ASC 350-40: Internal-Use Software

A practical guide to capitalizing software a company develops, acquires, or modifies for its own internal needs — covering scope, when capitalization starts and stops, what costs qualify, amortization, and the treatment of SaaS implementation costs.

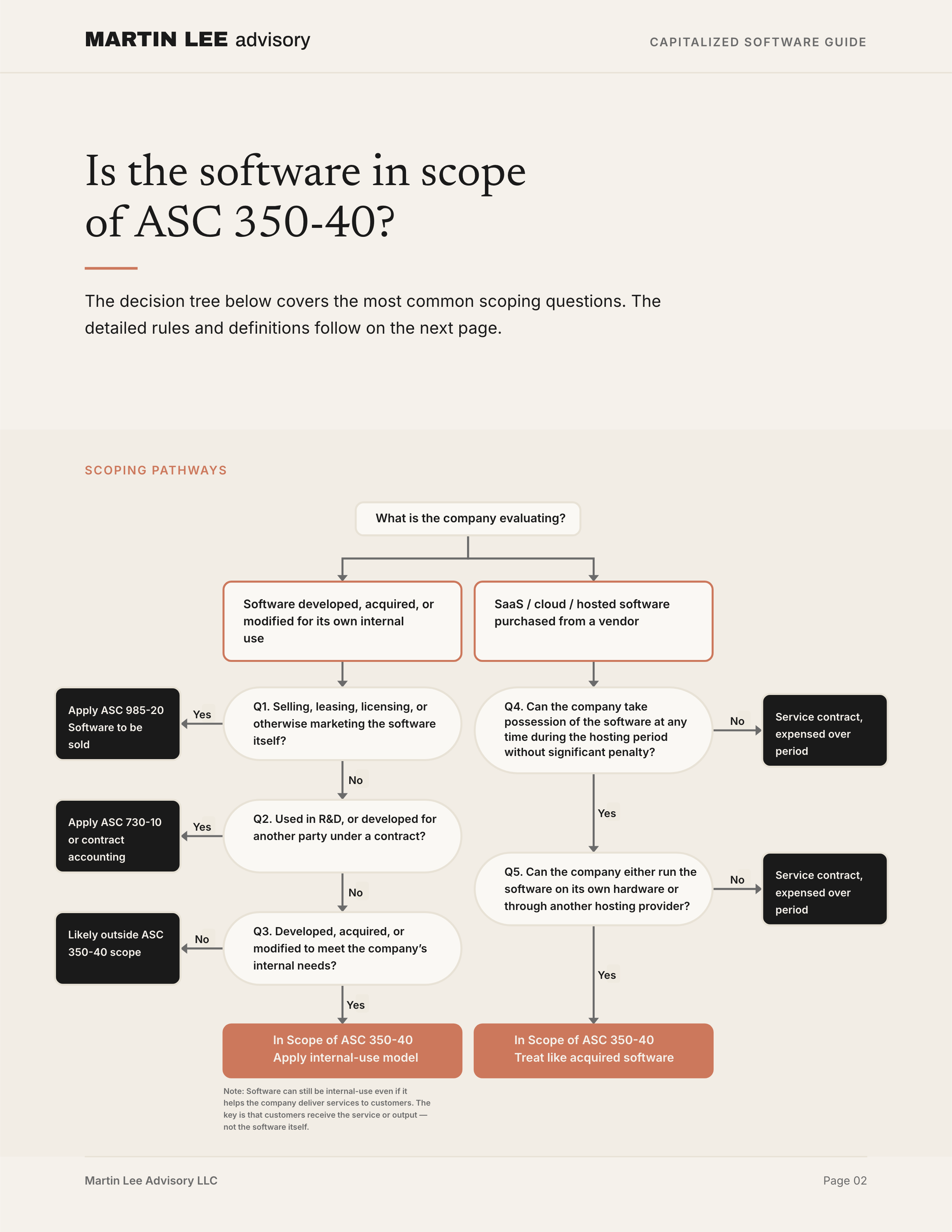

Scope: Is the software in scope of ASC 350-40?

Internal-use software is not limited to back-office systems. It can include platforms, systems, or tools used to operate the business, automate internal processes, or deliver services to customers. Customer-facing use does not automatically mean the software is being sold. The key is whether the company is using the software to provide a service or output, rather than selling, licensing, or otherwise giving customers the software itself or a right to use it.

To qualify as internal-use software, the company also cannot have a substantive plan during development to sell, lease, license, or otherwise market the software. A substantive plan identifies marketing channels and the supporting activities — promotion, delivery, billing, support — and implementing the plan must be at least reasonably possible.

ASC 350-40 does not apply to software being sold, leased, licensed, or otherwise marketed (which falls under ASC 985-20), software used in research and development, software developed for another party under a contract, or business process reengineering activities.

