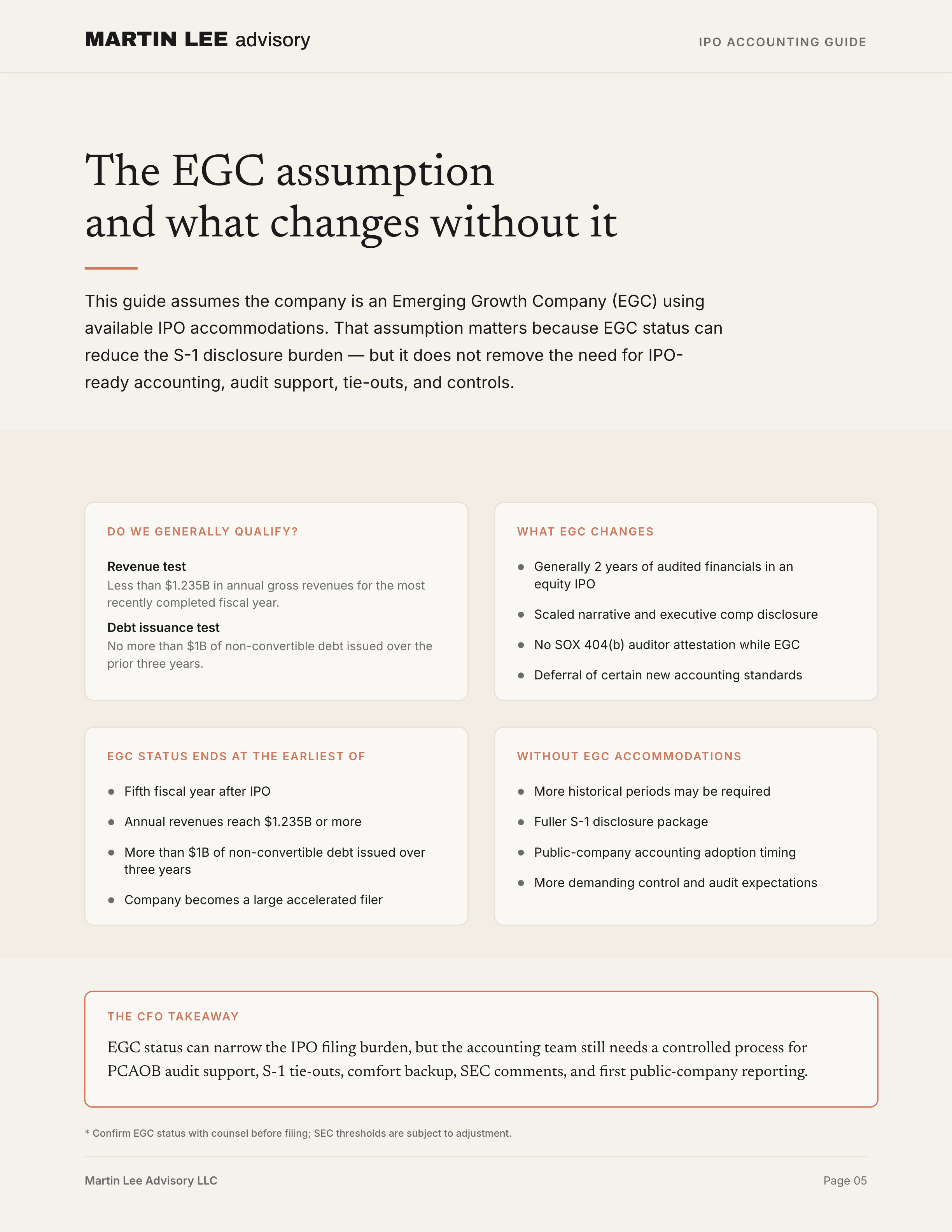

Page 05: The EGC Assumption

This guide assumes the company is an Emerging Growth Company (EGC) using available IPO accommodations. That assumption matters because EGC status can reduce the S-1 disclosure burden — but it does not remove the need for IPO-ready accounting, audit support, tie-outs, and controls.