When capitalization starts

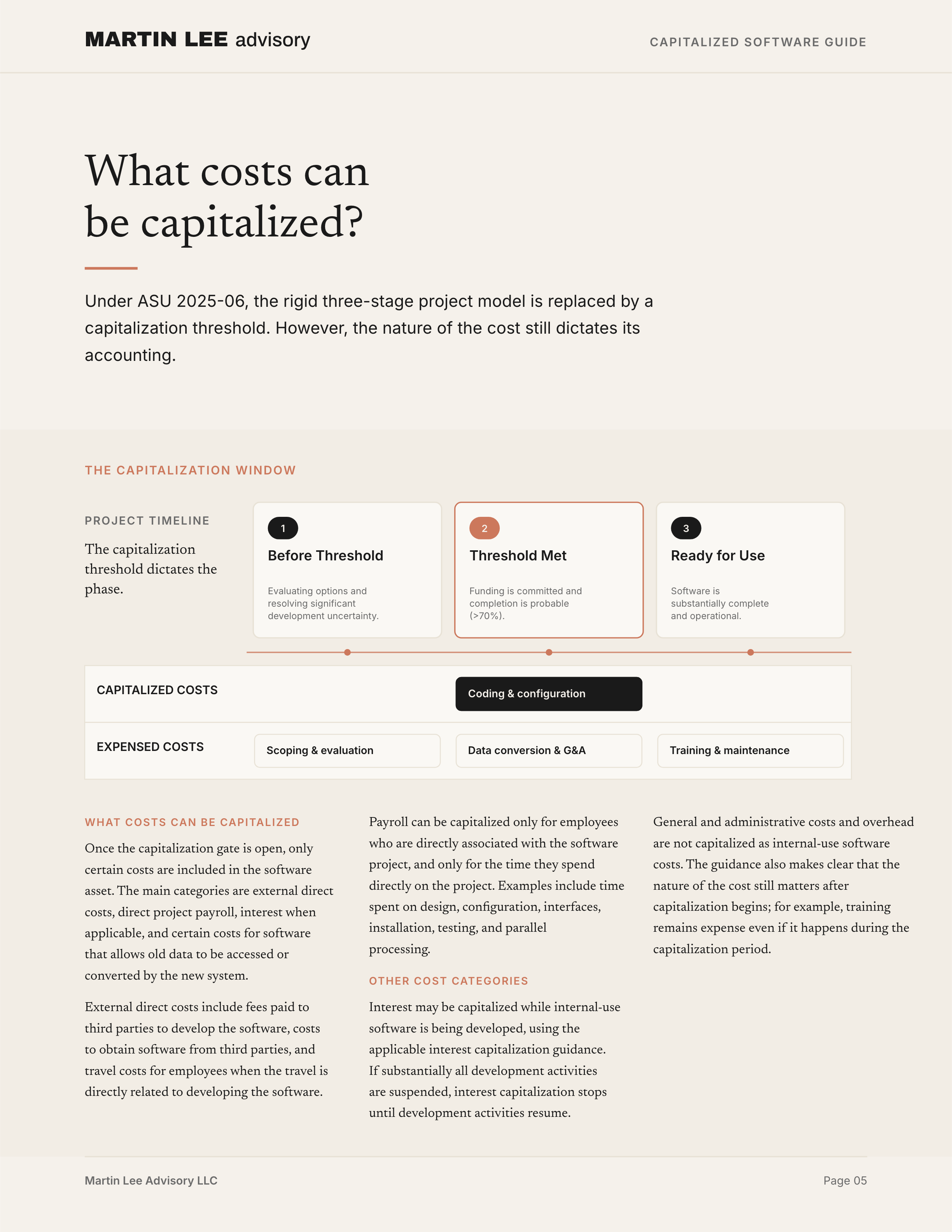

A company does not capitalize software costs just because a project has started. Costs incurred before the capitalization requirements are met are expensed as incurred. Training and data conversion activities are also generally expensed as incurred.

Capitalization begins only when two things are true. First, management with the right level of authority has approved the project and committed funding. Second, it is probable that the project will be completed and the software will be used as intended.

The probable threshold is not met if significant development uncertainty still exists, such as when the software includes novel, unique, unproven, or technologically innovative features that have not yet been resolved.

What costs can be capitalized

Once the capitalization gate is open, only certain costs are included in the software asset. The main categories are external direct costs, direct project payroll, interest when applicable, and certain costs for software that allows old data to be accessed or converted by the new system.

External direct costs include fees paid to third parties to develop the software, costs to obtain software from third parties, and travel costs for employees when directly related to developing the software.

Payroll can be capitalized only for employees who are directly associated with the software project, and only for the time they spend directly on the project. General and administrative costs, overhead, and training are not capitalized.

When capitalization stops & Amortization

Capitalization stops no later than when the software is substantially complete and ready for its intended use (after all substantial testing is complete).

Capitalized internal-use software is generally amortized on a straight-line basis, unless another systematic and rational method better reflects how the software is used. The useful life should be reassessed based on obsolescence, technology changes, and competition.