- What EGC Changes: Generally 2 years of audited financials in an equity IPO; scaled narrative and executive comp disclosure; no SOX 404(b) auditor attestation while EGC; deferral of certain new accounting standards.

- Without EGC Accommodations: More historical periods may be required; fuller S-1 disclosure package; public-company accounting adoption timing; more demanding control and audit expectations.

The CFO Takeaway: EGC status can narrow the IPO filing burden, but the accounting team still needs a controlled process for PCAOB audit support, S-1 tie-outs, comfort backup, SEC comments, and first public-company reporting.

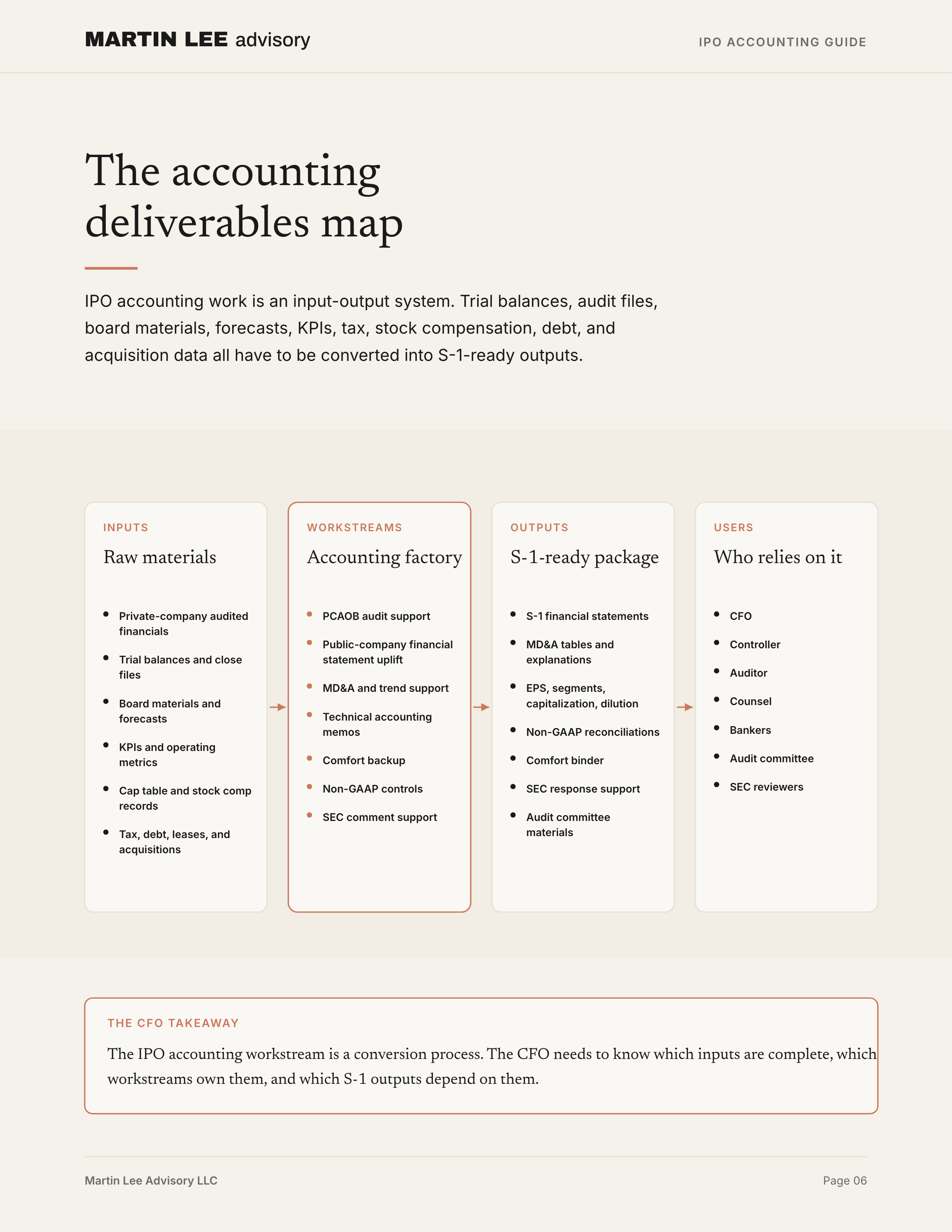

Page 06: The Accounting Deliverables Map

IPO accounting work is an input-output system. Trial balances, audit files, board materials, forecasts, KPIs, tax, stock compensation, debt, and acquisition data all have to be converted into S-1-ready outputs.

- Inputs (Raw materials): Private-company audited financials, trial balances, close files, board materials, forecasts, KPIs, cap table, tax, debt, leases, and acquisitions.

- Workstreams (Accounting factory): PCAOB audit support, public-company financial statement uplift, MD&A and trend support, technical accounting memos, comfort backup, non-GAAP controls, SEC comment support.

- Outputs (S-1-ready package): S-1 financial statements, MD&A tables and explanations, EPS, segments, capitalization, dilution, Non-GAAP reconciliations, comfort binder, SEC response support.

The CFO Takeaway: The IPO accounting workstream is a conversion process. The CFO needs to know which inputs are complete, which workstreams own them, and which S-1 outputs depend on them.

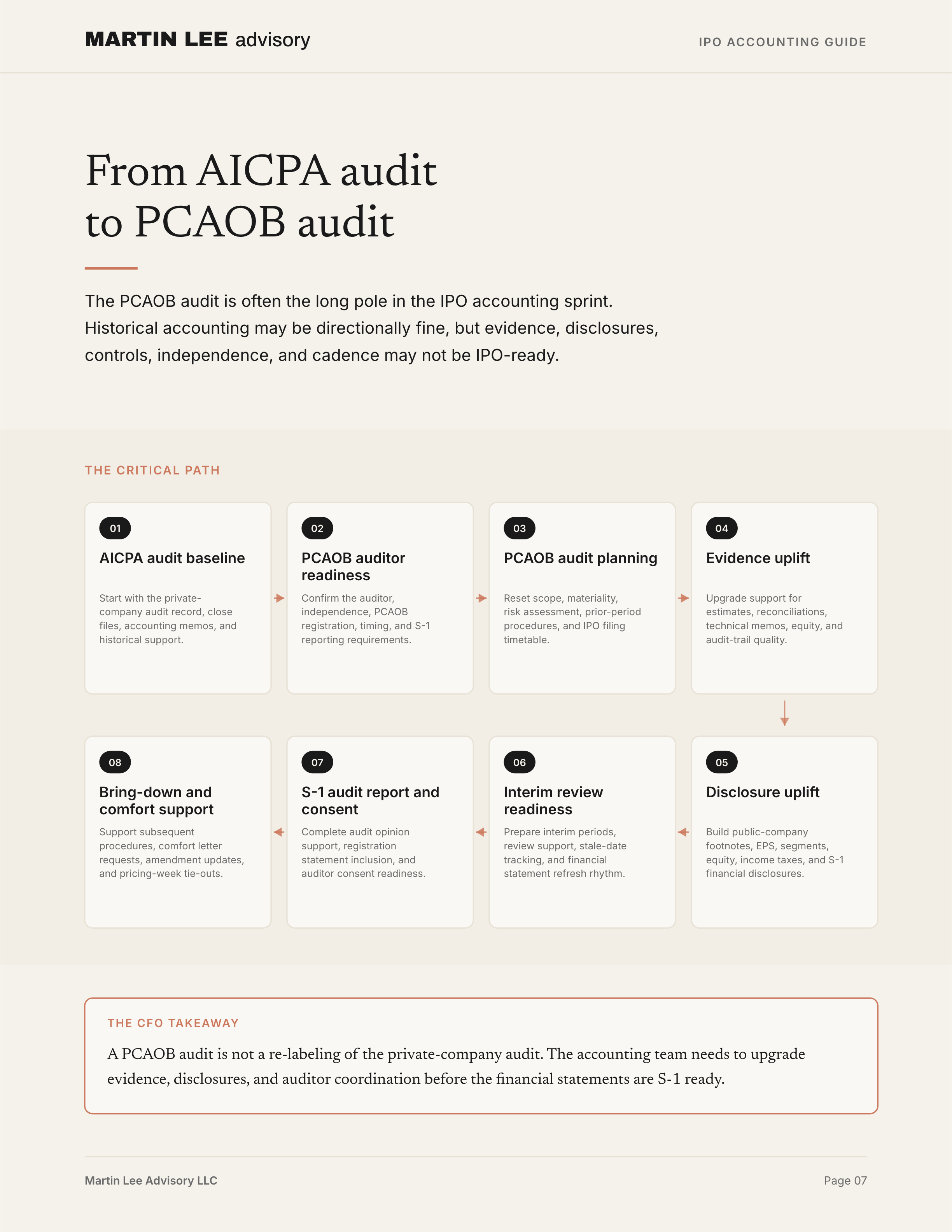

Page 07: From AICPA Audit to PCAOB Audit

The PCAOB audit is often the long pole in the IPO accounting sprint. Historical accounting may be directionally fine, but evidence, disclosures, controls, independence, and cadence may not be IPO-ready.

- AICPA audit baseline: Start with the private-company audit record, close files, accounting memos, and historical support.

- PCAOB auditor readiness: Confirm the auditor, independence, PCAOB registration, timing, and S-1 reporting requirements.

- PCAOB audit planning: Reset scope, materiality, risk assessment, prior-period procedures, and IPO filing timetable.

- Evidence uplift: Upgrade support for estimates, reconciliations, technical memos, equity, and audit-trail quality.

- Disclosure uplift: Build public-company footnotes, EPS, segments, equity, income taxes, and S-1 financial disclosures.

- Interim review readiness: Prepare interim periods, review support, stale-date tracking, and financial statement refresh rhythm.

- S-1 audit report and consent: Complete audit opinion support, registration statement inclusion, and auditor consent readiness.

- Bring-down and comfort support: Support subsequent procedures, comfort letter requests, amendment updates, and pricing-week tie-outs.

The CFO Takeaway: A PCAOB audit is not a re-labeling of the private-company audit. The accounting team needs to upgrade evidence, disclosures, and auditor coordination before the financial statements are S-1 ready.

Page 08: The S-1 Financial Information Stack

The registration statement is not just a set of financial statements. It is a controlled package of audited numbers, narrative disclosures, metrics, reconciliations, and transaction data that must survive auditor, banker, lawyer, and SEC review.

- Audited annual financial statements: PCAOB-audited annual financials, public-company disclosures, auditor report, and consent readiness.

- Interim financial statements: Unaudited interim periods, review support, age-of-financial-statement monitoring, and refresh planning.

- MD&A and operating trends: Liquidity, capital resources, results of operations, known trends, and period-over-period explanations.

- Metrics, KPIs, and non-GAAP measures: Definitions, consistency checks, reconciliations, disclosure controls, and support for banker materials.

- Capitalization, dilution, EPS, and equity: Preferred stock, options, RSUs, warrants, pro forma share counts, cheap stock, and EPS mechanics.

- Risk-factor and transaction support: Accounting-sensitive risk factors, subsequent events, related parties, tax, debt, and acquisition disclosures.

The CFO Takeaway: The S-1 is a consistency puzzle. Every number needs a controlled source, an owner, a reviewer, and a refresh plan. Weak tie-outs and late refreshes can quickly turn into filing delays.