Impairment, Upgrades, and Other Issues

If software is still being developed and the capitalization requirements are no longer met, the company stops capitalizing additional costs and evaluates the existing capitalized balance for impairment. Warning signs include significant changes to the software program, costs significantly exceeding expectations, or lack of budget.

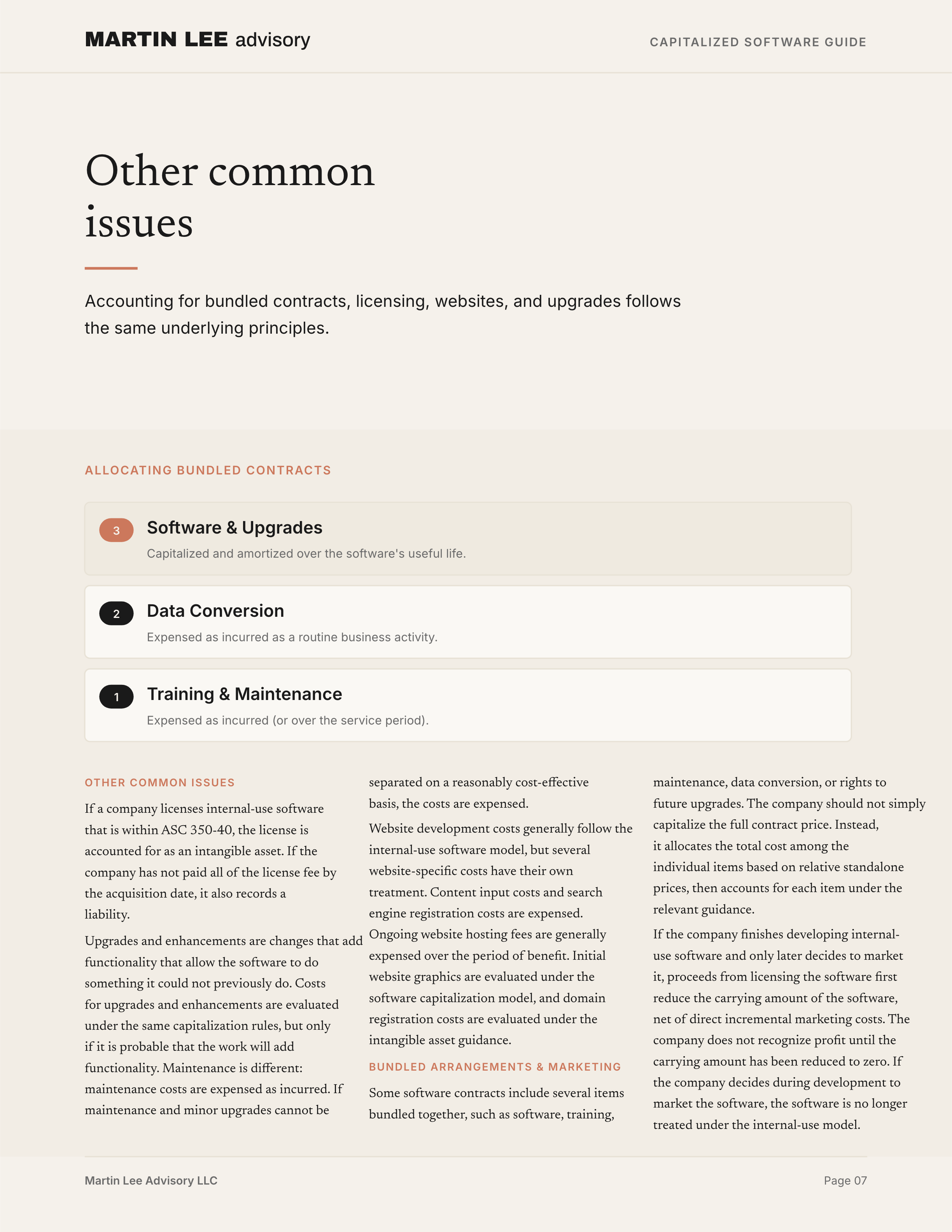

Costs for upgrades and enhancements are evaluated under the same capitalization rules, but only if it is probable that the work will add functionality. Maintenance costs are expensed as incurred.

SaaS and hosting arrangements

For a customer accessing software through a SaaS or hosting arrangement, the standard internal-use software model applies only if both conditions are met: the customer has the contractual right to take possession of the software at any time during the hosting period without significant penalty, and it is feasible for the customer to run the software itself.

Even when the SaaS or hosting arrangement is a service contract, ASC 350-40 still matters because implementation costs are evaluated using the internal-use software framework. Capitalized implementation costs for a SaaS contract are amortized over the term of the associated arrangement.

Disclaimer: This guide is provided for general orientation and is not specific accounting advice. Applications of ASC 350-40 require detailed facts-and-circumstances analysis.