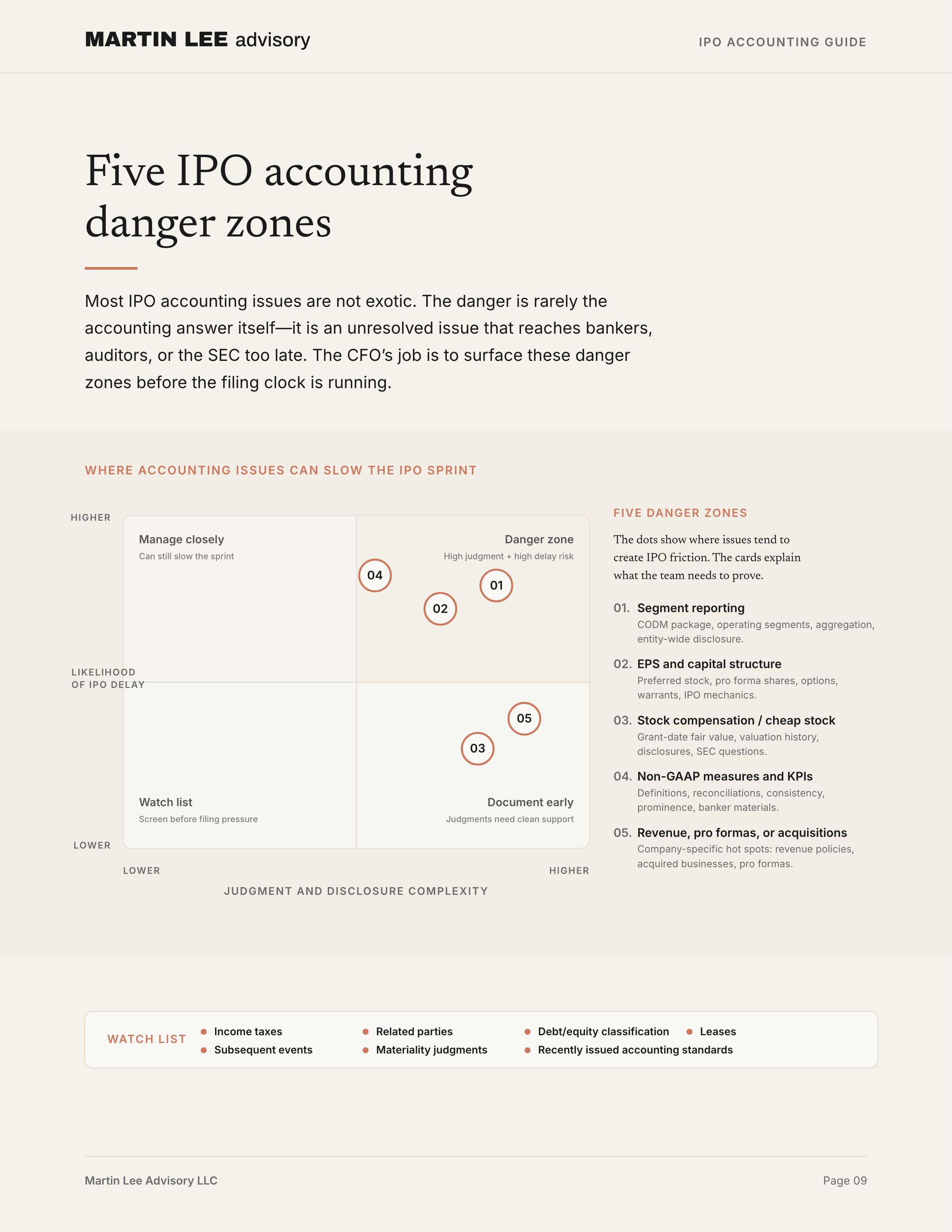

Page 09: Five IPO Accounting Danger Zones

Most IPO accounting issues are not exotic. The danger is rarely the accounting answer itself—it is an unresolved issue that reaches bankers, auditors, or the SEC too late. The CFO’s job is to surface these danger zones before the filing clock is running.

- 01. Segment reporting: CODM package, operating segments, aggregation, entity-wide disclosure.

- 02. EPS and capital structure: Preferred stock, pro forma shares, options, warrants, IPO mechanics.

- 03. Stock compensation / cheap stock: Grant-date fair value, valuation history, disclosures, SEC questions.

- 04. Non-GAAP measures and KPIs: Definitions, reconciliations, consistency, prominence, banker materials.

- 05. Revenue, pro formas, or acquisitions: Company-specific hot spots: revenue policies, acquired businesses, pro formas.

Page 10: Comfort Letters

The auditor issues the comfort letters, but the company creates the support environment. Accounting has to make S-1 numbers traceable, testable, refreshed, and ready for the scope and level of comfort requested by underwriters and counsel.

- Draft S-1 population: Identify the financial, KPI, and operating data that may be requested for comfort.

- Circle-up and comfort scope: Align on which numbers are circled, what level of comfort is requested, and what the auditor can provide.

- Evidence and backup build: Develop support for each number, including source systems, reconciliations, owner sign-offs, and non-financial evidence.

- Draft letter and tickmark legend: Agree on comfort letter language, tickmark meanings, included procedures, and excluded items.

- Auditor procedures: Auditors perform agreed procedures, compare supported amounts to the S-1, and identify exceptions.

- Open item clearance: Resolve backup gaps, refresh support, update S-1 tie-outs, and clear comments before launch or pricing.

- Pricing comfort letter: At effectiveness and pricing, the auditor issues the comfort letter.

- Bring-down comfort letter: At closing, the auditor issues a bring-down letter after refreshing procedures for subsequent changes.

The CFO Takeaway: Comfort letter readiness is a market-readiness test: can the company prove the numbers it is putting in front of underwriters and investors? Late backup gaps can delay filings, roadshow launch, pricing, or final sign-off.

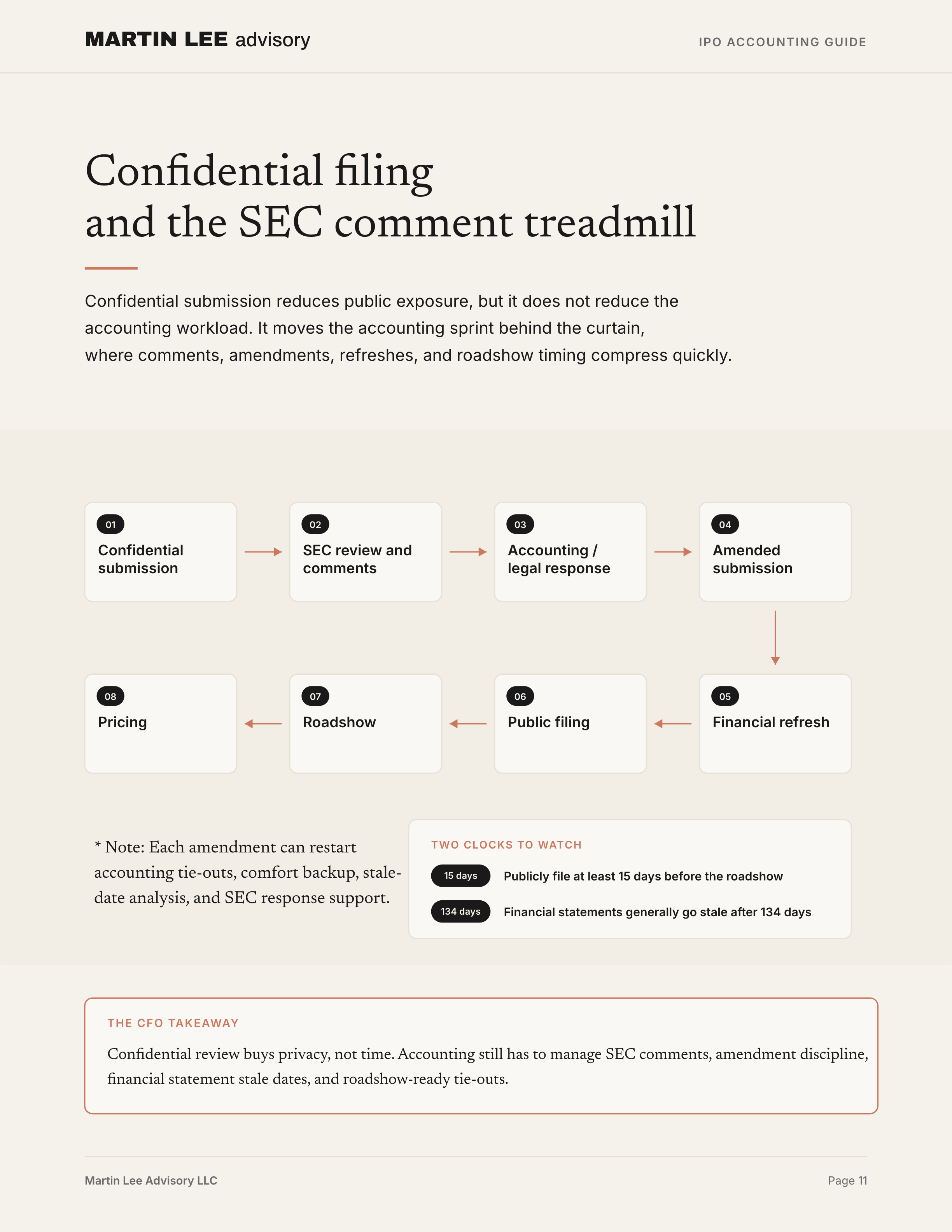

Page 11: Confidential Filing Treadmill

Confidential submission reduces public exposure, but it does not reduce the accounting workload. It moves the accounting sprint behind the curtain, where comments, amendments, refreshes, and roadshow timing compress quickly.

Two clocks to watch: 1. Publicly file at least 15 days before the roadshow. 2. Financial statements generally go stale after 134 days.

The CFO Takeaway: Confidential review buys privacy, not time. Accounting still has to manage SEC comments, amendment discipline, financial statement stale dates, and roadshow-ready tie-outs.

Page 12: The IPO Accounting Operating Model

The CFO does not need every answer personally. The CFO needs a system that identifies accounting issues early, assigns ownership, documents judgments, and prevents surprises.

Operating Rituals: The operating model works only if the team runs the same trackers and escalation rhythms every week: Daily filing standup, S-1 tie-out tracker, Comfort tracker, SEC comment tracker, Audit PBC dashboard, Disclosure committee review, Audit committee checkpoints, Open issue escalation list.

Page 13: An Outsourced IPO Accounting Execution Layer

The IPO accounting sprint is too important to manage with spare capacity. Martin Lee Advisory brings former Big 4 audit partner judgment, hands-on execution, and transaction project management to the accounting workstream.

- IPO accounting project management: Timelines, owners, dependencies, open items, and working-group coordination.

- PCAOB audit support: Audit-ready schedules, technical memos, evidence uplift, and auditor coordination.

- S-1 financial information: Financial statement uplift, EPS, segments, MD&A support, capitalization, and disclosure tie-outs.

- Comfort letter readiness: Circle-up support, backup binders, source evidence, refreshes, and open item tracking.

- SEC comment support: Accounting analyses, response support, revised disclosures, and issue resolution.

The CFO Takeaway: The goal is not to produce another readiness report. The goal is to help the accounting function execute — from diagnostic through filing support, audit defense, comfort readiness, and the first public-company reporting cadence.